Securing reliable banking is often the toughest hurdle for high-risk online businesses operating across the European Union and offshore. Regulations introduced by the European Banking Authority and enforced by national regulators shape your pathway to partnership, directly affecting account approvals and ongoing compliance. By breaking down the complexities of the Single Rulebook and sector-specific controls, this guide helps you anticipate documentation requests and build a compliance strategy that aligns with evolving EU standards.

Key Takeaways

| Point | Details |

|---|---|

| Understanding EU Regulations | EU banking regulations are crucial for securing banking partnerships, especially for high-risk businesses. Being well-prepared can enhance your compliance status. |

| Importance of Documentation | Quality of documentation significantly influences banking approvals; over-documentation can improve your chances. Ensure all compliance frameworks and records are well-organised. |

| Sector-Specific Requirements | Different high-risk sectors face unique regulations that must be adhered to; understanding these specific rules aids in preparing appropriate documentation. |

| Ongoing Compliance Duties | Compliance does not end with account approval; regular audits and updates are essential to maintaining good banking relationships and avoiding operational issues. |

Defining EU Banking Regulations for Businesses

EU banking regulations form the backbone of financial stability across the bloc. These rules exist to protect customers, ensure banks operate safely, and maintain confidence in the entire financial system. For high-risk businesses like yours, understanding these regulations is not optional—it directly impacts your ability to secure banking partnerships.

The European Banking Authority oversees a harmonised framework called the Single Rulebook. This rulebook applies across all Member States, creating consistency in how banks operate. Think of it as the universal standard that every bank in the EU must follow.

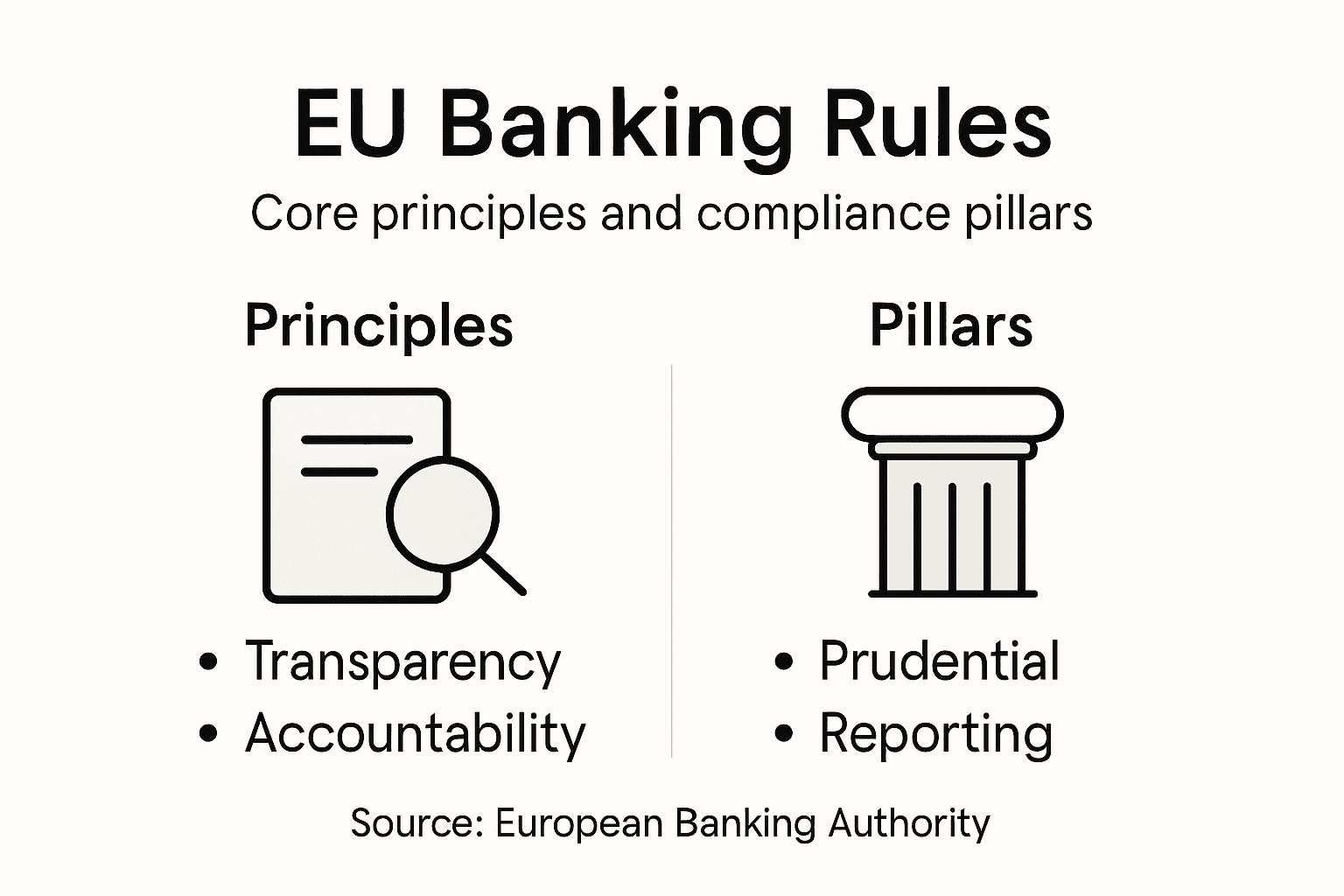

The regulatory framework covers three main pillars:

- Prudential requirements ensure banks maintain adequate capital and manage risks properly

- Operational standards govern how banks conduct daily business and protect customer funds

- Governance rules define how banks structure their leadership and decision-making

For your business, these regulations matter because they determine what banks can and cannot do when working with high-risk sectors. A bank cannot simply decide to accept your account—they must comply with strict regulatory requirements first.

When you approach a bank, they conduct due diligence based on regulatory obligations. This isn’t bureaucratic friction; it’s a legal mandate. They verify your identity, check compliance with anti-money laundering rules, and assess whether your business model aligns with their risk appetite.

EU financial regulation also establishes principles around transparency and accountability. Banks must report regularly to regulators, maintain detailed records, and demonstrate compliance. This creates an audit trail for every significant transaction.

High-risk sectors face additional scrutiny because regulators classify them as elevated risk. This doesn’t mean banking is impossible—it means banks need stronger assurances about your operations. Your compliance documentation, business structure, and transaction patterns all come under review.

The regulations evolve constantly. The EBA publishes guidelines regularly, and Member States implement new requirements as needed. What’s compliant today might require adjustments tomorrow. This is why ongoing banking compliance matters more than a one-time approval.

Understanding these regulations helps you position your business strategically. When you know what banks are required to verify, you can prepare documentation in advance. You can structure your operations to demonstrate genuine compliance rather than scrambling when a bank requests information.

Banks don’t reject high-risk businesses because of regulations—they reject those unprepared to meet regulatory requirements. The difference is preparation.

Your jurisdiction matters too. Some EU Member States implement stricter interpretations than others. A bank in Malta may assess risk differently than one in Germany, though both follow the same rulebook. This variance is why jurisdiction selection impacts your approval timeline significantly.

Pro tip: Document every aspect of your compliance framework before approaching banks. Organised evidence of regulatory adherence—licensing, transaction histories, beneficial ownership details—transforms you from a regulatory risk into a well-managed client.

Key Regulatory Bodies and Legal Frameworks

EU banking doesn’t operate under a single regulator making all decisions. Instead, multiple bodies work together, each with specific responsibilities. Understanding who controls what helps you grasp why banks behave the way they do.

The European Central Bank (ECB) supervises the largest banks directly, handling prudential oversight and stress testing. National central banks oversee smaller institutions within their Member States. Together, they form the Single Supervisory Mechanism, creating a coordinated approach across the bloc.

The European Banking Authority (EBA) acts as the harmoniser. Rather than directly supervising banks, the EBA issues guidelines ensuring financial institutions comply with EU and national laws. These guidelines cover sanctions, financial crime prevention, and governance arrangements that bind your banking options.

Key regulatory bodies include:

- European Central Bank oversees systemic financial stability and large bank prudential matters

- European Banking Authority creates harmonised standards across all Member States

- National regulators enforce rules within their jurisdictions and supervise smaller institutions

- Financial Action Task Force develops anti-money laundering and counter-terrorism financing standards

Regulation (EU) No 575/2013 establishes capital requirements that directly impact banking decisions. This regulation sets requirements for credit risk, market risk, operational risk, and capital buffers. Banks must maintain minimum capital levels, which constrains how aggressively they can lend or accept new clients.

For high-risk businesses, this matters because banks calculate risk-weighted assets for your account. A crypto business or adult entertainment platform occupies a different risk category than a standard retailer. The regulation forces banks to allocate more capital against your account, making approval decisions more conservative.

National regulators implement EU rules with local variations. A bank in Austria must follow EU law, but Austrian regulators add their own requirements. This creates a layered compliance structure where your business must satisfy both EU-level and country-level standards.

The EBA publishes guidelines regularly addressing emerging risks. Anti-money laundering guidance, beneficial ownership requirements, and sanctions screening protocols change as threats evolve. Banks tighten procedures when new EBA guidance appears, affecting approval criteria.

The regulatory framework isn’t rigid—it’s adaptive. Banks adjust controls when regulators issue new guidance, which is why your compliance needs may shift even after approval.

When approaching banks, understand that they’re operating under legal obligations from multiple sources. They’re not being difficult; they’re following directives from the ECB, EBA, and their national regulator simultaneously. This multi-layered oversight means banks err on the side of caution with unfamiliar sectors.

Here is a summary of core regulatory bodies and their major roles in EU banking regulation:

| Body | Main Responsibility | Effect on Businesses |

|---|---|---|

| European Central Bank (ECB) | Supervising large banks | Sets prudential expectations |

| European Banking Authority | Harmonising standards | Issues binding guidelines |

| National Regulators | Enforcing EU and local laws | Apply national compliance nuances |

| Financial Action Task Force | Anti-financial crime standards | Drives AML/CFT requirements |

Pro tip: Track EBA guidance updates and regulatory announcements in your sector. When banks tighten requirements, understanding the regulatory reason behind it helps you adjust your compliance strategy proactively rather than reactively.

Sector-Specific Rules for High-Risk Industries

High-risk industries don’t all face the same regulatory requirements. Crypto, iGaming, adult entertainment, and forex operate under distinct rule sets tailored to their specific risks. Banks treat each sector differently because regulators mandate sector-specific controls.

Your industry determines which compliance frameworks apply to your account. A cryptocurrency exchange faces anti-money laundering scrutiny that differs from an adult entertainment platform. Understanding your sector’s specific rules helps you prepare documentation banks will actually request.

Sector-specific rules typically address:

- Money laundering risks particular to your industry and transaction types

- Customer verification requirements scaled to sector risk profiles

- Transaction monitoring thresholds and suspicious activity reporting obligations

- Beneficial ownership disclosure standards specific to operational models

The crypto sector encounters the strictest scrutiny currently. Banks must verify wallet origins, track transaction flows, and monitor for sanctions compliance. The EU AI Act categorises certain AI applications in banking as high-risk and mandates additional safeguards, which affects how banks assess crypto clients using algorithmic risk scoring.

The iGaming sector must demonstrate responsible gambling controls and player protection measures. Banks require evidence of licensing, licence jurisdiction verification, and proof of responsible gaming software implementation. Transaction volatility patterns matter—banks flag unusual player fund movements as potential problem gambling indicators.

The forex sector faces position limit scrutiny and client suitability documentation requirements. Retail forex providers must show how they assess whether clients understand leverage risks. Banks verify that your operations comply with MiFID II suitability obligations.

Adult entertainment requires particular attention to payment processing and customer verification. Banks need evidence that your platform verifies customer age, maintains content moderation, and complies with local obscenity laws across jurisdictions where customers operate.

Guidelines managing Environmental, Social, and Governance risks increasingly affect sectors with environmental impact. Energy-intensive operations or businesses linked to carbon-heavy supply chains face enhanced ESG scrutiny from banks assessing transition risks.

The table below compares how selected high-risk industries face distinct banking requirements in the EU:

| Industry | Unique Banking Focus | Main Documentation Needed | Common Bank Concern |

|---|---|---|---|

| Crypto | Wallet tracing and sanctions | Wallet provenance; AML policies | Transaction traceability |

| iGaming | Player protection verification | Licence verification; risk controls | Volatile player fund movements |

| Forex | Suitability and leverage review | Suitability assessments; trade logs | High leverage risk to clients |

| Adult Entertainment | Customer age and content checks | Age verification; moderation reports | Payment processing transparency |

Regulators don’t create sector-specific rules to punish industries—they create them because certain sectors present genuine operational or financial crime risks that require targeted controls.

When preparing your banking application, sector intelligence matters more than generic compliance documentation. Banks want evidence you understand your sector’s specific regulatory obligations and have implemented controls matching those requirements.

Your internal compliance programme should mirror your sector’s specific risk profile. If you operate in crypto, your transaction monitoring should exceed iGaming standards. If you’re in forex, your client suitability documentation should exceed crypto standards. Exceed your sector baseline to demonstrate genuine commitment to compliance.

Pro tip: Research your sector’s specific AML/CFT guidance from the Financial Action Task Force and EBA publications. When approaching banks, reference sector-specific controls you’ve implemented—this demonstrates you’re not just compliant in general, but compliant specifically for your industry’s risks.

Compliance Obligations and Onboarding Challenges

Onboarding a high-risk business into a bank account isn’t a straightforward process. Banks face regulatory obligations that turn your application into a compliance investigation. Understanding what they’re checking for helps you prepare strategically.

Banks must implement customer due diligence (CDD) before accepting any account. This means verifying your identity, understanding your business model, and assessing your money laundering risk. For high-risk sectors, due diligence deepens considerably, adding weeks to approval timelines.

Key compliance obligations banks manage include:

- Anti-money laundering (AML) screening against sanctions lists and politically exposed person databases

- Know Your Customer (KYC) procedures verifying beneficial ownership and management structure

- Transaction monitoring systems flagging unusual activity patterns after account opening

- Risk assessments evaluating whether your business generates acceptable risk levels

The EBA’s Guidelines on internal governance emphasise that compliance obligations are integral to governance frameworks, addressing challenges in onboarding through anti-money laundering measures and sound operational policies aligned with EU law.

Onboarding challenges emerge because banks balance regulatory compliance with commercial speed. They want your account, but regulators require evidence that they’ve done sufficient due diligence. If a bank approves your account too quickly, they risk regulatory sanctions.

Documentation requests often feel excessive. You’ll provide ownership documents, bank statements, business plans, and compliance policies. Banks request these because regulators scrutinise their onboarding files during examinations. If documentation is weak, banks face fines.

The EU’s AML/CFT directives form comprehensive legal frameworks requiring stringent customer due diligence, reporting, and risk assessment procedures to mitigate high-risk exposures effectively.

Onboarding delays frustrate high-risk businesses specifically. A standard retail account might approve in days; yours takes weeks or months. This isn’t malice—it’s regulatory necessity. Banks allocate limited compliance resources to higher-risk cases.

Source of funds documentation represents the largest challenge. Banks need credible evidence that your business generates revenue legitimately. For crypto businesses, this means wallet provenance documentation. For iGaming, this means player fund traceability. Vague or incomplete source documentation halts applications indefinitely.

The difference between approval and rejection often isn’t regulatory interpretation—it’s documentation quality. Banks approve when they can demonstrate due diligence to regulators; they reject when gaps exist.

Conflict of interest disclosures matter more for high-risk sectors. If your beneficial owners have connections to other high-risk businesses, banks flag this as potential structuring risk. Transparency about ownership networks accelerates approvals dramatically.

Regulatory reporting obligations extend beyond onboarding. Once approved, banks monitor your account continuously. Suspicious activity triggers reports to financial intelligence units. Understanding this ongoing scrutiny helps you structure transactions to avoid unnecessary flags.

Pro tip: During onboarding, provide documentation exceeding what banks request. Include voluntary compliance certifications, external audit reports, and detailed source of funds explanations. Over-documentation signals cooperation and dramatically improves approval likelihood.

Managing Risks and Avoiding Common Pitfalls

High-risk banking approval isn’t just about passing compliance checks—it’s about demonstrating you understand and manage the risks inherent to your business. Banks reject applications when they perceive unmanaged risk, not just regulatory non-compliance. Knowing what risks concern banks helps you position your business strategically.

Liquidity risk tops the list for high-risk sectors. Banks worry that transaction patterns may shift dramatically, leaving them exposed if your account suddenly becomes inactive or generates massive outflows. Demonstrate stable, predictable transaction volumes with clear seasonality explanations.

Common risk management pitfalls include:

- Inconsistent transaction patterns that suggest layering or structuring activities

- Rapid account scaling without operational infrastructure supporting volume growth

- Vague beneficial ownership structures that obscure actual control and decision-making authority

- Inadequate compliance policies that don’t match your actual operational complexity

Operational resilience matters increasingly to banks. The ECB’s supervisory priorities include strengthening banks’ resilience to macro-financial and geopolitical risks through regular stress testing and robust governance. Banks now assess whether your business can survive operational disruptions without creating banking instability.

Geopolitical risk exposure represents an emerging pitfall. If your business serves customers in sanctioned jurisdictions or operates near high-risk regions, banks flag this as concerning. Document your sanctions screening procedures and explain geographical restrictions carefully.

ESG risk assessment growing rapidly. Banks now identify and mitigate emerging risks linked to sustainability and climate-related factors. If your business operates in energy-intensive sectors or involves environmentally sensitive activities, expect banks to request sustainability disclosures and transition planning documents.

Transaction monitoring failures represent the largest pitfall banks observe. Many high-risk businesses implement weak transaction monitoring because they’re focused solely on compliance approvals. Once approved, inadequate monitoring triggers account reviews, restrictions, or closures months later.

Conflict of interest failures damage credibility. If your beneficial owners sit on boards of competitor businesses or hold conflicting financial interests, disclose this upfront. Banks trust transparency more than concealment.

The businesses that maintain banking relationships longest aren’t those with the cleanest records—they’re those that manage risks transparently and adjust controls proactively when circumstances change.

Regular compliance audits prevent drift. After account approval, many founders assume compliance obligations end. Instead, they intensify. Schedule annual compliance reviews to verify your controls still match your operational reality.

Documentation updates matter. When your business model changes—new products, new markets, new ownership—notify your bank immediately with updated compliance documentation. Banks discover undisclosed changes during transaction monitoring and view this as intentional deception.

Pro tip: Build internal compliance operations that exceed banking requirements rather than meeting them minimally. When banks audit your transaction monitoring systems and find you’ve implemented controls beyond what regulations require, they perceive reduced risk and are more likely to support account growth and product expansion.

Navigate EU Banking Regulations with Confidence and Expert Support

The complex landscape of EU banking regulations for high-risk industries demands more than just compliance awareness. With stringent requirements like detailed due diligence, sector-specific rules, and continuous risk management, many businesses face costly delays and frustrating rejections. Your challenge is clear: present a robust compliance framework and deliver impeccable documentation to meet evolving standards — all while securing reliable banking relationships.

At BankMyCapital, we understand these hurdles deeply and offer specialised solutions designed precisely for crypto, iGaming, adult entertainment, and forex sectors. Our expert consultancy helps you prepare and organise your compliance documentation, select the right jurisdiction, and leverage a network of over 50 trusted banking partners to fast-track approvals with Swiss-grade encryption ensuring your sensitive data is safe.

Discover how you can reduce rejection risk and accelerate onboarding by visiting our high-risk banking consultancy services page. Take control of your EU banking journey now and transform regulatory complexity into your competitive advantage.

Frequently Asked Questions

What are EU banking regulations?

EU banking regulations are rules established to ensure financial stability, protect customers, and guarantee that banks operate safely within the European Union. These regulations are vital for businesses, especially those classified as high-risk, as they influence the ability to form banking relationships.

How do banking regulations affect high-risk businesses?

Banking regulations impose stricter compliance requirements for high-risk businesses, affecting how banks conduct due diligence. These regulations demand stronger documentation and assurances regarding a business’s operations, compliance practices, and financial activities.

What are the main pillars of EU banking regulations?

The main pillars of EU banking regulations include prudential requirements for capital and risk management, operational standards for daily bank operations and customer fund protection, and governance rules that define the structure and decision-making processes within banks.

Why is ongoing compliance important for high-risk businesses?

Ongoing compliance is crucial as EU banking regulations are constantly evolving. Businesses must adapt to new guidelines to maintain banking relationships, demonstrating compliance and readiness for regulatory changes to avoid potential disruptions to their banking services.

Recommended

- Banking Compliance: Safeguarding High-Risk Sectors

- 6 Step High-Risk Business Banking Checklist for Success

- Resilient Banking Structure for High-Risk Businesses in 2026

- Top Banks Still Onboarding High Risk Clients in 2026

- Staying Compliant: Financial Automation and Regulatory Requirements – BankStatementFlow Blog

- How Lenders Assess Risk – Key Steps for Kiwis