TL;DR:

- EMI is a fixed monthly payment that repays a loan’s principal and interest over a set period, simplifying budgeting. The reducing-balance method generally results in lower total interest costs than the flat-rate approach, especially for long-term loans. Choosing an appropriate tenure involves balancing monthly affordability against total interest paid, with prepayments helping reduce overall costs.

An Equated Monthly Instalment (EMI) is a fixed monthly payment that repays both the principal and interest of a loan over a defined period. Understanding what is EMI in payments matters whether you are taking out a mortgage, financing business equipment, or structuring a personal loan. Every EMI payment is identical in amount, which makes budgeting straightforward and repayment predictable. Two primary calculation methods exist: the flat-rate method and the reducing-balance method, each producing a different total interest cost over the loan’s life.

What is EMI in payments and how does it work?

EMI stands for Equated Monthly Instalment, the standard industry term used across banking, lending, and finance globally. Each payment you make covers a portion of the original loan amount (the principal) and the interest charged on the outstanding balance. The ratio between principal and interest within each payment shifts over time, but the total amount you pay each month stays constant throughout the loan tenure.

The amortisation dynamic is the key mechanism behind EMI. In the early months of a loan, the majority of each payment goes towards interest because the outstanding balance is at its highest. As you reduce the principal, the interest portion shrinks and more of each payment clears the actual debt. By the final months, almost the entire EMI goes towards principal repayment.

Common loan types that use EMI structures include home mortgages, auto loans, personal loans, and business equipment financing. Loan tenures vary from months to many years depending on the product, which gives borrowers flexibility to match repayment schedules to their income or cash flow cycles.

How is EMI calculated? the formula explained

The standard EMI formula is: EMI = [P × r × (1 + r)^n] ÷ [(1 + r)^n – 1]

Each variable carries a specific meaning:

| Variable | Meaning | Example Value |

|---|---|---|

| P | Principal loan amount | £50,000 |

| r | Monthly interest rate (annual rate ÷ 12) | 0.5% (6% annual ÷ 12) |

| n | Total number of monthly payments | 60 (5 years) |

Using the example above, a £50,000 loan at 6% annual interest over 60 months produces a monthly EMI of approximately £966. That figure stays fixed for every one of the 60 payments, regardless of how the internal split between principal and interest changes.

The EMI calculation formula accounts for compound interest, which is why the maths is more involved than simply dividing the loan by the number of months. Dividing £50,000 by 60 gives you £833 per month, but that ignores the cost of borrowing entirely. The formula corrects for this by factoring in the time value of money.

Understanding the formula also reveals why small changes in the interest rate have an outsized effect on total repayment cost. A 1% increase in annual rate on a £200,000 mortgage over 25 years adds tens of thousands of pounds to the total amount repaid.

Pro Tip: Use a dedicated loan comparison calculator to model different principal amounts, rates, and tenures side by side before committing to any loan structure. The numbers often reveal surprises that a rough mental estimate misses entirely.

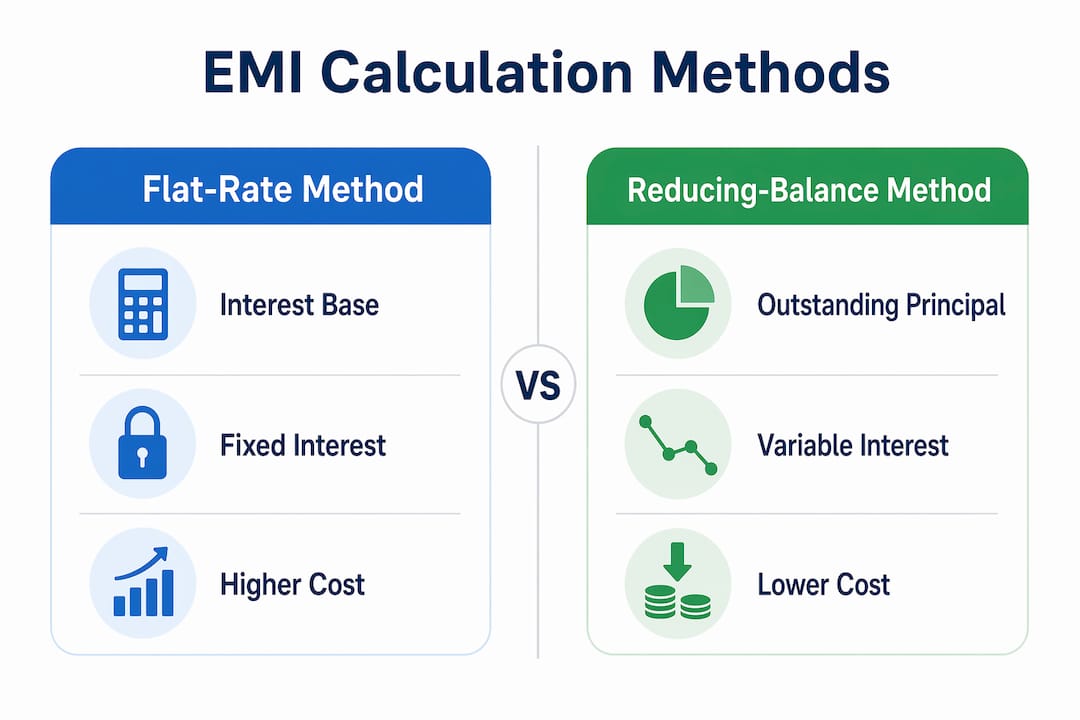

Flat-rate vs reducing-balance: which method costs more?

The two primary methods of EMI interest calculation produce very different outcomes, even when the headline interest rate looks identical.

Flat-rate method: Interest is calculated on the original principal for the entire loan tenure. If you borrow £10,000 at 10% flat for 3 years, you pay £1,000 in interest every year regardless of how much principal you have already repaid. Total interest = £3,000.

Reducing-balance method: Interest applies only to the outstanding principal at the start of each period. As you repay principal, the interest charge falls. On the same £10,000 at 10% over 3 years, total interest is considerably lower because the base shrinks with every payment.

| Feature | Flat-Rate Method | Reducing-Balance Method |

|---|---|---|

| Interest base | Original principal | Outstanding balance |

| Total interest paid | Higher | Lower |

| Typical loan types | Personal loans, consumer credit | Mortgages, business loans |

| Monthly EMI amount | Fixed, simpler to calculate | Fixed, but interest portion decreases |

| Effective annual rate | Higher than stated rate | Closer to stated rate |

The reducing-balance method is generally more economical for long-term loans such as mortgages. Lenders who advertise flat-rate products often quote a lower headline rate, but the effective annual rate is significantly higher once you account for the unchanged interest base.

Key points to watch for when comparing loan offers:

- Always ask whether the quoted rate is flat or reducing-balance.

- Convert flat rates to their effective equivalent before comparing products.

- For loans over 3 years, the difference in total interest between the two methods can exceed 30% of the original principal.

- Reducing-balance products are standard across EU banking and most regulated lending markets.

How do emis benefit individuals and businesses?

Fixed monthly payments reduce financial uncertainty by making cash flow forecasting reliable. You know exactly what leaves your account on the same date every month, which simplifies both personal budgeting and business treasury management.

For individuals, EMIs make large purchases accessible without requiring a lump sum. A £30,000 car purchase spread over 48 months at a competitive rate becomes a manageable monthly commitment rather than a capital event that drains savings. The same logic applies to home improvements, medical costs, and education financing.

For businesses, the advantages of EMI accounts extend beyond simple affordability. Equipment financing through EMI preserves working capital, which can then be deployed into revenue-generating activities. A manufacturing firm that finances a £500,000 CNC machine over 5 years keeps its cash reserves intact for stock, staffing, and growth.

Additional benefits worth noting:

- Borrower discipline: Fixed payment schedules create a structured repayment habit, reducing the risk of default compared to open-ended credit facilities.

- Lender predictability: Lenders price EMI products more competitively because the repayment structure is well-defined and default risk is easier to model.

- Credit profile improvement: Consistent on-time EMI payments build a positive credit history, improving access to future financing at better rates.

Pro Tip: If your business operates in a high-risk sector such as iGaming, forex, or crypto, EMI banking for high-risk businesses offers an alternative route to structured payment facilities when traditional banks decline applications.

What should you consider when choosing EMI tenure?

Tenure selection is the single most consequential decision in structuring an EMI loan. The trade-off is direct: a longer tenure lowers your monthly payment but increases the total interest you pay over the life of the loan.

Consider a £100,000 loan at 8% annual interest:

- 10-year tenure: Monthly EMI approximately £1,213. Total repayment approximately £145,593. Total interest approximately £45,593.

- 20-year tenure: Monthly EMI approximately £836. Total repayment approximately £200,760. Total interest approximately £100,760.

- 30-year tenure: Monthly EMI approximately £734. Total repayment approximately £264,155. Total interest approximately £164,155.

The monthly saving between a 10-year and 30-year tenure is £479. The additional interest cost is over £118,000. Longer repayment tenures reduce immediate financial burden but result in significantly higher total interest paid. Financial advisors consistently stress managing loan tenure carefully to avoid excessive total interest costs despite the appeal of lower monthly payments.

Prepayments are a practical way to reduce this cost. Making prepayments or paying additional amounts against the principal reduces the outstanding balance faster, which cuts the total interest charged. Some loan agreements include early repayment penalties, so always check the terms before making lump-sum payments against the principal.

One persistent misconception is that APR and EMI are the same figure. They are not. APR represents annual borrowing cost as a percentage, while EMI is the actual cash amount you pay each month. EMI is derived mathematically from the APR, the principal, and the tenure. Confusing the two leads borrowers to underestimate their actual monthly commitment. Use a calculator that takes all three inputs to get the true monthly figure before signing any agreement.

Key takeaways

EMI works because it converts a large debt into fixed, predictable monthly payments that cover both principal and interest, with the reducing-balance method delivering the lowest total interest cost for long-term loans.

| Point | Details |

|---|---|

| EMI definition | A fixed monthly payment covering principal and interest over a set loan tenure. |

| Calculation formula | EMI = [P × r × (1 + r)^n] ÷ [(1 + r)^n – 1], where P is principal, r is monthly rate, n is months. |

| Flat vs reducing-balance | Reducing-balance method costs less in total interest and is standard for mortgages and business loans. |

| Tenure trade-off | Longer tenures lower monthly payments but significantly increase total interest paid over the loan’s life. |

| APR vs EMI | APR is an annual percentage rate; EMI is the actual monthly cash payment derived from APR, principal, and tenure. |

How Bankmycapital supports your EMI and payment structuring

Bankmycapital works with businesses in high-risk sectors including crypto, iGaming, adult entertainment, and forex to establish banking relationships and structure payment facilities that conventional banks routinely decline. If your business needs EMI-based loan structuring, payment account setup, or access to pre-vetted financial partners across EU and offshore jurisdictions, Bankmycapital’s consultancy network covers it. The firm reports an 87% approval rate across its client base, with onboarding typically completed within 2–3 weeks. Explore the full range of banking and payment solutions or visit Bankmycapital directly to discuss your specific requirements with a specialist.

FAQ

What does EMI stand for in finance?

EMI stands for Equated Monthly Instalment. It is a fixed monthly payment that repays both the principal and interest of a loan over a chosen tenure.

How is EMI different from a regular loan repayment?

EMI payments are fixed in amount for the entire loan term, unlike variable repayments that change with the outstanding balance. The internal split between principal and interest shifts each month, but the total payment stays constant.

Which EMI calculation method is cheaper: flat-rate or reducing-balance?

The reducing-balance method is cheaper in total interest cost. It applies interest only to the outstanding principal, so the interest charge falls as you repay the loan.

Does a longer loan tenure mean lower EMI payments?

Yes, but the total interest paid increases significantly with tenure length. A 30-year mortgage on £100,000 at 8% costs over £118,000 more in interest than the same loan repaid over 10 years.

Can you reduce your EMI interest cost through prepayments?

Making prepayments against the principal reduces the outstanding balance faster and lowers total interest charged. Check your loan agreement for any early repayment penalties before making additional payments.