Most business owners assume payment processing works the same for everyone, but if you operate in crypto, iGaming, or adult entertainment, you face a completely different landscape. Traditional processors reject high-risk sectors at rates exceeding 70%, leaving operators scrambling for alternatives. This guide breaks down what makes payment processing high risk, how the mechanics differ from standard accounts, and practical steps to secure reliable banking relationships that support growth rather than stifle it.

Key takeaways

| Point | Details |

|---|---|

| High-risk criteria | Businesses with high chargebacks, heavy regulation, or cross-border payments need specialised processing. |

| Complexity and costs | Expect more verification, rolling reserves, and fees up to twice the standard rates. |

| Chargeback risk | Keeping chargebacks below card scheme thresholds is essential to keeping your account open. |

| Account structure | Hybrid setups using onshore, offshore, and crypto can minimise cost and risk. |

| Compliance is ongoing | Maintaining compliance and documentation is vital to avoid blacklists and operational disruption. |

What defines a high-risk business?

From a payment processor’s perspective, you’re high risk if your business model triggers frequent chargebacks, operates under complex regulations, or processes international payments across multiple jurisdictions. Industries like crypto, iGaming, and adult entertainment face classification as high risk because they combine all three factors.

Typical high-risk sectors share common characteristics. Crypto exchanges handle volatile assets and cross-border transactions. Online gaming and gambling sites face strict licensing requirements and age verification challenges. Adult entertainment platforms deal with subscription billing disputes and content-related chargebacks.

Several risk factors push businesses into this category:

- Chargeback rates exceeding 1% of total transactions

- Operating in jurisdictions with evolving or unclear regulatory frameworks

- Subscription-based or recurring billing models that increase dispute likelihood

- Cross-border sales requiring currency conversion and international compliance

- Products or services considered reputationally sensitive by traditional banks

Traditional processors avoid these sectors because the financial exposure outweighs potential profit. Banks face regulatory scrutiny when serving high-risk clients, and elevated chargeback rates threaten their standing with card networks like Visa and Mastercard.

Pro Tip: Present accurate company information and demonstrate a robust compliance posture from your first application. Processors flag inconsistencies immediately, and clean documentation significantly improves approval odds.

Understanding your high-risk merchant account criteria helps you prepare applications that address processor concerns upfront rather than triggering instant rejection.

How high-risk payment processing works: mechanics and fees

The application process for high-risk accounts involves intensive merchant underwriting. Processors examine your business registration documents, conduct Know Your Business and Know Your Customer checks, review your website content, and analyse financial statements. They’re assessing whether your operation can sustain the elevated risk profile.

Approval involves rigorous KYB/KYC, rolling reserves of 5-15% held for 90-180 days, and ongoing transaction monitoring. Settlement times stretch longer than standard accounts, often taking three to seven business days instead of next-day funding.

Fee structures differ dramatically from conventional processing:

| Account Type | Setup Fee | Transaction Fee | Chargeback Fee | Rolling Reserve |

|---|---|---|---|---|

| Standard Merchant | £0-£200 | 1.5-2.9% + £0.20 | £15-£25 | None |

| High-Risk Merchant | £500-£2,000 | 4-8% + £0.25-£0.50 | £25-£100 | 5-15% for 90-180 days |

These costs add up quickly. Fees and reserves can reach up to 15% effective cost, crushing margins for businesses operating on tight budgets. Transaction fees alone run two to three times higher than standard rates, and chargeback penalties escalate with each dispute.

Chargeback monitoring becomes intensive. Processors track your ratio weekly, and exceeding thresholds triggers account reviews or immediate termination. You’ll face monthly reporting requirements and regular compliance audits that standard merchants never encounter.

Adult sector merchants face rejection rates exceeding 70% during initial underwriting, with only specialised processors willing to assume the risk profile.

Pro Tip: Negotiate fees by demonstrating lower chargeback history or committing to higher processing volumes. Processors offer better terms when you prove your operation manages risk effectively.

Implementing best practices for fee management helps you reduce costs over time, and understanding the full scope of payment processing options ensures you’re not overpaying for services.

Understanding chargebacks and risk mitigation

A chargeback occurs when a customer disputes a transaction with their card issuer, forcing the processor to reverse the payment and return funds. For high-risk sectors, chargebacks stem from buyer’s remorse, subscription cancellation disputes, unauthorised use claims, and content dissatisfaction.

Card schemes set strict thresholds. Visa’s limit sits at 0.9-1% of monthly transactions, whilst Mastercard enforces similar standards. Exceed these ratios and you face escalating fines, enhanced monitoring programmes, or complete loss of processing privileges.

High-risk sectors average 2-5% chargeback rates, with adult entertainment at 3.5% and healthy merchants maintaining rates under 0.5%. This gap explains why processors demand rolling reserves and charge premium fees.

Common chargeback triggers for high-risk businesses include:

- Unclear billing descriptors that customers don’t recognise on statements

- Inadequate customer service response times for cancellation requests

- Subscription renewals without sufficient advance notice

- Product or service quality falling short of marketing promises

- Delayed delivery or access to digital content

Processors deploy multiple risk mitigation tools. Chargeback alerts notify you before disputes become official, giving you time to issue refunds and avoid ratio damage. Representment services help you fight illegitimate disputes with evidence packages. Anti-fraud checks screen transactions in real-time, blocking suspicious patterns before they process.

Pro Tip: Implement a multi-processor cascading setup to avoid single-point failure. If one account faces restrictions, transactions automatically route to backup processors, preventing revenue loss and blacklist risk.

Exploring comprehensive solutions for chargeback reduction protects your processing relationships and keeps your business operational.

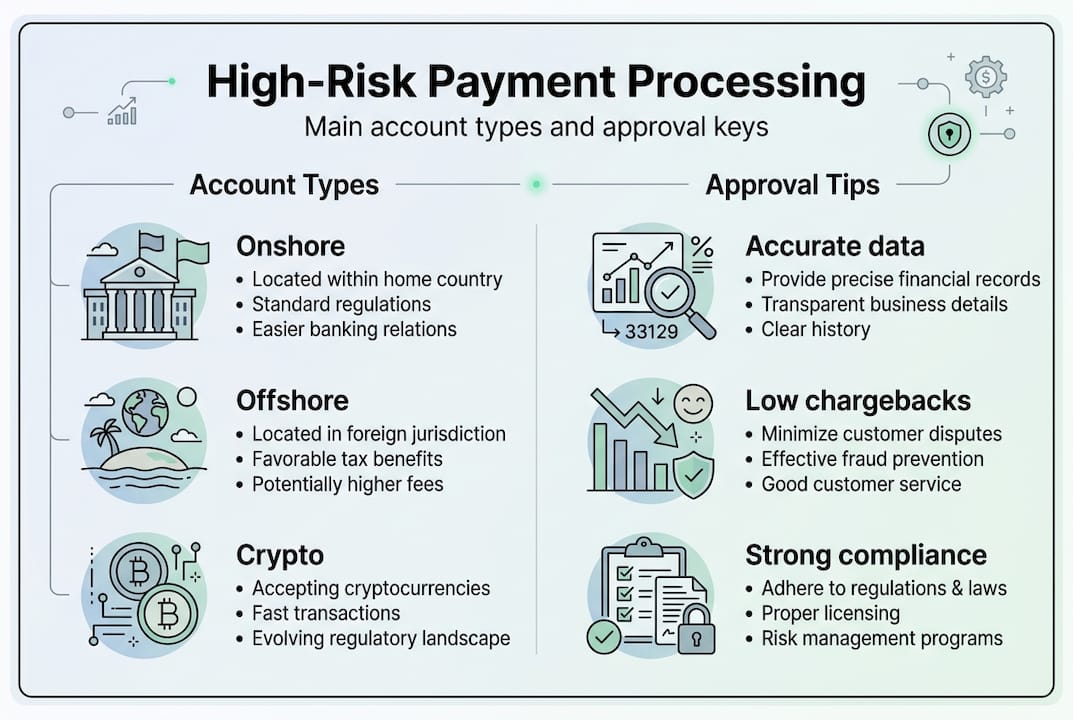

Onshore, offshore, and cryptocurrency: choosing the right setup

Onshore accounts operate within your home jurisdiction, offering regulatory familiarity and easier legal recourse. Offshore accounts establish processing relationships in jurisdictions with more flexible high-risk policies, often providing faster approvals but introducing currency conversion complexity.

| Setup Type | Approval Speed | Fee Range | Regulatory Oversight | Best For |

|---|---|---|---|---|

| Onshore | 4-8 weeks | 4-6% + fees | High | Established businesses with clean history |

| Offshore | 2-4 weeks | 5-8% + fees | Moderate | Startups or businesses facing domestic rejection |

| Cryptocurrency | 1-2 weeks | 0.5-1% | Evolving | Tech-savvy audiences, global transactions |

Offshore accounts carry higher risk and fees but sometimes faster settlements, whilst crypto eliminates chargebacks entirely through irreversible transactions. Each option presents distinct trade-offs.

Multi-MID setups distribute transaction volume across multiple merchant IDs, preventing any single account from hitting processing limits or chargeback thresholds. Cascading configurations automatically route failed transactions to alternative processors, maximising approval rates.

Cryptocurrency offers compelling advantages for high-risk sectors. Transactions settle instantly, eliminating chargeback risk entirely. Processing fees drop to 0.5-1% compared to 4-8% for traditional cards. Global transactions process without currency conversion headaches or international banking restrictions.

Crypto risks include price volatility affecting settlement values, evolving compliance requirements across jurisdictions, and customer education barriers. Many consumers remain unfamiliar with cryptocurrency payments, limiting adoption rates.

Traditional banks rarely serve high-risk merchants, pushing operators towards aggregator accounts that offer speed but less control, or dedicated accounts providing stability at the cost of longer approval times. Hybrid setups combining card processing with crypto acceptance increasingly represent the optimal approach.

Comparing offshore vs onshore options helps you select the structure matching your risk tolerance, and understanding benefits of offshore banking clarifies when international accounts make strategic sense.

Key compliance considerations for high-risk payment processing

Compliance never stops after initial approval. Processors conduct ongoing KYC and KYB updates, reviewing business model changes, ownership transfers, and website content modifications. They’re protecting their own relationships with card networks and banking partners.

The MATCH list represents the primary international blacklist for risky merchants. MATCH list blacklisting occurs after account termination for non-compliance, making future approvals nearly impossible. Once listed, you face five years of processing difficulties across all providers.

Core compliance steps for maintaining healthy high-risk merchant accounts:

- Maintain transparent billing descriptors that clearly identify your business

- Implement robust age verification systems for restricted content or services

- Provide detailed terms of service and refund policies prominently on your site

- Respond to customer service enquiries within 24 hours to prevent disputes

- Update processor documentation immediately when business operations change

- Conduct quarterly internal audits of transaction patterns and chargeback triggers

- Maintain rolling reserves as required without requesting early release

Site audits verify your website matches the business model described in your application. Processors flag discrepancies between approved activities and actual offerings, triggering account reviews or termination.

Clean site presentation and clear disclosure of business practices mitigate underwriting rejections, whilst empirical evidence of low chargeback history overcomes initial risk concerns.

Third-party validation services provide independent verification of your compliance posture, strengthening applications and renewal requests. These reports demonstrate proactive risk management to sceptical processors.

Proactive documentation prevents costly disruptions. Maintain organised records of all customer communications, transaction disputes, and resolution attempts. When processors request information during reviews, immediate comprehensive responses preserve account standing.

Following detailed compliance steps for approval ensures your accounts remain operational and your business continues processing without interruption.

Expert help for high-risk payment processing

Navigating account setup, compliance requirements, and chargeback management demands specialised knowledge that most business owners lack. The complexity of high-risk payment processing means mistakes cost thousands in lost revenue and months in approval delays.

Bank My Capital offers specialised payment processing solutions designed specifically for crypto, iGaming, and adult entertainment sectors. Our network of over 50 pre-vetted banking partners and EMIs provides options when traditional channels close, and our 87% approval rate demonstrates the value of expert guidance through the application process.

We provide tailored industry solutions addressing the unique challenges each sector faces, from crypto exchange compliance to iGaming licence acquisition. Our approach combines rapid onboarding timelines of two to three weeks with comprehensive legal and compliance support that keeps your accounts operational long-term.

Exploring diverse banking approaches helps you understand which structures best serve your specific business model, whether you need onshore stability, offshore flexibility, or hybrid solutions combining multiple processing channels.

Exploring payment processing options for high-risk sectors

High-risk businesses access payment processing methods spanning traditional and emerging technologies, each suited to different operational models. Card payments remain dominant for customer familiarity, but high-risk merchants face elevated processing fees and stricter underwriting. Enhanced verification protocols like 3D Secure 2.0 reduce fraud but add friction to checkout flows. Expect processing fees between 3% and 8%, significantly higher than standard merchant rates, plus rolling reserves that lock portions of revenue for chargeback protection.

E-wallets and digital payment platforms offer faster settlement and reduced chargeback exposure. Solutions like Skrill, Neteller, and PayPal (where available) appeal to iGaming customers familiar with these interfaces. However, many digital wallet providers explicitly exclude high-risk sectors or impose strict transaction limits. Those accepting high-risk merchants typically require extensive documentation and maintain the right to freeze accounts during compliance reviews.

Crypto payment gateways have emerged as powerful alternatives for businesses comfortable with digital assets. Bitcoin, Ethereum, and stablecoin processors eliminate chargeback risk entirely, offer near-instant settlement, and bypass traditional banking restrictions. Fees range from 0.5% to 2%, substantially lower than card processing. The trade-offs include price volatility for non-stablecoin transactions, regulatory uncertainty in some jurisdictions, and customer adoption barriers outside crypto-native audiences.

Bank transfers and SEPA options provide cost-effective solutions for larger transactions common in Forex trading. Direct bank connectivity ensures regulatory compliance and eliminates intermediary fees, but settlement times extend to 1-3 business days. This method suits businesses with established customer relationships where immediate payment confirmation isn’t critical. Consider these key advantages and limitations:

- Card payments: Widest acceptance but highest fees and chargeback risk

- E-wallets: Faster settlement with moderate fees but sector restrictions

- Crypto gateways: Lowest fees and no chargebacks but volatility concerns

- Bank transfers: Cost-effective for large amounts but slower processing

Your optimal mix depends on customer preferences, transaction sizes, and risk tolerance. Most successful high-risk operators deploy multiple payment methods to maximise conversion while managing exposure.

EU vs offshore: Jurisdictions and account options

To round out your understanding, consider where to set up your account. Location shapes your fees, terms, banking reliability, and the level of consumer protection your customers receive.

EU merchant accounts are issued by acquirers operating under European Economic Area regulation. They offer strong consumer protection frameworks, access to SEPA payments, and credibility with card schemes. Cyprus and Malta are the most common EU jurisdictions for high-risk processing, offering EU legal frameworks with relative flexibility compared to larger EU markets.

Offshore merchant accounts are issued in jurisdictions such as Seychelles, Belize, or Vanuatu. They offer higher approval rates for businesses that EU acquirers reject outright, fewer restrictions on business model, and faster onboarding. The trade-off is less regulatory oversight and occasionally less stability.

| Factor | EU account | Offshore account |

|---|---|---|

| Approval rate | Moderate | Higher |

| Processing fees | 4% to 6% | 5% to 9% |

| Consumer protection | Strong (EEA rules) | Limited |

| Card scheme access | Visa/Mastercard direct | Often via third-party |

| Onboarding time | 1 to 3 weeks | 3 to 10 days |

| Regulatory stability | High | Variable |

Most mature high-risk operators use both. An EU account handles regulated markets and card scheme volume, while an offshore account processes jurisdictions or business lines that EU acquirers will not touch. Understanding the full range of banking solution types available to your sector is the starting point for building a resilient payment infrastructure.

Key considerations when choosing:

- Your customer base geography (EU customers expect EU-regulated billing)

- Your licence status (a Malta Gaming Authority licence opens EU acquirer doors)

- Your chargeback history (offshore is more forgiving for new operators)

- Your long-term growth plans (EU accounts scale better with card scheme programmes)

For a detailed breakdown of the trade-offs, the offshore vs onshore account comparison and the case for why go offshore are both worth reviewing before you commit to a structure.

Comparing payment processing solutions: a side-by-side analysis

Systematic comparison reveals which solutions align with your operational priorities. Comparative analysis helps identify the best fit for specific high-risk business needs, balancing cost, compliance, and customer experience. The following table examines three primary solution categories across critical evaluation dimensions:

| Solution Type | Processing Fees | Compliance Complexity | Integration Ease | Best Suited For |

|---|---|---|---|---|

| Card Processors | 3-8% plus reserves | High (PCI DSS, fraud monitoring) | Moderate (established APIs) | iGaming platforms with diverse customers |

| Crypto Gateways | 0.5-2% | Moderate (blockchain verification) | Easy (simple API integration) | Crypto exchanges and tech-savvy audiences |

| E-Wallets | 2-5% | Moderate (KYC/AML protocols) | Easy (plug-and-play options) | Forex brokers with international clients |

| Bank Transfers | 0.1-1% | Low (direct banking relationship) | Complex (requires banking integration) | High-value B2B transactions |

Card processors excel when customer convenience outweighs cost concerns. They offer the broadest market reach but demand rigorous chargeback management systems. Crypto gateways shine for businesses targeting digital-native audiences, offering superior economics and eliminating chargeback fraud entirely. However, they require customer education and expose you to cryptocurrency price fluctuations unless you immediately convert to fiat.

E-wallets strike a middle ground, particularly for banking solutions for high-risk businesses operating across multiple jurisdictions. They simplify cross-border payments and reduce compliance overhead compared to card networks. Bank transfers remain optimal for Forex brokers handling substantial deposits where customers accept longer settlement times in exchange for minimal fees.

Risk mitigation capabilities vary dramatically. Card processors provide sophisticated fraud scoring but expose you to chargeback disputes that can threaten merchant accounts. Crypto transactions offer finality but require robust wallet security. E-wallets balance these concerns with reversible transactions under dispute protocols, though this reintroduces chargeback exposure.

Pro Tip: Consider the balance of cost versus compliance demands by calculating total cost of ownership, including processing fees, compliance software, staff training, and potential chargeback losses, rather than focusing solely on headline processing rates.

Core types of payment processing risk

Most businesses treat payment risk as synonymous with fraud. That framing is dangerously incomplete. The risks in payment processing span four distinct categories, each with its own mechanics, consequences, and mitigation requirements.

Fraud risk

Fraud is the most visible category, but its detection has become genuinely sophisticated. Modern processors use real-time fraud scoring that analyses behavioural and payment signals within milliseconds, flagging elevated-risk transactions before they complete. These signals include device fingerprinting, IP geolocation, transaction velocity, and card verification results.

The financial stakes are significant. Businesses lost 7.7% of annual revenue to fraud in the 2024 to 2025 period. That figure includes direct losses, dispute fees, and the operational cost of managing fraudulent orders. For high-risk businesses, fraud exposure is compounded by the fact that many operate in digital environments where physical verification is impossible.

Chargeback risk

A chargeback occurs when a cardholder disputes a transaction directly with their bank rather than seeking a refund from the merchant. This is distinct from a refund. The merchant bears the cost of the original transaction, a dispute fee, and the administrative burden of responding.

Card networks set hard thresholds. Mastercard fines merchants who exceed a 1.5% chargeback rate, and approaching 1% is already considered problematic by most processors. Sustained high chargeback rates can result in account suspension, placement on industry blacklists such as MATCH, and difficulty securing future processing relationships.

Compliance risk

Payment compliance obligations include PCI DSS (the Payment Card Industry Data Security Standard), Know Your Customer (KYC) protocols, and Anti-Money Laundering (AML) regulations. Failing to meet these requirements does not just expose your own business to penalties. It creates liability for your processor, which is precisely why non-compliant merchants are terminated quickly.

The regulatory environment is tightening. Regulators are increasingly holding processors accountable for inadequate merchant monitoring, which means processors are in turn placing greater compliance demands on the businesses they onboard.

Reputational risk

Reputational risk is the most underestimated category. A business operating in a legal but socially contentious industry, such as online gambling or adult content, can lose processing access not because it did anything wrong, but because the processor decides the association no longer aligns with its risk appetite. Conduct matters. Public regulatory actions, media coverage, or customer complaints can shift a processor’s willingness to maintain the relationship.

Pro Tip: Keep a documented compliance record, including KYC verification logs, PCI DSS attestations, and chargeback response histories. This documentation actively reduces perceived risk during processor reviews and underwriting.

Recommended

- Payment processing best practices for high-risk businesses 2026

- Payment processing solutions for high-risk industries 2026

- High-risk banking in the EU: 87% approval guide for 2026

- What is high approval banking? A guide for high-risk sectors

Frequently asked questions

What is meant by high-risk payment processing?

High-risk payment processing refers to specialised banking setups with stricter scrutiny, higher fees, and added compliance for businesses prone to chargebacks and regulatory risk. These accounts require rolling reserves and intensive monitoring.

Why are chargebacks such a major issue for high-risk industries?

Chargebacks damage reputations, trigger fines, and quickly lead to account shutdowns when thresholds are exceeded. Visa’s threshold sits at 0.9-1%, whilst many high-risk sectors average 2-5%, creating constant pressure to maintain low dispute rates.

How do rolling reserves work in high-risk merchant accounts?

A rolling reserve holds back 5-15% of transactions for 90-180 days to cover possible losses from chargebacks or fraud. Processors release funds gradually as your account demonstrates stability.

Can cryptocurrency solve my payment processing problems?

Cryptocurrency reduces chargebacks to zero and cuts fees to 0.5-1%, but brings volatility risk and requires customer adoption. It works best as part of a hybrid approach rather than a complete replacement.

What happens if I get placed on a blacklist like MATCH?

MATCH list placement makes opening new accounts nearly impossible and severely limits payment options for five years. Prevention through compliance and chargeback management is essential.