TL;DR:

- Kahnawake casino banking requires strict AML, KYC, and technical infrastructure compliance, making standard accounts unsuitable.

- Payment data must be hosted locally at MIT with segregated accounts and real-time monitoring to ensure regulatory adherence.

- Ongoing audit practices and dynamic internal processes are critical for long-term operational resilience and licensing stability.

Opening a bank account for a Kahnawake casino is nothing like opening a business current account at your local branch. The Kahnawake Gaming Commission (KGC) imposes a layered web of anti-money laundering, know-your-customer, and technical infrastructure mandates that instantly disqualify most conventional banking routes. Operators who underestimate this complexity risk licence suspension, frozen funds, and regulatory penalties before they process a single player deposit. This guide walks you through the regulatory foundations, payment processing frameworks, resilient account structures, and ongoing compliance practices that separate operators who thrive in Kahnawake from those who stall at the first banking rejection.

Key Takeaways

| Point | Details |

|---|---|

| Kahnawake banks face strict rules | Operators must meet KGC’s advanced AML, KYC, and audit requirements to retain licences. |

| Local hosting ensures compliance | Mohawk Internet Technologies server hosting is mandatory for all payments and transaction data. |

| Segregated and resilient accounts | Use specialised account structures with layered compliance for security and operational continuity. |

| Proactive compliance protects business | Build KYC and AML flows into everyday operations to prevent costly regulatory issues. |

Understanding Kahnawake licensing and banking regulations

The KGC is one of the longest-standing online gaming regulators in the world, but longevity does not mean simplicity. Its framework is deliberately demanding, and for good reason. Every licensed operator must satisfy strict financial oversight requirements before a single transaction is processed.

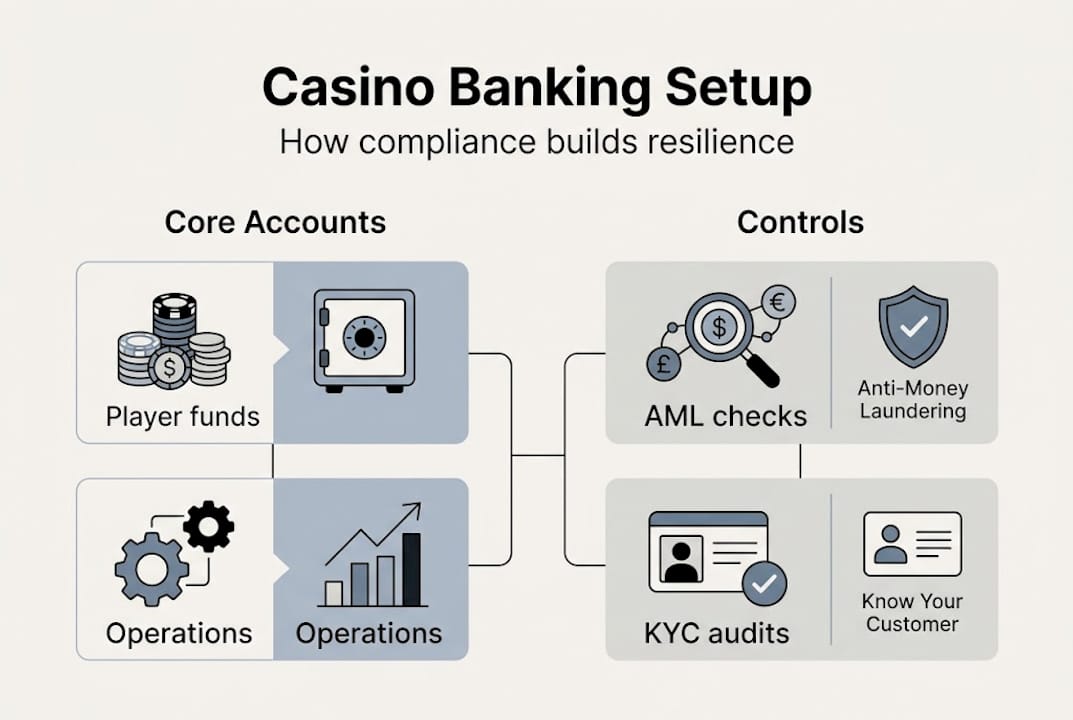

KGC mandates strict AML/CFT compliance, including complete records of financial transactions, internal audits, KYC procedures, and continuous monitoring for suspicious activities in payment processing. AML stands for anti-money laundering. CFT stands for countering the financing of terrorism. KYC means know your customer, the process of verifying player identities before they deposit or withdraw. These are not optional add-ons. They are baseline requirements baked into every licence condition.

The high-risk classification of iGaming reshapes what banks are willing to offer. Most mainstream banks in Canada and internationally categorise casino operators as high-risk clients. This means standard business accounts are routinely declined, and even where they are approved, the terms are often restrictive, with low transaction limits and sudden account closures. The idea that you can simply open an iGaming bank account through a standard commercial bank is one of the most damaging misconceptions in this space.

Here is what the KGC specifically requires of licensees on the financial compliance side:

- Documented KYC procedures for every player account

- Ongoing AML monitoring with flagging protocols for suspicious transactions

- Complete financial transaction records retained for audit purposes

- Internal audit schedules with written findings

- Segregated player funds, kept separate from operational capital

- Reporting obligations to the KGC on request

Failing to meet these requirements is not a minor administrative issue. The KGC can suspend or revoke a licence, freeze operations, and issue financial penalties. Operators have lost their licences over documentation gaps alone, not fraud, just missing paperwork.

“Tick-box compliance is not the same as functional compliance. The KGC looks at whether your processes actually work, not just whether you have a policy document on file.”

Pro Tip: Before approaching any bank or payment provider, prepare a compliance dossier that includes your KYC policy, AML procedures, transaction monitoring methodology, and audit schedule. Banks assess your risk profile before they assess your revenue. A well-prepared dossier can dramatically improve your approval odds, which is why integrating casino KYC processes into your banking application from the outset is a strategic advantage.

Payment processing frameworks: Local hosting, data flow, and compliance

Regulations dictate not just policy, but also influence technical and operational models. For Kahnawake operators, this is where many are caught off guard. The KGC’s technical requirements are unusually specific and directly affect how payment data is handled.

All servers must be hosted locally at Mohawk Internet Technologies (MIT) in Kahnawake, which directly impacts payment data security and compliance architecture. This is not a suggestion. MIT is the designated hosting provider, and your payment processing infrastructure must sit within that environment. This affects latency, integration options, and the vendors you can work with.

Segregated accounts and local server hosting ensure player fund protection and transaction auditability, with AML and KYC integrated directly into payment flows to prevent laundering. This means your payment gateway must be configured to trigger identity checks and flag anomalies in real time, not as a post-processing step.

Here is a clear breakdown of the core compliance requirements for payment processing:

| Requirement | Detail | Compliance impact |

|---|---|---|

| Server hosting | Must be at MIT in Kahnawake | Non-negotiable; affects all payment vendors |

| Account segregation | Player funds separate from operations | Protects players; required for audit |

| Audit trails | Full transaction logs retained | Must be accessible to KGC on request |

| KYC integration | Identity checks at deposit and withdrawal | Prevents fraud and laundering |

| AML monitoring | Real-time suspicious activity flagging | Mandatory; linked to licence conditions |

The step-by-step flow from player deposit to funds reconciliation typically works as follows:

- Player initiates deposit via the payment gateway hosted at MIT

- KYC check is triggered automatically against verified identity records

- Funds are routed to the segregated player account, not the operator’s operational account

- Transaction is logged with full metadata for audit trail purposes

- AML monitoring scans the transaction against risk parameters

- Reconciliation is performed at agreed intervals, with records stored for regulatory review

Pro Tip: Before going live, run a sandboxed test environment that mirrors your full payment flow, including KYC triggers and AML flags. Many operators discover integration gaps during testing that would have caused compliance failures in production. Pairing this with high-risk payment solutions designed for iGaming environments reduces the risk of technical non-compliance significantly. You can also review guidance on streamlining payment processes to optimise your setup before launch.

Establishing resilient banking structures for Kahnawake operators

With technical and process requirements clear, the next challenge is structuring banking relationships effectively. This is where most Kahnawake operators either build a solid foundation or create fragility that surfaces at the worst possible moment.

Traditional banks fail Kahnawake licensees for predictable reasons. Casino operations generate high transaction volumes, involve international player bases, and carry reputational risk that compliance teams at mainstream banks are not equipped to manage. The result is rejection, or worse, an account that is opened and then abruptly closed mid-operation.

Segregated accounts with integrated AML and KYC controls are the operational standard for iGaming operators, protecting player funds and ensuring full auditability. A segregated account means player deposits are held separately from your working capital. If your business faces a financial dispute, player funds are protected. This is both a regulatory requirement and a commercial safeguard.

Here is a comparison of the main account structures available to Kahnawake operators:

| Account type | Compliance burden | Cost level | Suitability for KGC |

|---|---|---|---|

| Offshore bank account | Moderate to high | Low to medium | Conditional on structure |

| Local Canadian bank | Very high | Medium | Rarely approved |

| E-money institution (EMI) | Moderate | Medium | Strong if iGaming-friendly |

| Dedicated iGaming account | High but supported | Higher | Best fit for KGC mandates |

For offshore bank account options to work for a Kahnawake casino, they must be structured with proper segregation and AML controls built in, not bolted on afterwards. EMIs are increasingly popular because they offer faster onboarding and more flexible transaction handling, though not all EMIs accept iGaming clients.

Common banking errors made by Kahnawake casino operators include:

- Using a single account for both player funds and operational expenses

- Selecting a bank without prior iGaming experience or risk appetite

- Failing to disclose the gaming licence during the account application

- Ignoring currency diversification, leaving the business exposed to FX risk

- Not establishing backup banking relationships before the primary account is stressed

A resilient, multi-layered setup typically includes a primary segregated player account, a secondary operational account, and at least one EMI relationship for payment redundancy. Exploring banking solutions for high-risk businesses gives you a clearer picture of which combinations work best for iGaming operators in your jurisdiction.

Integrating compliance: Practical steps for ongoing audit and reporting

Operational resilience only works if reinforced by ongoing compliance and comprehensive audit trails. Many operators treat compliance as a launch-phase activity. That is a costly mistake.

Operators must maintain complete records of financial transactions, internal audits, KYC procedures, and AML controls to avoid penalties. The KGC does not accept retrospective compliance. If your records are incomplete at the point of audit, the consequences are immediate.

Here is a five-point action plan for embedding compliance into daily operations:

- Automate transaction monitoring using software that flags anomalies in real time against pre-set AML thresholds

- Schedule monthly internal audits with written findings stored in a compliance management system

- Maintain a live KYC register that updates automatically when player verification status changes

- Conduct quarterly reviews of your AML policy against any KGC regulatory updates

- Assign a dedicated compliance officer who liaises directly with your banking partners and the KGC

The must-have data points to track in every audit cycle include:

- Full transaction logs with timestamps, player IDs, and amounts

- KYC verification status and date of last update for each player

- AML flag history and resolution records

- Segregated account balances reconciled against player liability

- Internal audit reports with sign-off from a senior officer

- Correspondence with the KGC, including any requests or notices

Regulatory non-compliance is not a theoretical risk. Licence suspension can follow a single failed audit cycle, cutting off your payment processing and banking access simultaneously. Reviewing EU casino banking strategies provides useful cross-jurisdictional context, and keeping up with high-risk financial compliance developments ensures your processes stay ahead of regulatory shifts rather than reacting to them.

Editorial perspective: What most guides get wrong about Kahnawake casino banking

Most articles on Kahnawake banking treat compliance as a checklist. Get the KYC policy written, set up an AML procedure, open a segregated account, done. That framing is dangerously incomplete.

What separates operators who build durable businesses from those who face repeated banking disruptions is the quality of their internal processes, not just their documentation. A policy document that no one follows is worse than having no policy at all, because it creates false confidence.

The MIT server requirement is a good example of where technical and commercial decisions collide. Hosting at MIT is non-negotiable, but how you architect your payment flows within that constraint determines whether you can integrate modern payment innovations or remain locked into legacy processing options.

Agility matters. The operators who succeed long-term treat their iGaming banking setup as a living system, reviewing financial controls proactively rather than waiting for an audit to expose gaps. Compliance is not a destination. It is an ongoing operational discipline that directly enables commercial growth.

Get support for Kahnawake casino banking challenges

If these challenges seem daunting, specialist guidance can streamline the path to compliance and sustainable profit. At BankMyCapital, we work directly with iGaming operators navigating the specific demands of Kahnawake licensing, from structuring segregated accounts to engineering payment workflows that satisfy KGC technical requirements from day one.

Our network of over 50 pre-vetted banking partners and EMIs means we can match your operation with institutions that actively welcome iGaming clients, with an 87% approval rate and onboarding typically completed within two to three weeks. Explore our payment processing solutions for iGaming, set up business banking without a local setup, or review our high-risk payment processing best practices to understand exactly what a compliant, resilient banking structure looks like in practice.

Frequently asked questions

Does my Kahnawake casino need to host all payment servers locally?

Yes, the KGC requires all core casino servers, including those handling payments, to be hosted at MIT in Kahnawake. There are no approved exceptions to this infrastructure requirement.

What is the biggest compliance risk for Kahnawake casino banking?

The primary risk is failing to maintain proper AML, KYC, and transaction audit records, which can trigger immediate licence suspension and loss of banking access.

Can I use a standard offshore bank account for my Kahnawake casino?

Standard offshore accounts rarely satisfy KGC demands. You need segregated, AML-integrated accounts specifically structured for iGaming compliance, not generic offshore banking products.

Does every payment flow require KYC integration?

Yes. KGC regulation demands that KYC and AML checks are embedded into every initiated payment to prevent laundering and maintain ongoing licence compliance.

What happens if I fail an AML audit in Kahnawake?

Failing an AML audit puts your licence at immediate risk. Incomplete financial records or absent AML controls can result in licence revocation and the loss of all associated banking and payment processing privileges.