TL;DR:

- Structured crypto banking workflows with operational substance improve account stability for iGaming.

- A hybrid offshore and EU EMI setup offers flexibility and compliance advantages in 2026.

- Proper documentation, continuous compliance, and transparency are essential to avoid banking closures.

Blocked accounts, rejected applications, and compliance requests that never seem to end. If you operate in iGaming or crypto, this is not bad luck; it is the predictable result of approaching high-risk banking without a structured workflow. The good news is that operators who treat banking as a process rather than a one-time task consistently outperform those who scramble from crisis to crisis. This guide walks you through every stage of a proven crypto banking workflow, from initial setup and document preparation through to live operations and ongoing compliance, with specific attention to the regulatory realities facing iGaming businesses in 2026.

Key Takeaways

| Point | Details |

|---|---|

| Combine offshore and EU EMI | A dual structure offers flexibility while satisfying EU compliance for iGaming. |

| Prepare substance and documentation | Banks require real operations, not just paperwork, plus full KYC/AML files. |

| Follow verified workflow steps | Proceed in sequence from legal structuring to ongoing transaction audits. |

| Treat crypto as a compliance ally | Leveraging blockchain traceability is now a benefit, not a loophole. |

| Stay ahead of 2026 EU regulation | Align processes with MiCA and stablecoins to futureproof your banking. |

Understanding the challenges: crypto banking for iGaming

The banking landscape for iGaming and crypto businesses has shifted considerably. Regulatory pressure from frameworks like MiCA (Markets in Crypto-Assets Regulation), alongside tightening KYC (Know Your Customer) and AML (Anti-Money Laundering) requirements, means that the window for informal or loosely structured banking arrangements is closing fast. By mid-2026, any crypto-related business operating within the EU must demonstrate full MiCA compliance or risk losing access to payment infrastructure entirely.

Mainstream banks and many neobanks have responded to this pressure by simply refusing iGaming and crypto clients outright. Their risk models are calibrated for low-complexity retail and SME clients. Your business does not fit that model, and no amount of charm or persistence will change their internal policy. This is not a negotiation problem; it is a structural mismatch.

What many operators miss, however, is that crypto can actually work in your favour during compliance reviews, provided your workflow is built correctly. Blockchain transactions are inherently traceable, timestamped, and immutable. When structured properly, this transparency becomes a compliance asset rather than a liability.

Key obstacles you are likely facing right now:

- Mainstream banks categorically declining iGaming and crypto applications

- Compliance teams requesting documentation you have not prepared in advance

- Accounts frozen or closed due to unexplained transaction patterns

- Jurisdictional mismatches between your licence and your banking partner

- Insufficient evidence of operational substance to satisfy due diligence

As iGaming Business notes, banks prefer operational entities over shells; demonstrating substance through real servers, active staff, and traceable business activity is what moves applications forward. Crypto’s traceability, when used correctly, is a compliance tool, not a loophole.

“The operators who succeed in banking are those who treat compliance as infrastructure, not an afterthought. Transparency built into your workflow from day one is what keeps accounts open.”

If you are starting from scratch or rebuilding after a closure, iGaming bank account opening requires a fundamentally different approach than standard business banking. Understanding offshore banking for high-risk businesses is equally important before you commit to any structure.

With the need for structure clear, next we will assess what you must prepare before setup.

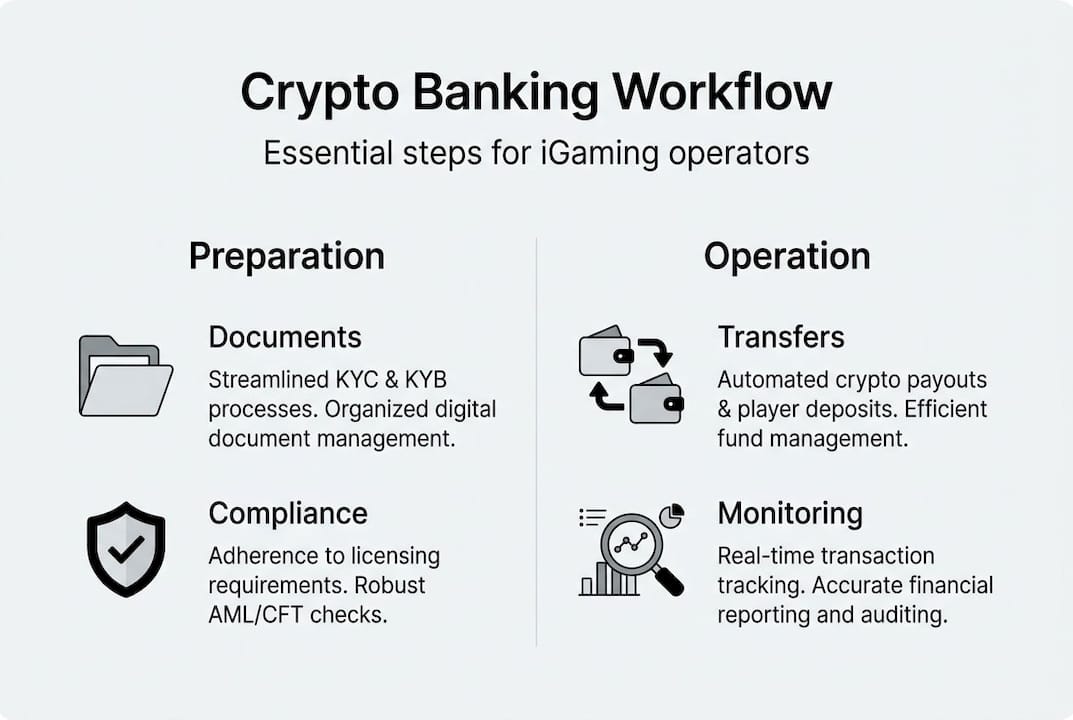

Setting up: prerequisites and workflow design

Before you submit a single application, your business needs to be bank-ready. This means more than having a company registered somewhere. It means assembling the full picture that a compliance officer will scrutinise during due diligence.

The most robust structure for iGaming operators in 2026 combines an offshore entity with an EU Electronic Money Institution (EMI) account for SEPA access. As outlined in offshore banking for high-risk businesses, offshore suits startups and high-risk operations well, but pairing this with an EU EMI for SEPA ensures you can process European player payments without friction. Stablecoins play a key role here too, minimising exchange-rate volatility across your treasury.

Here is what you need to document before onboarding begins:

- Certificate of incorporation and corporate structure chart

- Proof of operational substance: office lease, server contracts, employment records

- Gaming or crypto regulatory licence (jurisdiction-specific)

- KYC and AML policy documentation, including your compliance officer’s credentials

- Source of funds and source of wealth declarations for all UBOs (Ultimate Beneficial Owners)

- Six months of bank statements or financial projections for new entities

- Website and platform documentation showing live or near-live operations

Pro Tip: Do not wait for a bank to ask for these documents. Prepare a compliance dossier before you approach any institution. Operators who arrive with complete documentation close accounts in weeks, not months.

The following table maps the core tools and services you will need across each layer of your workflow:

| Workflow layer | Tool or service type | Purpose |

|---|---|---|

| Legal | Corporate law firm or agent | Entity setup, UBO registration |

| Banking | EU EMI plus offshore bank | SEPA access and treasury holding |

| Platform | iGaming software provider | Player management and game delivery |

| Payments | PSP or payment processor | Fiat deposit and withdrawal rails |

| Crypto | Stablecoin wallet or custodian | Volatility management and treasury |

For operators needing SEPA-enabled bank accounts specifically, the EU EMI route is currently the most reliable path. Understanding the full range of crypto banking solution types available will also help you select the right combination for your volume and jurisdiction.

With an understanding of the risks, it is time to assemble what you will need for successful onboarding.

Step-by-step workflow: from onboarding to operations

Once your prerequisites are in place, these are the exact steps you will follow for a live crypto banking workflow.

- Register your entity in your chosen jurisdiction, ensuring the structure supports your intended banking and licensing goals.

- Obtain your regulatory licence before approaching banks. Most EMIs and offshore banks will not engage without one.

- Open your offshore account for treasury and crypto holdings, using a bank familiar with iGaming activity.

- Open your EU EMI account for SEPA transactions, player deposits, and European payment processing.

- Integrate your payment processor with both accounts, ensuring fiat rails connect cleanly to your platform.

- Set up stablecoin treasury management to hold operational reserves without exposure to crypto price swings.

- Establish your compliance monitoring system, including real-time transaction monitoring and scheduled KYC reviews.

Pro Tip: Document every movement between crypto and fiat meticulously. Each conversion, transfer, and settlement should carry a timestamp, reference number, and business purpose. This is your audit trail, and it will be the first thing a regulator or bank requests if questions arise.

The choice of banking structure significantly affects your operational flexibility. Here is a comparison of the three main approaches:

| Structure | Pros | Cons |

|---|---|---|

| Fully onshore (EU only) | Regulatory clarity, SEPA native | Very limited bank options for iGaming |

| Fully offshore | Flexibility, fewer restrictions | Limited fiat access, SEPA exclusion |

| Hybrid (offshore plus EU EMI) | Best of both, compliance-friendly | Requires more setup and ongoing management |

The hybrid model consistently outperforms the alternatives for iGaming operators. MiCA compliance is critical for EU crypto activity by mid-2026, and stablecoins minimise volatility across your treasury holdings. Operators using crypto banking services for casino operators benefit from pre-structured workflows that account for these requirements. Your payment processing solutions must also align with your banking structure to avoid settlement delays. Keeping a live crypto compliance checklist updated throughout operations is not optional; it is the mechanism that keeps your accounts active.

Now, to keep your new workflow running smoothly, watch for these common stumbling blocks.

Troubleshooting and compliance: pitfalls to avoid

Even well-structured workflows fail when operators make predictable mistakes. Understanding these pitfalls in advance saves you from account closures, frozen funds, and regulatory investigations.

The most damaging errors we see repeatedly:

- Shell company reliance: Registering an entity without genuine operational substance is the fastest route to account closure. Banks conduct enhanced due diligence on iGaming clients, and a company with no staff, no servers, and no activity will not survive scrutiny.

- Outdated KYC files: KYC is not a one-time exercise. Player and UBO records must be refreshed regularly, and any change in ownership or structure must be reported promptly.

- Missing transaction monitoring: Real-time monitoring of crypto and fiat flows is now expected, not optional. AML flags triggered by unusual patterns can freeze accounts within hours.

- Ignoring MiCA timelines: Operators who have not aligned their EU crypto operations with MiCA by mid-2026 face the real prospect of losing banking access across the region.

- Jurisdiction mismatch: Your gaming licence, banking jurisdiction, and player base must be legally compatible. Mismatches create compliance gaps that banks will identify during periodic reviews.

As iGaming Business confirms, crypto’s traceability is a compliance asset when used correctly, not a mechanism for avoiding oversight. Operators who treat it as the latter consistently face enforcement action.

“The operators who lose banking access are rarely those who broke the rules deliberately. They are usually those who did not build compliance into their daily operations from the start.”

Practical fixes to implement now:

- Maintain a live compliance file updated monthly, not just at onboarding

- Use stablecoins for treasury reserves to reduce volatility-related transaction anomalies

- Prioritise SEPA compatibility in every banking relationship you build

- Seek bank account pre-approval before committing to a jurisdiction or structure

- Review offshore bank account options specifically designed for iGaming to avoid generic high-risk mismatches

Why most crypto banking guides miss the operational truth

Most guides in this space focus on finding the right jurisdiction or the most permissive bank. That framing is fundamentally wrong, and it leads operators into short-term fixes that collapse under scrutiny.

The real lesson from working with iGaming operators across dozens of banking engagements is this: substance wins, always. Banks are not looking for clever structures; they are looking for real businesses. Servers, staff, licences, transaction history, and a compliance officer who actually knows your operation. These are the signals that keep accounts open.

Treating crypto as a compliance tool rather than a workaround is the shift that separates operators with stable banking from those perpetually rebuilding after closures. Blockchain traceability, when embedded into your workflow, gives banks exactly what they want: a clear, auditable record of legitimate business activity.

The smartest operators we work with run hybrid setups, blending offshore flexibility with EU EMI access, and they keep everything audit-trail ready at all times. Understanding offshore jurisdiction strategies is part of this, but it is the operational discipline behind the structure that actually delivers sustainable banking. The guide that tells you to find a loophole is the guide that will cost you your accounts.

Expert support to optimise your crypto banking workflow

If you are ready to avoid pitfalls and fast-track your success, these tailored solutions can help. At BankMyCapital, we work directly with iGaming operators and crypto entrepreneurs to design and implement banking workflows that hold up under regulatory scrutiny. Our network of over 50 pre-vetted banking partners and EMIs means we match your specific structure to institutions already familiar with your sector. From crypto banking setup support to full compliance dossier preparation and jurisdiction selection, we handle the complexity so you can focus on operations. Our offshore banking solutions are built for exactly this challenge, with an 87% approval rate and onboarding timelines of two to three weeks.

Frequently asked questions

What is the most effective structure for crypto banking in iGaming?

A dual setup combining an offshore entity with an EU EMI for SEPA access delivers the best balance of flexibility, compliance, and operational efficiency. This hybrid approach suits high-risk operators far better than a purely onshore or purely offshore arrangement.

How does MiCA affect iGaming crypto banking in 2026?

MiCA enforces tighter compliance and due diligence standards for any crypto interaction in the EU, and full adherence is mandatory by mid-2026. Operators who have not aligned their operations with MiCA risk losing EU banking and payment access.

Can using stablecoins help manage crypto volatility for iGaming?

Yes, stablecoins minimise volatility and are widely used for iGaming treasury management in multi-bank setups, reducing the risk of anomalous transaction patterns triggering compliance flags.

Why do banks reject iGaming and crypto businesses?

Banks prefer real operational businesses with demonstrable substance and reject shell entities or those with incomplete compliance documentation. The rejection is structural, not personal.

What is one common mistake in the crypto banking workflow?

Relying solely on on/off ramps without maintaining continuous audit trails and compliance updates is the most frequent cause of account closures among iGaming operators.