Managing money across borders can turn into a real headache for high-risk crypto and iGaming businesses. As soon as you operate in multiple countries, you are up against complex regulations, messy cash flow, and stubborn banking restrictions. A multi-currency account solution gives you the power to hold, receive, and send funds in different currencies, making compliance and daily operations far simpler. Discover how this approach can replace complicated traditional banking setups and keep your business agile and compliant worldwide.

Key Takeaways

| Point | Details |

|---|---|

| Operational Efficiency | Multi-currency accounts streamline cross-border transactions, reducing the need for separate currency accounts and simplifying compliance reporting. |

| Cost Management | By consolidating transactions into one account, businesses can lower currency conversion fees and administrative costs while improving cash flow management. |

| Regulatory Compliance | These accounts facilitate easier adherence to AML, KYC, and other regulatory obligations, providing a clear audit trail that meets compliance standards. |

| Flexibility | With real-time balance updates and instant currency conversion, businesses can strategically manage their funds and respond to market conditions effectively. |

What Multi-Currency Accounts Offer

Multi-currency accounts simplify cross-border operations for high-risk businesses like crypto, iGaming, and forex firms. Rather than maintaining separate bank accounts for each currency, you consolidate everything into one account that holds multiple currencies simultaneously.

You gain immediate operational advantages:

- Hold funds in multiple currencies without constant conversions

- Receive payments directly in client or supplier currencies

- Send funds to vendors and staff in their preferred currencies

- Reduce currency conversion fees and associated costs

- Manage cash flow across jurisdictions more efficiently

The core benefit? Multi-currency accounts enable seamless transactions across borders, eliminating the friction that plagues traditional banking for high-risk sectors.

For crypto businesses processing payments in Bitcoin, Ethereum, or stablecoins alongside fiat currencies, this flexibility becomes essential. Your iGaming operation can receive player deposits in EUR, accept vendor payments in GBP, and hold operational reserves in USD—all within the same account structure.

Flexibility at your fingertips. You no longer juggle multiple banking relationships or wait for fund transfers between accounts. When you need to convert currencies, you do so at times that work for your cash flow strategy, not on someone else’s timeline.

The infrastructure removes barriers that typically plague high-risk sectors. Users can hold, receive, and spend multiple currencies without managing separate accounts, which simplifies compliance reporting and audit trails—critical advantages when regulators scrutinise your operations.

Real-world example: A crypto exchange operating across Europe needs to hold reserves in EUR, GBP, and USD for different regulatory jurisdictions. A traditional banking approach would require three separate accounts, three sets of compliance documentation, and three separate relationships to manage. A multi-currency account consolidates this into one manageable structure.

Multi-currency accounts reduce operational complexity whilst improving cash flow management—exactly what high-risk businesses need when navigating strict regulatory environments.

You also gain invoice flexibility. Crypto firms can invoice clients in the currency their jurisdiction requires whilst holding funds until conversion becomes strategically advantageous. This timing advantage directly improves profitability.

The operational transparency matters too. Single-account structures simplify your banking compliance, create cleaner audit trails for regulators, and reduce administrative overhead when you’re already managing complex international compliance requirements.

Here is a concise comparison of multi-currency accounts versus managing multiple single-currency accounts:

| Aspect | Multi-Currency Account | Multiple Single-Currency Accounts |

|---|---|---|

| Number of Relationships | One consolidated provider | Several providers per currency |

| Compliance Burden | Unified process | Separate for each account |

| Reporting & Audit | Single audit trail | Fragmented, complex reporting |

| Fee Structure | Consolidated fees, may be higher | Lower per account, higher total admin cost |

| Fund Availability | Instant cross-currency transfer | Delays due to account transfers |

| Regulatory Transparency | Easier to demonstrate compliance | Difficult to prove consolidated activity |

Pro tip: When evaluating multi-currency accounts, prioritise providers who specialise in high-risk sectors rather than mainstream banks—they understand your specific compliance needs and won’t freeze your account when processing legitimate crypto or iGaming transactions.

Core Features and Typical Structures

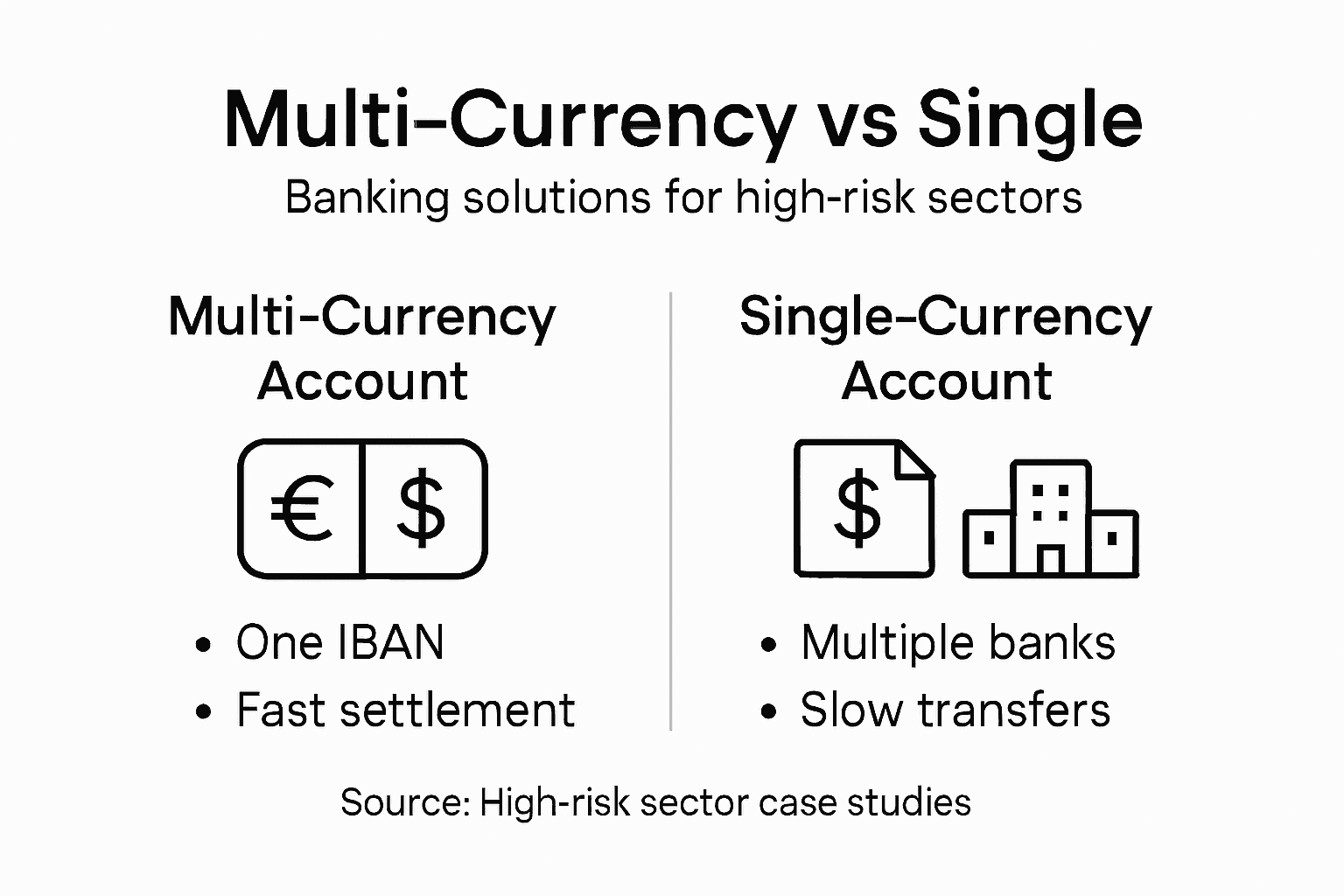

Modern multi-currency accounts operate on a unified architecture that simplifies what would otherwise require multiple banking relationships. The core structure consolidates all your currency balances under a single IBAN, giving you one account number instead of managing several.

Key features that matter for high-risk sectors:

- Single IBAN for all currency holdings and transactions

- Real-time balance updates across all currencies

- Instant currency conversion at competitive rates

- API-first integration for seamless payment processing

- Cross-border payment facilitation without intermediaries

- Compliance-ready frameworks supporting AML, PSD2, and GDPR

API integration proves critical for crypto and iGaming operations. Rather than manual processes, you connect your platform directly to the account through application programming interfaces, automating fund movements, conversions, and reconciliation.

The account typically supports major trading currencies. Multi-currency accounts enable holding USD, EUR, GBP, and JPY simultaneously, with real-time conversion capabilities when you need to rebalance across currencies.

For your compliance obligations, these accounts consolidate multiple currency balances under regulatory frameworks that meet European standards. This consolidation matters enormously when auditors examine your operations.

Conversion mechanics work transparently. You choose when to convert currencies based on market conditions and operational needs, rather than waiting for batch processing windows. A crypto exchange holding reserves can shift from EUR to GBP instantly when regulatory requirements or cash flow priorities shift.

Single-account structures with API integration reduce operational friction whilst maintaining regulatory compliance—the exact combination high-risk sectors require.

Transaction settlement happens faster than traditional banking routes. Cross-border payments that once took 3-5 days now complete within hours, directly reducing your working capital requirements.

For iGaming platforms, this means player withdrawals process immediately in their local currency without multiple conversion steps. Your vendors receive payments in their preferred currencies without delay. Your operational staff in different jurisdictions access funds in their local currency seamlessly.

The administrative overhead drops significantly. One account means one set of bank statements, one reconciliation process, and one compliance relationship instead of maintaining multiple accounts across different institutions.

Pro tip: Verify that your multi-currency provider offers API documentation meeting modern standards (REST, webhooks, real-time notifications)—this prevents integration delays and ensures your platform can automate compliance reporting without manual intervention.

High-Risk Industry Use Cases Explained

Multi-currency accounts solve specific operational challenges that plague crypto exchanges, iGaming platforms, and forex operations. Each sector faces distinct regulatory and transactional pressures that traditional banking cannot handle efficiently.

Cryptocurrency exchanges face the most complex multi-currency requirements. You receive deposits in Bitcoin, Ethereum, and stablecoins whilst maintaining fiat reserves across multiple jurisdictions. A single multi-currency account lets you hold operational reserves in EUR for European regulatory compliance, GBP for United Kingdom operations, and USD for international settlements—all without juggling separate bank accounts that traditional institutions refuse to open.

Funds settle faster too. Rather than waiting 3-5 business days for transfers between accounts, deposits consolidate instantly for internal operations and compliance reporting.

iGaming platforms operate across dozens of countries with different player currencies. Your players deposit in their local currency: EUR from Germany, GBP from the United Kingdom, SEK from Sweden. Multi-currency accounts mean you accept these deposits directly without conversion delays, improving player experience whilst reducing your currency conversion costs.

Vendor payments become straightforward. Your software developers expect payment in their local currency. Your payment processors require specific currencies for settlement. A multi-currency account handles all these requirements from one banking relationship rather than maintaining separate accounts for each currency.

Forex brokers and trading platforms operate across multiple regulatory jurisdictions simultaneously. Opening bank accounts for high-risk businesses requires compliance frameworks that multi-currency providers understand natively. You maintain segregated client funds in multiple currencies whilst meeting jurisdictional capital requirements.

Common use case patterns:

- Receive customer deposits in 12+ currencies simultaneously

- Pay vendors and contractors in their preferred currencies

- Maintain regulatory reserves in jurisdiction-specific currencies

- Convert between currencies strategically based on market conditions

- Automate compliance reporting across multiple currency balances

Multi-currency accounts transform high-risk sectors from managing currency complexity into managing business strategy.

Adult entertainment and content platforms benefit similarly. International content creators, affiliates, and payment processors operate across diverse regions with strict currency controls. Multi-currency accounts simplify international payments without the rejection barriers traditional banks impose.

Real-world impact: A crypto exchange previously maintained five separate bank accounts across different institutions, each requiring independent compliance documentation and audits. After consolidating to a multi-currency account, they reduced administrative overhead by 60% whilst improving settlement times from 3 days to 2 hours.

The regulatory compliance advantage matters equally. Understanding how to open banking relationships in the EU becomes dramatically simpler when one account consolidates all currency activity, creating transparent audit trails that regulators demand.

Pro tip: Before committing to a multi-currency provider, confirm they specialise in your specific sector—crypto, iGaming, forex, or adult content—because generic providers freeze accounts when transaction patterns don’t fit traditional business profiles.

Compliance, Security, and Legal Challenges

Multi-currency accounts introduce compliance responsibilities that differ fundamentally from traditional single-currency banking. High-risk sectors must understand these obligations before committing to any provider.

Anti-Money Laundering (AML) requirements apply across all currencies simultaneously. Your account must monitor transaction patterns in EUR, GBP, USD, and other currencies for suspicious activity. A single transaction might appear innocent in one currency but trigger alerts when analysed across your total account activity.

Know Your Customer (KYC) obligations become more complex. You must verify beneficial owners, source of funds, and customer legitimacy across multiple jurisdictions. Each currency jurisdiction adds regulatory layers.

Data security proves critical. Multi-currency accounts hold sensitive financial data across borders, requiring encryption standards that meet European regulations. Security in high-risk banking requires comprehensive compliance frameworks that protect client funds whilst maintaining regulatory transparency.

Regulatory challenges include:

- AML and KYC compliance across multiple jurisdictions

- Real-time transaction monitoring in multiple currencies

- Cross-border reporting requirements (FATCA, Common Reporting Standard)

- Currency control regulations in specific territories

- Data protection under GDPR and equivalent standards

- Audit trails meeting regulatory scrutiny standards

Traditional banks reject high-risk sectors partly because multi-currency compliance demands exceed standard banking infrastructure. They lack expertise in crypto transaction patterns, iGaming fund flows, or forex settlement complexities.

Specialised multi-currency providers succeed where traditional banks fail because they design compliance systems for high-risk sector realities, not generic business templates.

PSD2 (Payment Services Directive 2) regulations require strong customer authentication and fraud prevention across transactions. This applies regardless of currency, adding operational complexity that generic providers mishandle.

Legal liability questions arise too. If your multi-currency provider experiences a breach, who bears responsibility? The provider? Your business? Affected customers? Banking compliance for high-risk sectors requires contractual clarity on liability distribution that protects your business.

Transaction reversals create headaches. Currency movements mean a £1,000 reversal doesn’t equal a €1,000 settlement. Your compliance records must track exactly which currency was reversed and at what exchange rate.

Regulatory reporting timelines matter. Some jurisdictions demand transaction reports within 24 hours of settlement. Others require quarterly filings. Multi-currency accounts must automate this across multiple reporting frameworks simultaneously.

The audit trail becomes your strongest defence. When regulators question your operations, detailed records showing exactly when transactions settled, which currencies were involved, and why conversions occurred protect your business from accusations of impropriety.

Pro tip: Request your multi-currency provider’s compliance certifications and audit results before opening an account—specifically ask about their AML automation, KYC verification processes, and experience serving your sector, as generic certifications don’t guarantee high-risk sector competence.

Cost, Accessibility, and Alternative Solutions

Multi-currency accounts come with real costs that high-risk businesses must evaluate against their operational savings. Understanding pricing structures and alternatives helps you make informed decisions.

Typical fees include:

To clarify common fee types and strategic considerations for high-risk sectors, see the summary below:

| Fee/Consideration | Typical Amount | Impact on High-Risk Sectors |

|---|---|---|

| Monthly Account Maintenance | £15–£100+ | Increases with risk and volume |

| Currency Conversion Spread | 0.5–2% | Major cost when transacting at scale |

| Wire Transfer Charge | £10–£50/transfer | Relevant for cross-border vendors |

| API Integration Fee | Variable | Essential for platform automation |

| Compliance/KYC Set-up | One-time/variable | Often higher due to sector scrutiny |

| Inactive Account Fee | Variable | Penalises low-activity accounts |

- Monthly account maintenance (£15–£100+)

- Currency conversion spreads (0.5–2% above market rates)

- Wire transfer charges (£10–£50 per transaction)

- API integration fees (variable based on transaction volume)

- Compliance and KYC verification costs (one-time setup)

- Inactive account fees (if you don’t maintain minimum activity)

For high-volume crypto exchanges or iGaming platforms, conversion spreads become the largest expense. Converting £500,000 monthly across multiple currencies at 1.5% spread costs £7,500 monthly—potentially £90,000 annually.

Small operations face different economics. A £50,000 monthly transaction volume might pay £500 in spreads, making the convenience benefit worthwhile. The calculation changes entirely based on your scale.

Accessibility varies significantly. Traditional multi-currency providers reject crypto and iGaming businesses outright. Specialised providers charge premium fees precisely because they accept high-risk sectors. This creates a trade-off: pay more or accept banking rejection.

Alternative solutions exist but carry distinct disadvantages:

- Multiple single-currency accounts: Cheaper fees but requires managing separate bank relationships, compliance documentation, and audit trails

- Payment processor accounts: Easier approval but limited currency options and slower settlement times

- Cryptocurrency payment gateways: Excellent for crypto but can’t hold fiat reserves or pay traditional vendors

- Offshore banking structures: Complex setup, regulatory uncertainty, and higher compliance costs

- Fintech money platforms: Faster approvals but often refuse high-risk transactions after account opening

Multi-currency accounts cost more than traditional banking precisely because they solve problems traditional banking refuses to address.

Payment processors like Stripe or PayPal offer multi-currency features but with critical limitations. They freeze accounts when transaction patterns don’t fit their risk profiles—exactly the problem you’re trying to solve.

Offshore banking centres (Seychelles, Singapore, Cyprus) promise lower costs but introduce regulatory complexity that outweighs savings. You still need compliance infrastructure, and offshore structures attract greater regulatory scrutiny for high-risk sectors.

Cryptocurrency-only solutions fail because your iGaming platform, forex operation, or crypto exchange needs fiat reserves, staff payments in local currencies, and vendor settlements. Cryptocurrency-only accounts don’t provide this functionality.

The real cost comparison must include operational overhead. Managing five separate bank accounts requires dedicated administrative staff, separate compliance reporting, and independent audit processes. One consolidated multi-currency account reduces headcount requirements and automates reporting.

A practical calculation: If maintaining separate accounts costs £2,000 monthly in administrative overhead and you save £1,500 monthly through consolidated compliance, a £800 monthly multi-currency fee becomes cost-neutral immediately.

Pro tip: Negotiate fees based on your transaction volume and sector experience—providers competing for high-risk business often discount spreads by 0.5–1% for platforms processing £500,000+ monthly, transforming your cost structure entirely.

Unlock Seamless Banking Solutions for High-Risk Sectors with BankMyCapital

Managing multi-currency accounts in high-risk industries such as crypto, iGaming, and forex is a complex challenge. You face the constant struggle of navigating regulatory compliance, reducing operational friction, and avoiding costly currency conversion fees while maintaining transparency for audits. The article highlights key pain points including fragmented banking relationships, slow fund settlements, and the critical need for specialised providers who understand your sector’s unique requirements.

BankMyCapital offers exactly what you need: tailored banking solutions designed for high-risk businesses operating within the European Union and offshore jurisdictions. By leveraging our network of over 50 vetted banking partners and EMIs, we dramatically reduce rejection risks and accelerate onboarding to just 2-3 weeks. Our services include comprehensive legal and compliance support that align perfectly with the demands of multi-currency accounts as discussed in the article. Whether it is facilitating your banking relationships, navigating licensing challenges, or implementing secure payment processing, BankMyCapital delivers a transparent, secure, and efficient pathway that transforms operational complexity into strategic advantage.

Are you ready to bypass traditional banking barriers and gain control over your financial operations with a provider who truly understands your industry? Discover how BankMyCapital’s specialised expertise can simplify your multi-currency account challenges and enhance your global reach. Take the next step today by visiting BankMyCapital and turning regulatory obstacles into opportunities.

Frequently Asked Questions

What are the main advantages of using a multi-currency account for high-risk businesses?

Multi-currency accounts allow businesses to hold funds in multiple currencies, receive payments directly in client or supplier currencies, reduce currency conversion fees, and manage cash flow across different jurisdictions more efficiently.

How do multi-currency accounts simplify compliance for high-risk sectors?

By consolidating all currency balances under a single IBAN, multi-currency accounts reduce administrative overhead, create cleaner audit trails, and simplify compliance reporting, which is crucial for high-risk jurisdictions.

Can multi-currency accounts assist with fee reduction for cross-border transactions?

Yes, multi-currency accounts can reduce operational costs by consolidating transaction fees and providing instant currency conversion, thereby eliminating the need for multiple banking relationships and their associated fees.

What compliance challenges do high-risk sectors face when using multi-currency accounts?

High-risk sectors need to navigate complex AML and KYC requirements, data protection regulations, and real-time transaction monitoring across multiple currencies, all of which can complicate compliance and regulatory reporting.