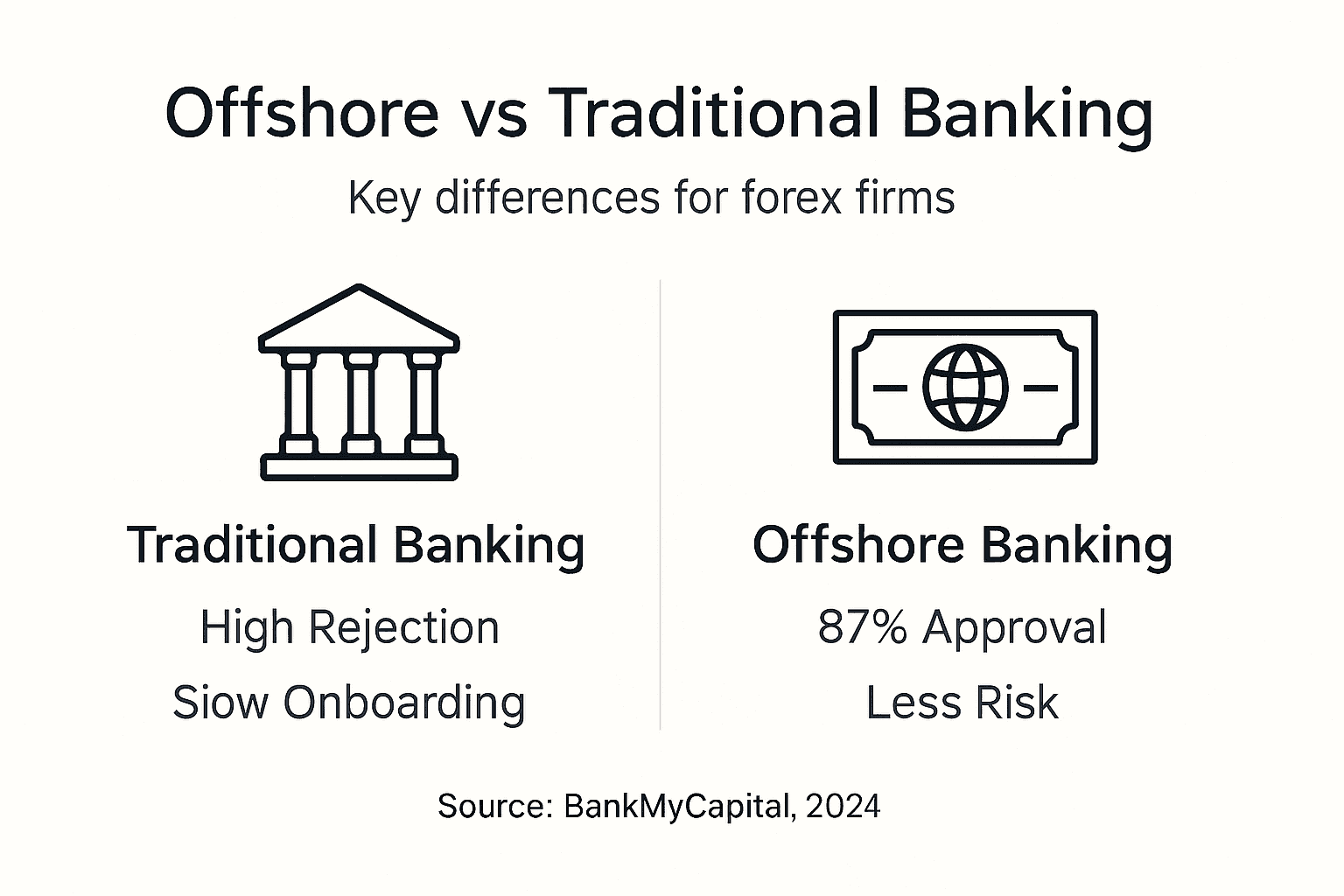

European forex firms routinely face rejection rates exceeding 60% when applying for traditional banking accounts, alongside onboarding processes stretching 6 to 8 weeks. Offshore banking offers a strategic alternative, delivering faster approvals, enhanced compliance frameworks, and operational agility tailored specifically for high-risk forex operations. This guide clarifies how offshore banking works, which jurisdictions excel, and how to implement compliant, efficient offshore solutions that reduce disruption and accelerate growth.

Key Takeaways

| Point | Details |

|---|---|

| Lower Rejection Rates | Offshore banking reduces forex account rejection rates from 60% with traditional banks to approximately 13% with specialized providers. |

| Faster Onboarding | Specialized offshore banks complete onboarding in 2 to 3 weeks compared to 6 to 8 weeks for traditional European institutions. |

| Risk Diversification | Diversifying banking relationships across offshore jurisdictions cuts service interruptions by up to 50%. |

| Compliance Strength | Offshore banks enforce robust AML and KYC standards aligned with FATF guidelines, ensuring regulatory adherence. |

| Operational Efficiency | Multi-currency support and flexible payment processing enhance transaction speeds and client payout reliability. |

Understanding Offshore Banking in Forex: Definition and Mechanism

Offshore banking involves establishing business accounts in jurisdictions outside your firm’s home country to access specialized banking infrastructure, regulatory flexibility, and enhanced privacy protections. For forex trading firms, this means holding accounts in locations that accommodate high-risk business models while maintaining strict compliance standards.

Offshore accounts facilitate critical forex operations such as multi-currency holdings, liquidity management, and cross-border transaction processing. Unlike traditional banks that often reject forex applications due to perceived risk, offshore institutions specialize in serving sectors like forex, crypto, and iGaming. They understand the unique compliance challenges and operational demands these industries face.

Three core mechanisms drive offshore banking advantages:

- Regulatory Arbitrage: Jurisdictions offering balanced regulation enable forex operations without excessive administrative burdens while maintaining AML and KYC enforcement.

- Enhanced Privacy: Offshore banks provide confidentiality protections within legal frameworks, safeguarding business strategies and client data.

- Specialized Infrastructure: Banking platforms designed for high-volume, multi-currency transactions improve processing speed and reduce technical failures.

The primary difference between offshore and onshore banking centers on acceptance criteria and service agility. Traditional European banks apply rigid risk assessments that frequently disqualify forex firms. Offshore crypto license jurisdictions recognize forex as legitimate commerce, building banking systems that support multi-jurisdictional account setups optimizing regulatory compliance and operational flexibility.

Offshore banking is not about evading taxes or hiding assets. It is a legitimate compliance and operational strategy that enables forex firms to access banking services otherwise unavailable through traditional channels.

Jurisdictional Advantages: Choosing the Right Offshore Location for Forex

Selecting the optimal offshore jurisdiction requires balancing regulatory tolerance, banking infrastructure quality, and compliance framework strength. Popular jurisdictions among forex firms include Seychelles, Mauritius, Belize, and the Cayman Islands, each offering distinct advantages.

Seychelles provides a favorable regulatory environment with streamlined licensing processes and banks experienced in high-risk sectors. Mauritius combines African market access with robust financial infrastructure and bilateral tax treaties. Belize offers cost-effective licensing and minimal compliance overhead while maintaining international banking standards. The Cayman Islands deliver premium banking services with strong legal frameworks, though at higher operational costs.

When evaluating jurisdictions, prioritize these criteria:

- Regulatory Framework: Ensure the jurisdiction enforces AML and KYC standards recognized by international bodies like FATF while accommodating forex business models.

- Banking Infrastructure: Assess the availability of multi-currency accounts, payment gateway integrations, and technological platforms supporting high-frequency transactions.

- Licensing Efficiency: Jurisdictions offering clear licensing pathways reduce setup time and legal uncertainty.

- Political and Economic Stability: Stable jurisdictions minimize risks of sudden regulatory changes or banking service disruptions.

Operational infrastructure significantly impacts forex performance. Jurisdictions with mature payment processing ecosystems enable seamless client deposits, withdrawals, and inter-bank transfers. Multi-currency support eliminates conversion delays and reduces transaction costs, critical for firms operating across global markets.

Pro Tip: Match your jurisdiction choice to your primary client base geography. If serving European clients, consider jurisdictions with EU payment network access to reduce cross-border friction.

Exploring best offshore banks for forex reveals that specialized institutions understand forex compliance needs better than generalist banks. These banks offer tailored account structures, dedicated relationship managers, and expedited onboarding processes. Understanding offshore jurisdiction benefits helps firms align banking strategies with business expansion goals and regulatory obligations.

Compliance and Risk Management in Offshore Forex Banking

Compliance forms the foundation of sustainable offshore banking relationships. Offshore banks enforce strict AML and KYC standards mandated by global regulators like the Financial Action Task Force. These protocols require detailed client verification, transaction monitoring, and suspicious activity reporting identical to requirements in traditional banking.

Legal frameworks in reputable offshore jurisdictions criminalize money laundering, terrorist financing, and financial fraud. Banks implement robust compliance programs including:

- Customer Due Diligence: Comprehensive identity verification, beneficial ownership disclosure, and source of funds documentation.

- Transaction Monitoring: Automated systems flagging unusual transaction patterns for manual review and potential regulatory reporting.

- Ongoing Compliance: Regular account reviews, updated documentation requests, and adherence to evolving regulatory standards.

- Regulatory Reporting: Timely submission of suspicious transaction reports to local financial intelligence units.

Offshore forex banking carries unique risks requiring proactive management. Banking service interruptions can occur when jurisdictions tighten regulations or when individual banks reassess risk appetites. Reputational risks arise from misconceptions about offshore banking legality, potentially affecting client trust or partnership negotiations.

Diversification mitigates these risks effectively. Offshore forex banking reduces service interruptions by up to 50% when diversifying banking partners across jurisdictions. Maintaining accounts in three to four jurisdictions ensures operational continuity if one banking relationship encounters difficulties.

Pro Tip: Establish primary and backup banking relationships before operational needs become urgent. Onboarding takes weeks even with specialized providers, so plan ahead to avoid cash flow disruptions.

Implementing comprehensive banking compliance for high-risk forex processes protects your firm from regulatory penalties and banking terminations. Compliance is not a checkbox exercise but an ongoing operational priority requiring dedicated resources and expert guidance.

Operational Benefits and Process Improvements Through Offshore Banking

Offshore banking delivers tangible operational advantages that directly improve forex firm performance and client satisfaction. The most immediate benefit is accelerated onboarding, with specialized offshore banks completing account setup in 2 to 3 weeks compared to 6 to 8 weeks for traditional institutions. This speed enables faster market entry and quicker revenue generation.

Payment processing efficiency increases substantially. Offshore banks serving forex firms offer:

- Multi-Currency Account Structures: Hold balances in EUR, USD, GBP, and other major currencies without conversion delays or excessive fees.

- Cross-Border Payment Optimization: Direct access to SWIFT, SEPA, and regional payment networks reduces transaction times from days to hours.

- Higher Transaction Limits: Offshore accounts accommodate larger individual transactions and daily volumes than standard business accounts.

- Flexible Payment Gateway Integration: APIs and direct integrations with forex platforms streamline client deposits and withdrawals.

Relationship management with offshore banks provides customized solutions unavailable from traditional institutions. Dedicated account managers understand forex operational cycles, margin requirements, and liquidity management needs. They proactively suggest account structure optimizations and facilitate introductions to complementary service providers like payment processors or liquidity providers.

Operational scalability improves as offshore banking infrastructure supports business expansion without requiring new banking applications. Adding new trading instruments, expanding into new geographic markets, or increasing transaction volumes occurs within existing account frameworks. This flexibility reduces administrative overhead and accelerates strategic initiatives.

Client transaction flows become more reliable with offshore banking. Faster payment processing improves trader satisfaction, reducing complaints and support tickets. Reliable deposit and withdrawal systems build trust, encouraging higher trading volumes and client retention. The cumulative effect enhances your firm’s reputation and competitive positioning.

To open offshore forex account efficiently, prepare comprehensive documentation upfront and engage with banks experienced in forex operations to maximize these operational benefits.

Common Misconceptions About Offshore Banking for Forex Firms

Several persistent myths prevent forex firms from exploring offshore banking strategically. Addressing these misconceptions clarifies the legitimate value offshore banking provides.

Myth: Offshore Banking Equals Tax Evasion

Offshore banking is a legal business strategy used for compliance optimization, operational efficiency, and risk diversification. Firms remain obligated to report income and pay taxes in their home jurisdictions. Offshore accounts simply provide banking infrastructure better suited to forex operations than domestic alternatives.

Myth: Offshore Banks Lack Robust AML and KYC Controls

Reputable offshore banks enforce compliance standards matching or exceeding traditional institutions. They implement comprehensive KYC procedures, transaction monitoring systems, and regulatory reporting to satisfy international standards. Jurisdictions with weak compliance attract regulatory scrutiny and banking partner exits, incentivizing strong enforcement.

Myth: Offshore Banking Eliminates All Operational Risk

While offshore banking reduces certain risks like domestic banking access denial, it introduces others requiring active management. Jurisdictional regulatory changes, currency fluctuations, and individual bank policy shifts demand diversification and ongoing relationship monitoring. Offshore banking complements traditional banking rather than replacing it entirely.

Myth: Offshore Banking Has High Rejection Rates

Specialized offshore banks achieve approval rates near 87% for forex firms by understanding industry-specific risk profiles and compliance requirements. These institutions design account structures specifically for high-risk sectors, reducing rejection likelihood compared to traditional banks applying generic risk assessments.

Myth: Only Large Firms Benefit from Offshore Banking

Small and medium forex firms gain proportionally greater advantages from offshore banking. Reduced onboarding times, lower rejection rates, and flexible account structures help emerging firms compete with established players. Offshore banking democratizes access to professional banking infrastructure previously available only to large institutions.

Understanding these realities positions offshore banking as a strategic tool rather than a dubious workaround. European forex firms using offshore solutions legally and compliantly gain competitive advantages while maintaining full regulatory adherence.

Comparing Offshore and Traditional Banking for Forex Firms

Data-driven comparison reveals clear performance differences between offshore and traditional banking options for forex operations.

| Criteria | Traditional Banking | Offshore Banking |

|---|---|---|

| Application Rejection Rate | 60% | 13% |

| Onboarding Timeline | 6 to 8 weeks | 2 to 3 weeks |

| Multi-Currency Support | Limited, high conversion fees | Native multi-currency accounts |

| Compliance Complexity | Rigid, sector-averse frameworks | Flexible yet robust, sector-experienced |

| Relationship Management | Generic business banking | Dedicated forex industry managers |

| Transaction Limits | Conservative, frequent reviews | Higher limits, scalable structures |

| Geographic Flexibility | Domestic focus | Multi-jurisdictional servicing |

| Service Interruption Risk | Moderate, policy-dependent | Lower with diversification |

Rejection rates represent the most significant operational difference. Traditional banks classify forex as high-risk, applying conservative underwriting that disqualifies 60% of applications. Offshore banks specializing in forex understand the business model, evaluating applications based on compliance documentation quality and operational transparency rather than sector categorization alone.

Onboarding speed impacts time to market and opportunity costs. Six to eight weeks waiting for traditional bank approval delays revenue generation and market positioning. Offshore banks compress this timeline to 2 to 3 weeks through streamlined processes and dedicated onboarding teams.

Compliance complexity varies significantly. Traditional banks impose rigid requirements designed for conventional businesses, creating bottlenecks when forex-specific documentation does not fit standard templates. Offshore banks implement strong AML and KYC frameworks but customize documentation requirements to forex operational realities.

Risk profiles differ structurally. Traditional banking concentrates risk in single-jurisdiction relationships vulnerable to domestic regulatory shifts. Offshore banking distributes risk across multiple jurisdictions, reducing disruption likelihood but requiring active relationship management and compliance monitoring across locations.

Understanding offshore banking vs traditional banking tradeoffs enables informed strategic decisions. Evaluating offshore vs onshore bank accounts clarifies which account types align with specific operational priorities and risk tolerances.

Practical Guide: Implementing Offshore Banking Solutions in Forex

Successfully implementing offshore banking requires systematic planning and expert execution. Follow these steps to maximize approval rates and operational benefits.

-

Assess Banking Needs and Risk Profile: Document transaction volumes, currency requirements, geographic markets served, and compliance capabilities. Identify specific pain points with current banking arrangements that offshore solutions should address.

-

Select Target Jurisdictions: Match jurisdictions to operational requirements considering regulatory frameworks, banking infrastructure quality, and client geography. Prioritize jurisdictions with proven forex banking expertise and stable political environments.

-

Engage Specialized Consultants: Partner with advisors experienced in offshore forex banking to navigate jurisdiction-specific requirements and bank introductions. Expert guidance reduces application errors and accelerates approvals.

-

Prepare Comprehensive Documentation: Compile AML and KYC materials including beneficial ownership disclosures, source of funds evidence, business plans, compliance procedures, and regulatory licenses. Tailor documentation to jurisdiction-specific banking requirements.

-

Implement Diversified Banking Relationships: Establish accounts in three to four jurisdictions to mitigate service interruption risks. Balance primary operational accounts with backup relationships activated during disruptions.

-

Monitor Compliance and Relationships: Schedule quarterly reviews of banking relationships, compliance documentation currency, and regulatory changes in each jurisdiction. Proactive monitoring prevents surprise account closures or service restrictions.

Pro Tip: Budget 10% to 15% more time than estimated timelines for offshore account setup. Regulatory reviews and documentation clarifications occasionally extend processes beyond initial projections.

Following a structured open offshore forex account guide reduces implementation friction. Leveraging a high-risk bank onboarding guide ensures documentation completeness and compliance strength. Using a comprehensive bank account opening checklist maximizes approval likelihood and minimizes delays.

Explore Expert Offshore Banking Solutions for Forex Firms

Navigating offshore banking complexities requires specialized expertise and proven banking relationships. BankMyCapital offers tailored guidance helping forex firms secure compliant, efficient offshore banking solutions. Our network spans over 50 pre-vetted banking partners across multiple jurisdictions, delivering 87% approval rates and 2 to 3 week onboarding timelines.

We provide comprehensive support including jurisdiction selection, documentation preparation, compliance framework development, and ongoing relationship management. Our high-risk bank compliance guidance helps firms build robust AML and KYC procedures satisfying international standards. Access our high-risk business banking checklist to prepare applications maximizing approval chances. Explore our offshore banking solutions designed specifically for forex firms seeking operational flexibility and reduced rejection risk.

Frequently Asked Questions About Offshore Banking for Forex

What are the key compliance documents required for opening an offshore forex account?

Offshore banks require comprehensive KYC documentation including passport copies and proof of address for all beneficial owners, detailed business plans explaining forex operations and target markets, source of funds evidence demonstrating capital legitimacy, AML and KYC policy documents outlining internal compliance procedures, and valid forex licenses from home or target jurisdictions. Some banks request additional materials like audited financial statements or reference letters from existing banking relationships.

How does offshore banking affect tax obligations for European forex firms?

Offshore banking does not eliminate tax obligations in your home jurisdiction. European forex firms remain liable for corporate income tax, VAT, and other applicable taxes regardless of where banking accounts are located. Offshore accounts must be reported to tax authorities through mechanisms like Common Reporting Standard disclosures. Consult tax advisors to ensure full compliance with home country reporting requirements while leveraging offshore banking for operational benefits.

Can offshore banking improve transaction speeds and client payouts in forex trading?

Yes, offshore banks specializing in forex offer superior payment processing infrastructure compared to traditional institutions. Multi-currency accounts eliminate conversion delays, direct payment network access reduces cross-border transaction times from days to hours, and higher transaction limits accommodate large client withdrawals without manual reviews. These improvements increase client satisfaction and reduce support overhead related to payment delays.

Is it legal for European forex firms to hold accounts in multiple jurisdictions?

Holding accounts in multiple jurisdictions is entirely legal provided firms comply with reporting requirements in each jurisdiction and their home country. Multi-jurisdictional banking is a standard risk management practice reducing dependence on single banking relationships. Ensure proper tax reporting, maintain transparent ownership structures, and comply with AML regulations in all jurisdictions to operate legally and sustainably.