Global banks paid over $5 billion in AML fines in 2023, driving unprecedented caution against high-risk sectors. Many compliant crypto, iGaming, and forex businesses across the EU now face banking refusals despite operating legally. This guide reveals why banks reject these sectors and how to improve your acceptance chances through strategic compliance and jurisdiction selection.

Key Takeaways

| Point | Details |

|---|---|

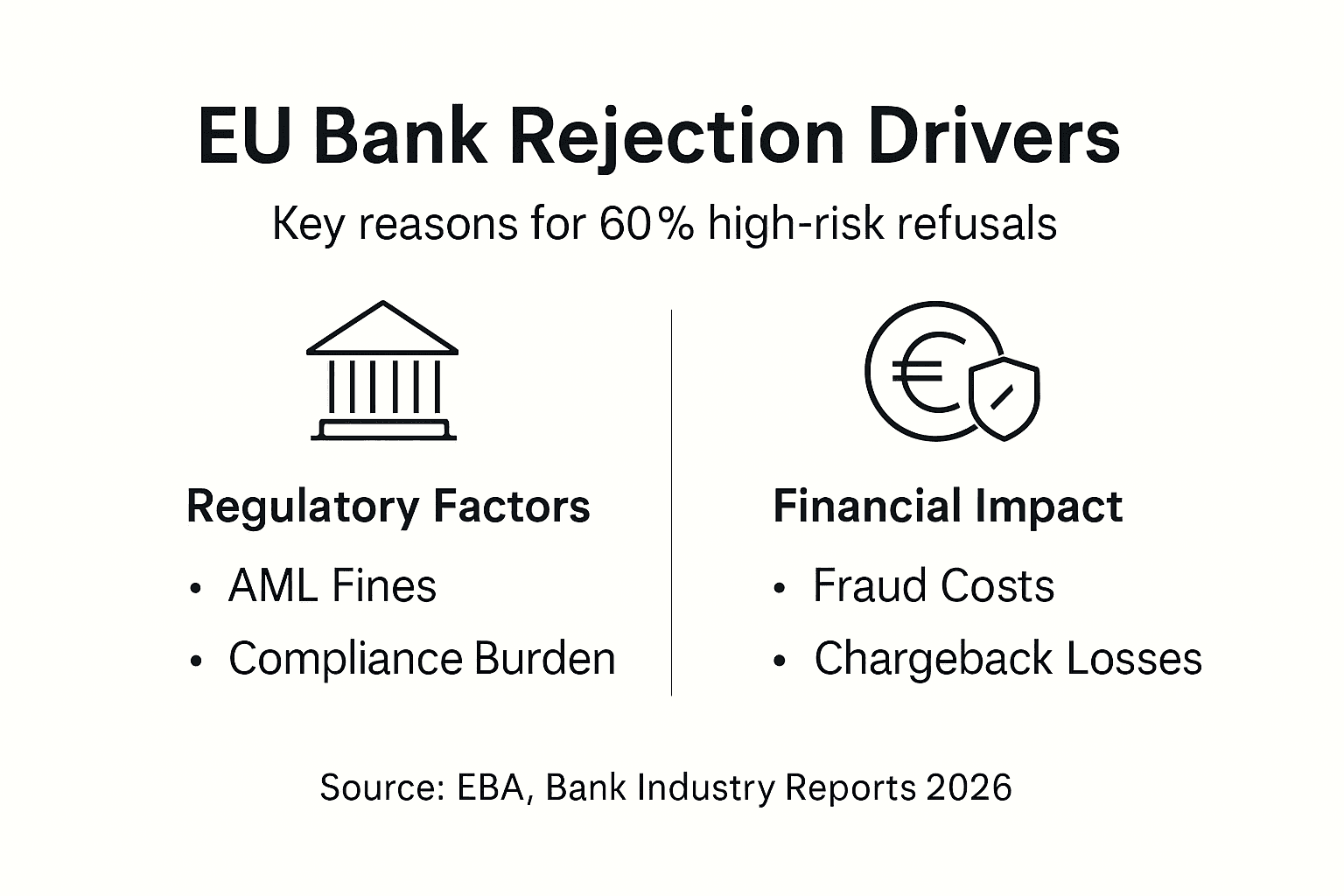

| Banks reject high-risk sectors | Elevated financial crime and reputational risks drive conservative onboarding policies. |

| EU regulations increase scrutiny | MiCA and PSD3 mandates raise compliance burdens significantly. |

| Operational costs deter banks | High fraud and chargeback rates create financial strain. |

| Strategic compliance boosts approval | Strong KYC/AML processes and jurisdiction choice improve banking access. |

| Crypto gateways complement banking | They offer alternatives but cannot fully replace compliant accounts. |

Understanding Bank Risk Assessment Criteria

Banks evaluate potential clients through sophisticated risk frameworks that assess sector classification, geographic exposure, ownership structures, and transaction patterns. Your business operates in crypto, iGaming, or forex? That immediately triggers enhanced scrutiny protocols.

Regulatory fines exceeding $5 billion in recent years have made financial institutions extraordinarily cautious. They fear both monetary penalties and the reputational damage that follows money laundering or terrorist financing scandals. This fear shapes every onboarding decision.

FATF and EBA guidelines mandate enhanced due diligence for high-risk sectors, creating a 40-60% higher rejection likelihood compared to traditional businesses. Banks must verify beneficial ownership, source of funds, transaction purposes, and ongoing activity patterns with exhaustive documentation.

Specific sectors face particular challenges:

- Crypto businesses encounter scrutiny over wallet verification and blockchain traceability

- iGaming platforms deal with concerns about player fund segregation and licensing validity

- Forex brokers must demonstrate sophisticated transaction monitoring and client classification systems

Reputational risk weighs heavily in bank decision making. One compliance failure can trigger regulatory investigations, customer exodus, and share price drops. Banks calculate whether your business relationship justifies these potential consequences.

“The cost of getting it wrong far exceeds the revenue from most high-risk accounts. Banks choose safety over profit when reputational stakes are this high.”

Your high-risk business banking checklist should address every criterion banks use to reject high-risk sectors before you submit applications.

Regulatory and Compliance Challenges in the EU

The EU regulatory landscape has intensified dramatically in 2026. MiCA regulation deadlines now force crypto businesses to implement comprehensive compliance frameworks or face operating restrictions. You cannot ignore these requirements and expect banking access.

PSD3 mandates enhanced due diligence across payment services and fintech operations, directly impacting how banks evaluate your application. Every transaction pattern, customer relationship, and operational process faces deeper scrutiny than ever before.

70% of EU authorities report rising money laundering and terrorist financing risks in fintech and crypto sectors due to weak AML governance. This statistic shapes bank attitudes toward your entire industry, not just individual businesses.

Key regulatory pressures driving rejection rates:

- MiCA compliance deadlines requiring extensive operational restructuring

- Travel Rule implementation for crypto transactions above thresholds

- PSD3 strong customer authentication requirements

- Beneficial ownership transparency mandates across all jurisdictions

- Real-time transaction monitoring obligations

Banks face mounting compliance costs themselves. Every high-risk client requires dedicated resources for ongoing monitoring, regulatory reporting, and periodic reviews. Many institutions calculate that these costs exceed potential revenue, particularly for smaller accounts.

EU banking regulations for high-risk businesses create a complex web of obligations that vary by member state. The EBA money laundering risks report highlights how regulatory fragmentation compounds challenges for both banks and businesses.

Compliance complexity translates directly into higher rejection rates. Banks prefer straightforward clients over those requiring specialized regulatory expertise and enhanced monitoring systems.

Financial and Operational Challenges for Banks Serving High-Risk Sectors

Financial realities drive banking decisions as much as regulations. Chargebacks and fraud costs total 8-10% of gross revenue for high-risk merchants, creating immediate operational losses for partner banks.

Every chargeback costs $4.61 per $1 lost to fraud, plus processing fees ranging from 3% to 6%. These costs stack rapidly when serving sectors with elevated dispute rates. Banks absorb much of this financial burden through their risk management processes.

Rolling reserves impose another layer of financial strain:

| Reserve Type | Percentage | Duration | Impact |

|---|---|---|---|

| Standard rolling reserve | 5-10% | 90-180 days | Reduces available liquidity |

| High-risk reserve | 10-20% | 180-365 days | Significantly limits cash flow |

| Security deposit | 15-30% | Until account closure | Ties up substantial capital |

Banks hold these reserves to cover potential losses, but you experience reduced working capital. This arrangement makes high-risk accounts less attractive compared to traditional businesses requiring no reserves.

Operational burdens extend beyond direct costs:

- Specialized compliance staff dedicated to high-risk portfolio monitoring

- Advanced transaction screening systems requiring constant updates

- Enhanced due diligence refreshes every 6-12 months

- Regulatory reporting obligations consuming significant resources

- Legal counsel costs for regulatory liaising and policy interpretation

These expenses reduce banks’ willingness to serve high-risk clients, particularly when profit margins are compressed by competitive pressures and low interest environments.

Pro Tip: Implement chargeback reduction strategies like robust fraud detection, clear terms disclosure, and proactive customer service to improve bank acceptance chances and reduce operational costs.

Exploring banking solutions for high-risk businesses helps you understand how specialized institutions structure services to manage these chargeback and fraud costs more effectively.

Common Misconceptions about Bank Rejections

Many business owners believe their sector is inherently illegal, but crypto, iGaming, and forex operate perfectly legally across numerous EU jurisdictions with proper licensing. Banks reject you not because your business is illegal, but because they fear reputational consequences.

Up to 60% of fully compliant high-risk businesses face bank refusal due to reputation risk, not compliance failures. Your documentation might be perfect, your operations transparent, yet banks still decline. This reflects institutional risk appetite, not your business quality.

Common false beliefs:

- Rejection always indicates compliance deficiencies in your operations

- Only businesses with suspicious activity face banking barriers

- All banks evaluate high-risk sectors using identical criteria

- Offshore incorporation automatically triggers rejection

- Larger businesses always receive preferential treatment

Banks make risk-averse decisions based on sector classification alone. They fear regulatory scrutiny, potential fines, and negative media coverage that might follow any compliance incident. Even your exemplary track record cannot always overcome these institutional fears.

“Banks reject based on what might happen, not what has happened. Fear of restrictive account measures drives conservative policies that exclude compliant businesses.”

You need to understand this psychology. Banks balance potential revenue against worst-case scenarios. When regulators signal heightened scrutiny of your sector, banks withdraw rather than invest in enhanced monitoring capabilities.

Pro Tip: Maintain transparent, ongoing compliance documentation including audit trails, KYC refreshes, and transaction monitoring reports to counter misperceptions about your sector and demonstrate commitment to best practices.

Review bank compliance for high-risk accounts to understand how addressing misconceptions about bank rejections through superior documentation improves outcomes.

Navigating Jurisdictional Options for High-Risk Banking

Jurisdiction selection dramatically impacts your banking success. Malta, Switzerland, and the UK consistently rank highest for regulatory friendliness toward crypto and iGaming businesses in 2026. These jurisdictions offer clear compliance frameworks that reduce bank uncertainty.

Banks specialize in certain jurisdictional risks. A Lithuanian EMI might welcome crypto businesses while a German institution rejects them entirely. Understanding these specializations helps you target receptive partners.

| Jurisdiction | High-Risk Friendliness | Key Advantages | Considerations |

|---|---|---|---|

| Malta | Very High | Established crypto/iGaming frameworks | Requires local licensing |

| Switzerland | High | Strong privacy, stable regulations | Higher operational costs |

| UK | High | Mature fintech ecosystem | Post-Brexit regulatory evolution |

| Estonia | Medium-High | Digital-first approach | Enhanced scrutiny post-scandals |

| Cyprus | Medium | iGaming specialization | Recent regulatory tightening |

Selecting jurisdictions with clear compliance frameworks aids banking acceptance by reducing ambiguity. Banks prefer jurisdictions where regulatory expectations are explicit and enforcement is consistent.

Offshore jurisdictions can offer improved onboarding chances when properly structured. Seychelles, BVI, and Cayman Islands maintain specialized banking sectors serving high-risk industries with appropriate compliance protocols.

Proper jurisdiction choice reduces regulatory ambiguity for banks evaluating your application. When they understand the licensing regime, supervision framework, and enforcement history, they can assess risk more accurately. This clarity improves approval rates.

Explore EU high-risk banking jurisdictions and offshore banking for high-risk sectors to identify optimal locations for your operations and banking relationships.

Mitigating Bank Rejection Risk with Compliance Best Practices

Preparing complete KYC/AML documentation before application submission dramatically improves outcomes. Banks appreciate organized, comprehensive packages that demonstrate your understanding of compliance obligations.

Structured KYC approaches can increase approval rates up to 87% in specialized banking contexts. This statistic reflects how proper preparation signals professionalism and reduces bank workload during due diligence.

Maintain transparent governance and transaction monitoring records that demonstrate ongoing compliance commitment. Banks want evidence of internal controls, not just initial documentation. Your systems should capture and flag suspicious patterns automatically.

Steps to build compliant KYC/AML processes:

- Document beneficial ownership with certified corporate structure charts and shareholder registers

- Prepare source of funds documentation tracing capital origins through audited statements

- Implement transaction monitoring systems with clear threshold alerts and investigation protocols

- Establish customer due diligence procedures matching FATF recommendations for your risk level

- Create compliance manuals detailing policies, procedures, and staff responsibilities

- Schedule regular external audits validating control effectiveness and regulatory adherence

- Maintain ongoing training programs ensuring staff understand current AML/CFT obligations

Adopt enhanced due diligence measures tailored to your sector and jurisdiction. Generic compliance programs fail because they do not address specific risks banks identify in crypto, iGaming, or forex operations.

Your documentation package should include:

- Detailed business plan explaining revenue models and customer segments

- Licensing documentation from relevant authorities

- Compliance policies covering AML, KYC, data protection, and fraud prevention

- Transaction monitoring reports demonstrating system effectiveness

- Internal audit findings and remediation actions

- Risk assessments identifying and mitigating sector-specific threats

Pro Tip: Engage compliance consultants experienced with high-risk EU banking to optimize success. They understand bank expectations and can identify documentation gaps before submission, saving months of application delays.

Review the high-risk bank account documents guide and high-risk bank onboarding guide to understand how structured KYC effectiveness translates into banking access.

Alternative Financial Solutions for High-Risk Businesses

Crypto payment gateways offer operational resilience when traditional banking proves difficult. They lower chargeback risks through irreversible transactions and speed up settlement times from days to minutes.

Benefits of crypto payment solutions:

- Near-zero chargeback risk compared to card payments

- Faster settlement reducing cash flow gaps

- Lower processing fees than traditional merchant accounts

- Global reach without currency conversion complications

- Reduced dependency on single banking relationships

Limitations require careful consideration. Regulatory challenges persist as jurisdictions implement varying crypto frameworks. Price volatility can erode margins if you do not convert immediately to stablecoins or fiat. Limited universal acceptance means many customers still prefer traditional payment methods.

Best practice combines crypto payments with compliant bank accounts. This hybrid approach provides payment diversity, operational backup, and customer choice. iGaming platforms increasingly use this model to mitigate banking risks while maintaining broad payment acceptance.

Real-world application shows effectiveness. A mid-sized iGaming operator might process 60% of deposits through crypto gateways while maintaining EUR and GBP bank accounts for withdrawals and operational expenses. This structure reduces bank exposure while preserving essential fiat services.

Crypto infrastructure should complement, not replace, your banking strategy. You still need bank accounts for regulatory compliance, payroll, supplier payments, and customer trust. Pure crypto operations face licensing obstacles and limit your addressable market.

Explore crypto payment gateways to understand how integrating these solutions within your broader financial architecture reduces vulnerability to banking access challenges.

Explore Expert Solutions for High-Risk Business Banking Success

Specialized checklists and compliance guides significantly increase success rates by addressing bank concerns systematically. Access to banks actively onboarding high-risk sectors in 2026 eliminates wasted applications to institutions with blanket rejection policies. Tailored consulting bridges knowledge gaps for EU crypto, iGaming, and forex firms navigating complex regulatory landscapes.

Start with the high-risk business banking checklist to audit your readiness before applications. Learn how to pass bank compliance through proven frameworks developed specifically for high-risk sectors. Discover top banks onboarding high-risk clients to focus your efforts on receptive partners.

Frequently Asked Questions

Why do banks reject compliant high-risk businesses?

Banks reject compliant businesses primarily due to reputational risk fears, not actual compliance deficiencies. They worry that any incident in high-risk sectors triggers regulatory investigations and negative publicity regardless of individual client quality. Risk-averse policies exclude entire sectors to avoid potential consequences.

How can I improve my chances of banking approval in the EU?

Improve approval chances by selecting crypto-friendly jurisdictions like Malta or Switzerland, preparing comprehensive KYC/AML documentation before application, and implementing robust compliance systems with transaction monitoring. Target banks specializing in your sector rather than mainstream institutions with blanket high-risk rejections.

Are crypto payment gateways a full replacement for bank accounts?

Crypto gateways complement but cannot fully replace bank accounts for most businesses. You still need fiat banking for regulatory compliance, payroll, supplier payments, and serving customers preferring traditional methods. Best practice uses hybrid solutions combining crypto payments with compliant banking relationships.

Which EU jurisdictions are friendliest for high-risk banking?

Malta, Switzerland, and the UK offer the most favorable environments for high-risk banking in 2026 due to established regulatory frameworks for crypto and iGaming. These jurisdictions provide clarity that reduces bank uncertainty, improving approval rates compared to markets with ambiguous or evolving regulations.

What common mistakes cause banking application failures?

Common failures include incomplete beneficial ownership documentation, inadequate source of funds evidence, generic compliance policies not addressing sector-specific risks, targeting banks without high-risk specialization, and poor preparation of business plans explaining revenue models. Addressing these gaps before submission dramatically improves outcomes.