High-risk businesses relying on single banking relationships face existential risk from account closures, policy changes, and regulatory shifts. UK account closures surged 44% in 2024, demonstrating that banking access can evaporate overnight regardless of business legitimacy. This guide explains how to build redundant banking infrastructure across multiple jurisdictions and banking partners, ensuring operational continuity when individual relationships encounter difficulties. Resilient banking structures demand strategic planning from inception rather than reactive scrambling during crises.

Key takeaways

| Point | Details |

|---|---|

| Single banking relationships create existential risk | 44% account closure rate in UK; regulatory changes can terminate relationships instantly |

| Diversification prevents operational disruption | Multiple accounts across different banks/EMIs ensure continuity if one relationship fails |

| Jurisdictional redundancy provides stability | Accounts across EU and offshore jurisdictions reduce vulnerability to regional regulatory shifts |

| Backup accounts require proactive setup | Establishing secondary relationships during normal operations prevents crisis-mode scrambling |

| Cost is investment in continuity | Maintaining multiple accounts increases expenses but prevents catastrophic disruption costs |

| Hybrid structures balance credibility and flexibility | Combining EU banks (credibility) with EMIs (flexibility) optimises resilience and operational efficiency |

Understanding banking fragility for high-risk sectors

High-risk businesses operate in uniquely fragile banking environments. Traditional banks increasingly view crypto, iGaming, Forex, and adult entertainment as reputational liabilities rather than commercial opportunities. Regulatory pressure intensifies continuously, with compliance costs rising and approval rates falling. This creates a fundamental mismatch: high-risk sectors require stable banking relationships to operate, yet face continuous risk of sudden account termination without warning or appeal.

Banking relationships in high-risk sectors lack the stability mainstream businesses enjoy. A mainstream company can rely on established banking relationships lasting decades unless severe misconduct occurs. High-risk businesses operate under the constant threat of policy changes: regulatory shifts can trigger instant relationship terminations, reputational concerns can surface unexpectedly, compliance review results can change banking partner appetites overnight. According to the Financial Conduct Authority (FCA) guidance on account closure and exit from banking relationships, banks can terminate high-risk accounts with minimal notice when risk appetites change.

The operational consequences of unexpected account closure prove catastrophic for high-risk businesses. Payment processing interruptions immediately damage customer relationships and revenue continuity. Float management becomes impossible, preventing operational expense coverage. Growth financing halts as credit facilities disappear. Vendor relationships become uncertain when payment capabilities vanish. Rebuilding banking relationships takes months, during which competitive position erodes and customer trust deteriorates.

Pro Tip: Assume all banking relationships have finite lifespans. Plan not if but when your primary banking partner terminates the relationship. Resilient structures treat secondary accounts as operational necessities, not backup luxuries. This mindset shift from hoping relationships endure to planning for inevitable changes transforms your banking stability fundamentally.

Building multi-account banking infrastructure

Resilient banking structures combine multiple accounts strategically across different dimensions: banking partners, account types, jurisdictions, and currencies. Rather than viewing secondary accounts as expensive insurance, treat them as core operational infrastructure enabling business continuity. This strategic reframing changes investment calculus: the expense of maintaining secondary accounts becomes justified as operational resilience investment.

Primary operational structure typically includes a main EU bank account providing institutional credibility and investor-friendly positioning, coupled with EMI accounts handling transaction volume and payment processing. This combination provides credibility for external relations (investors, partners, regulators) whilst ensuring operational flexibility and transaction processing capability. The EU bank account may process minimal volume; its primary function involves institutional signalling rather than transaction processing.

Secondary operational accounts introduce redundancy across multiple dimensions. A secondary EU bank account with different institution provides backup if primary relationship terminates. Secondary EMI accounts with different providers ensure payment processing capability survives single EMI failure. These accounts should handle meaningful volume even during normal operations, preventing the backup account perception that triggers regulatory scrutiny.

Jurisdictional diversification extends protection beyond single-region vulnerability. Accounts across EU and offshore jurisdictions provide continuity if regional regulatory changes trigger mass account terminations. Offshore accounts buffer against EU regulatory tightening; EU accounts provide market access if offshore relationships encounter compliance difficulties. This geographical distribution ensures that regional regulatory shifts cannot simultaneously disrupt all banking relationships.

| Account Layer | Primary | Secondary | Tertiary | Purpose |

|---|---|---|---|---|

| EU Bank Account | Bank A | Bank B | — | Institutional credibility |

| EMI Account | EMI X (EU) | EMI Y (EU) | EMI Z (Offshore) | Payment processing |

| Offshore Account | Bank C (Cayman) | Bank D (UAE) | — | Geographic diversification |

| Currency Accounts | EUR, GBP | EUR, USD | EUR, JPY | Multi-currency flexibility |

Practical implementation requires careful timing and positioning. Establish secondary accounts during periods of banking relationship stability, not during crises. Banks view account creation patterns; opening new accounts only after relationship problems signals desperation and triggers additional scrutiny. Conversely, proactive diversification during normal operations signals prudent risk management.

Jurisdictional strategy and regulatory positioning

Jurisdictional diversification provides strategic advantages beyond simple redundancy. EU accounts provide market access and regulatory alignment within European operations. Offshore accounts provide operational flexibility and cost advantages. Combining both enables strategy-driven positioning rather than forced compliance with constraints of single jurisdiction.

EU jurisdictions offer automatic market access, simplified cross-border transactions with EU customers, and regulatory alignment with European regulatory frameworks. However, EU jurisdictions impose higher compliance costs, stricter regulatory requirements, and increasingly hostile attitudes towards high-risk sectors. Recent regulatory tightening including MiCA (Markets in Crypto-Assets Regulation) and enhanced AML/CFT requirements elevate EU banking complexity.

Offshore jurisdictions like Cayman Islands, UAE, and Malta offer faster licensing timelines, clearer crypto/iGaming regulatory frameworks, and 30-50% lower compliance costs. These jurisdictions actively compete for high-risk business, maintaining sophisticated regulatory frameworks balancing oversight with innovation support. However, offshore jurisdictions lack automatic EU market access, requiring careful structuring for European customer operations.

Resilient structures combine both: EU accounts for European market operations and regulatory positioning, offshore accounts for operational flexibility and cost management. This hybrid approach provides strategic optionality—you can shift operational balance between jurisdictions as regulatory environments evolve without losing functionality. According to ESMA (European Securities and Markets Authority) guidance on jurisdictional regulation, EU operations require specific regulatory alignment regardless of back-office jurisdiction.

Pro Tip: Structure jurisdictional accounts with clear operational purposes before regulatory pressure forces decisions. EU accounts handle customer-facing European operations; offshore accounts manage back-office functions, liquidity management, and non-EU market operations. This clear separation prevents the appearance of regulatory arbitrage whilst actually optimising both functions.

Implementation roadmap: Creating resilient banking infrastructure

Implementing resilient banking infrastructure requires systematic planning across several dimensions. Start by mapping your current banking relationships and identifying critical failure points: which accounts handle essential functions? Which relationships face regulatory vulnerability? Which banking partners show signs of appetite contraction? This honest assessment reveals where secondary account establishment provides most value.

Priority sequencing matters significantly. Establish primary EU account first if not already in place, providing institutional foundation. Simultaneously establish primary EMI account for payment processing, creating dual-source operational infrastructure. Both primary accounts should handle meaningful volume, establishing transaction history and banking partner confidence. Only after both primary accounts function smoothly should you establish secondary accounts, preventing appearance of desperation or rapid account cycling.

Secondary account establishment requires deliberate positioning. Applications should reference existing banking relationships as context, not as signals of difficulty. Banking partners evaluate new applicants partly on whether existing banking relationships appear healthy; if your application appears driven by primary relationship problems, approval likelihood drops dramatically. Position secondary accounts as growth infrastructure (“expanding transaction processing capacity”) rather than relationship failure response.

Currency diversification extends protection strategically. Primary accounts in EUR/GBP provide European operational currency stability. Secondary accounts in USD, JPY, CHF, or AED provide currency options when primary currency relationships face pressure. Multi-currency capabilities prevent situations where regulatory shifts against single-currency processing eliminate payment options.

Timeline expectations require careful management. Initial application to first account approval typically requires 2-4 weeks with proper preparation. Subsequent account establishment accelerates (existing banking relationships provide credibility), typically completing in 2-3 weeks per account. Total timeline for establishing resilient infrastructure (primary EU account + primary EMI + secondary EU account + secondary EMI + offshore account) typically requires 12-16 weeks from inception, suggesting planning should begin 6 months before operations require full redundancy.

Cost structure for resilient banking requires honest budgeting. Annual costs for maintaining 4-5 accounts across different jurisdictions typically range from £5,000-£15,000 in fees, plus transaction processing costs. This represents substantial ongoing expense but proves immaterial compared to costs of unexpected account closure: revenue disruption, customer relationship damage, rebuilding timeline, competitive disadvantage. The cost-benefit analysis strongly favours maintaining redundancy.

Regulatory relationships and ongoing management

Resilient banking infrastructure requires proactive regulatory relationship management. Regulators and banking partners view account diversification as responsible risk management when implemented transparently. However, they view rapid account cycling, hidden backup accounts, or apparent attempts to circumvent regulatory oversight negatively. The difference lies in transparency and strategic positioning.

Communicate clearly with banking partners about your multi-account strategy. Frame redundancy as business continuity planning: “We maintain secondary accounts to ensure uninterrupted service to our customers if any single relationship encounters difficulties.” This positioning signals prudent business management rather than regulatory evasion. Banking partners appreciate operators who maintain continuity planning.

Maintain consistent compliance standards across all accounts. Regulators evaluate high-risk businesses partly on whether they maintain equivalent compliance across multiple relationships. Inconsistent compliance across accounts raises suspicions about which relationships represent “real” operations versus which are contingency backup. Treat all accounts as primary from compliance perspective, maintaining equivalent AML/KYC standards, transaction monitoring, and documentation requirements.

Update banking partners on material business changes consistently. If regulatory environment shifts, regulatory guidance updates, or business model evolution occurs, communicate these changes proactively to all banking partners. Surprises discovered during compliance reviews trigger account scrutiny; proactive communication prevents misunderstandings and maintains trust.

According to EBA (European Banking Authority) guidelines on account opening decisions for high-risk businesses, transparency and proactive compliance communication represent key success factors for account acceptance and retention in high-risk sectors.

When resilient structures prevent catastrophic disruption

Real-world scenarios demonstrate resilient banking structure value clearly. Consider a crypto exchange experiencing sudden regulatory pressure in primary jurisdiction. Without secondary accounts, regulatory-driven account closure triggers immediate payment processing failure, customer fund lock-up, reputational damage, and lengthy recovery period. With resilient structure (secondary EU bank + secondary EMI + offshore backup), the exchange shifts payment processing immediately to secondary accounts, maintaining service continuity throughout regulatory resolution. Customer trust persists because service never interrupted; recovery moves from crisis management to routine operations resumption.

Alternatively, imagine an iGaming operator when a banking partner faces its own regulatory challenge. Mainstream bank consolidation, regulatory action against financial institution, or compliance failure at banking partner sometimes triggers sudden closure of entire high-risk client portfolios. Primary account closure would disrupt the operator’s operations severely. Secondary accounts enable seamless transition to backup relationships whilst primary account challenges resolve.

These scenarios occur regularly across high-risk sectors. Operators maintaining single banking relationships face existential threats; operators maintaining resilient structures experience these events as operational inconveniences rather than business threats. The strategic value of redundancy becomes obvious in crisis moments.

Mitigating Risks: Compliance and Best Practice

Compliance is not a department. It is a business function that determines whether your company survives or collapses.

For high-risk fintech, compliance failures do not result in warnings. They result in account closures, regulatory fines exceeding your annual revenue, and criminal investigations of senior staff.

Effective compliance risk management requires a structured approach:

- Identify risks: Understand which regulations apply to your specific business model in each jurisdiction

- Assess severity: Prioritise which compliance gaps pose the greatest threat to your banking relationships

- Monitor continuously: Track regulatory changes and internal control effectiveness monthly, not annually

- Mitigate systematically: Implement controls that reduce risk to acceptable levels

- Document everything: Maintain evidence that you identified, assessed, and addressed compliance risks

Effective compliance risk management involves identifying, assessing, monitoring, and mitigating regulatory risks to ensure legal and ethical operation. Banks develop comprehensive risk frameworks, prioritise compliance activities, and leverage technology for automation. Senior management engagement is critical—this cannot be delegated to junior compliance staff.

Compliance culture means your CFO, product lead, and customer support team all understand that compliance protects the business. It is not an obstacle to overcome.

Your specific compliance obligations depend on your business model. Crypto exchanges face different requirements than iGaming platforms, which differ from forex brokers. But all high-risk businesses must master these fundamentals:

Anti-Money Laundering (AML) and Know-Your-Customer (KYC) controls form the foundation. You must verify customer identity, understand their source of funds, and monitor transactions for suspicious patterns. Mistakes here trigger immediate account freezes.

Banks implement robust customer due diligence and transaction monitoring alongside staff training and automated compliance tools to mitigate ongoing risk. Real-world cases demonstrate that non-compliance carries severe consequences, making strong controls and ethical standards non-negotiable.

Your compliance infrastructure must include:

- Customer Due Diligence (CDD): Verify identity, address, and beneficial ownership using independent documentation

- Ongoing Monitoring: Screen transactions against sanctions lists monthly and review unusual account behaviour quarterly

- Staff Training: Annual compliance training for all employees covering AML, GDPR, and your specific regulatory obligations

- Automated Tools: Compliance software that flags suspicious transactions, reducing human error and demonstrating diligence to regulators

- Audit Trails: Complete records of every compliance decision, approval, and exception to investigations

Most regulatory investigations begin when banks discover compliance gaps during their own audits of your account. Your banking partner notifies regulators before notifying you. By then, your account is already compromised.

Prevention requires proactive internal audits. Conduct quarterly reviews of your AML controls, KYC files, and transaction monitoring systems. If you discover gaps, fix them immediately and document the remediation.

The following table summarises key compliance and security controls fintechs must demonstrate to maintain trusted banking relationships:

| Control Area | Expected Evidence | Typical Oversight |

|---|---|---|

| Customer Due Diligence | Copies of verified documents | Automated screening |

| Transaction Monitoring | Real-time suspicious activity alerts | Internal and external audits |

| Data Encryption | Protocol deployment records | Regular third-party testing |

| Incident Response | Documented resolution process | Executive-level reviews |

| Staff Training | Certificates and attendance logs | Annual mandatory sessions |

Pro tip: Hire an external compliance audit firm annually, even if not required. When regulators investigate, they treat internally-discovered gaps far more leniently than externally-discovered ones. Audit reports demonstrate good faith effort to maintain standards.

Why defence-in-depth matters: Layering encryption for real-world resilience

Encryption and key management are necessary but still insufficient on their own. The Verizon DBIR 2025 confirms that data breaches remain frequent and costly, and ransomware attackers have become adept at navigating around encryption by targeting the humans and processes that control keys rather than the cryptographic algorithms themselves.

“Attackers do not break encryption. They find the person or process that holds the key and compromise that instead.”

The attack surface in a high-risk banking environment extends far beyond the data layer. Endpoint devices, identity and access management (IAM) systems, API gateways, and third-party integrations all represent potential entry points. Results Technology consistently emphasises that monitoring, penetration testing, and certificate hygiene are the controls that close the gaps encryption leaves open.

A practical layered control checklist for high-risk banking environments:

- Implement TLS 1.3 for all external communications and enforce certificate pinning for mobile applications.

- Deploy a Security Information and Event Management (SIEM) system with real-time alerting on anomalous decryption events.

- Conduct penetration testing at least annually, with a specific focus on key extraction and lateral movement scenarios.

- Enforce multi-factor authentication (MFA) on all systems with access to encrypted data or key management infrastructure.

- Automate certificate renewal to eliminate expiry-related outages and man-in-the-middle exposure windows.

- Segment networks so that a compromise in one zone cannot propagate to the zone holding encryption keys or cryptographic infrastructure.

For secure data-powered banking operations, these controls are not optional enhancements. They are foundational. Operators who build comprehensive security strategies with layered controls consistently demonstrate stronger compliance postures and face fewer onboarding rejections from banking partners.

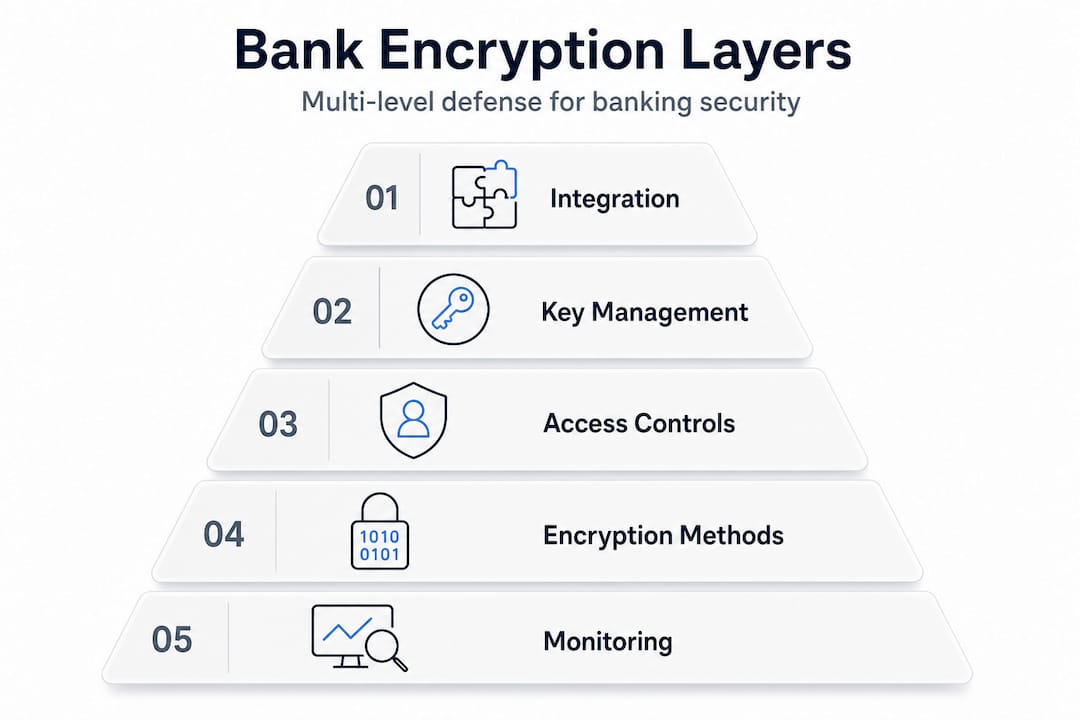

Data Protection and Encryption Protocols

Encryption is not optional for your fintech business. It is the foundation that allows regulators and banking partners to trust you with customer data and funds.

Without encryption, every transaction, every customer document, and every internal communication is readable to anyone with network access. Regulators will not permit this. Banks will not work with you.

Financial institutions deploy multiple encryption approaches depending on the data type and risk level:

- Symmetric encryption: Single shared key that encrypts and decrypts data. Fast and efficient for large datasets but requires secure key distribution

- Asymmetric encryption: Two keys (public and private) enabling secure data exchange without sharing secrets. Slower but critical for authentication

- Hybrid encryption: Combines both methods for optimal speed and security across different data flows

- End-to-end encryption: Data remains encrypted from sender to recipient, with only authorised users holding decryption keys

Encryption techniques for financial data security include symmetric, asymmetric, and hybrid protocols that protect sensitive information in fintech applications. Emerging techniques like homomorphic encryption allow you to analyse customer data without actually decrypting it—meeting both security and operational requirements.

End-to-end encryption ensures customer payment data never exists in plaintext on your servers. Banks and regulators expect this as standard practice, not optional feature.

Beyond encryption algorithms, you must implement specific security protocols that regulators mandate. The European Union requires eIDAS digital certificates for authenticating identity during secure data exchanges. These certificates prove that communications genuinely originate from verified participants, not imposters.

Banks use EU-mandated eIDAS certificates alongside Pretty Good Privacy (PGP) keys to ensure message authenticity and integrity. PGP provides both encryption and digital signatures, guaranteeing that customer payment orders remain confidential and unaltered during transmission.

Your data protection architecture must address:

- Data in transit: All customer information moving between systems uses encryption with strong cipher suites (AES-256 minimum)

- Data at rest: Customer records stored on servers remain encrypted using industry-standard protocols

- Key management: Encryption keys are rotated regularly, stored in hardware security modules, and accessible only to authorised systems

- Access controls: Only staff members requiring specific data can decrypt it, with logging of every access

Compliance with frameworks like PCI-DSS (for payment card data) and GDPR (for any European customer data) mandates these controls explicitly. Your banking partners verify that you implement them correctly before approving your account.

Most high-risk fintechs fail not because their encryption is weak but because their key management is chaotic. Keys stored in accessible locations, shared across too many staff members, or rotated infrequently create vulnerabilities that attackers exploit.

Pro tip: Use a dedicated hardware security module (HSM) from a reputable vendor to store encryption keys. Never keep encryption keys on the same servers that encrypt data. This architectural separation is the single most effective way to demonstrate security maturity to banking partners.

How encryption actually works: Methods and implementation in banking

Encryption is not one technology. It is a family of methods, each suited to different situations in a banking environment.

Symmetric encryption uses the same key to encrypt and decrypt data. It is fast and efficient, which makes it ideal for encrypting large volumes of stored data, such as transaction records or customer databases. AES-256 is the standard bearer and is accepted across all major regulatory frameworks.

Asymmetric encryption uses a public key to encrypt and a private key to decrypt. It is computationally heavier but solves the key distribution problem. TLS handshakes, for example, rely on asymmetric cryptography to establish a shared session key, after which symmetric encryption takes over for the actual data transfer.

| Method | Use case | Speed | Key complexity |

|---|---|---|---|

| AES-256 (symmetric) | Database encryption, stored files | Fast | Single shared key |

| RSA / ECC (asymmetric) | TLS handshakes, digital signatures | Slower | Public/private key pair |

| Tokenisation | Payment card data substitution | Near-instant | Vault-based lookup |

| Format-preserving encryption | PAN data in legacy systems | Moderate | Structured key management |

Protecting data in motion requires TLS 1.2 as a minimum, with TLS 1.3 strongly preferred for new deployments. VPNs add a further layer for internal traffic between distributed infrastructure nodes. Anything below TLS 1.2 should be treated as a critical vulnerability and remediated immediately.

Protecting data at rest goes beyond full-disk encryption. Regulators expect column-level or table-level database encryption for sensitive fields, file-level encryption for document stores, and tokenisation for payment card numbers where the actual PAN value does not need to be retained.

Advanced methods worth understanding:

- Authenticated encryption (AE/AEAD): Simultaneously protects confidentiality and verifies integrity. GCM mode with AES is the most widely deployed variant and is specified in EPC guidance.

- Homomorphic encryption: Allows computation on encrypted data without decrypting it first. Still emerging in production banking environments but increasingly relevant for privacy-preserving analytics.

- Format-preserving encryption (FPE): Encrypts data whilst retaining its original format, critical for legacy systems where database schemas cannot be changed.

Pro Tip: Never rely on your cloud provider’s default encryption settings. Defaults are designed for broad compatibility, not regulatory compliance. Review each setting explicitly against your applicable frameworks before going live.

Encryption for crypto banking environments demands particular attention to wallet key infrastructure and API gateway encryption, both of which have caused significant losses when poorly implemented. For reference on bank-grade encryption reliability, mature implementations combine multiple layers rather than relying on any single method.

According to Results Technology, real effectiveness comes from integration with key management, access controls, and monitoring. The technology is only as strong as the processes surrounding it.

BankMyCapital guidance on building resilient banking structures

BankMyCapital specialises in helping high-risk businesses establish and maintain resilient banking infrastructure across multiple jurisdictions. Our 87% approval rate reflects expertise in positioning applications so that multiple account approvals succeed rather than triggering suspicion about rapid application cycling. We advise on optimal jurisdictional combinations, account sequencing, and regulatory positioning ensuring your resilient structure commands banking partner confidence rather than triggering scrutiny.

Our approach combines strategic planning with expert implementation. We assess your operational requirements, identify critical failure points in current banking relationships, recommend optimal secondary and tertiary account structures, and guide implementation timing ensuring smooth account establishment without triggering regulatory concerns. Our ongoing relationship management prevents the compliance inconsistencies that damage multi-account strategies.

Contact BankMyCapital for comprehensive resilient banking architecture design tailored to your specific operational requirements, or explore our full banking solutions to understand how strategic redundancy strengthens your long-term banking stability.

Recommended

- EU Banks vs EMIs for High-Risk Businesses

- Bank Account Pre-Approval Strategy for High-Risk Companies

- Banking Compliance Best Practices for High-Risk Accounts

- Complete Guide to Opening High-Risk Bank Accounts

Frequently asked questions

How much does maintaining multiple banking accounts actually cost?

Typical annual costs for resilient banking infrastructure range from £15,000-£35,000 in account fees and compliance costs for 4-5 accounts across different jurisdictions. This varies significantly based on transaction volumes—higher volumes may trigger lower percentage-based fees, reducing relative costs. Compare this against costs of unexpected account closure: operational disruption, customer relationship damage, revenue loss, and rebuilding timeline typically exceed £100,000 in total impact. The cost-benefit analysis strongly supports maintaining redundancy.

Will opening multiple accounts trigger regulatory suspicion?

Not if structured transparently. Regulators and banking partners view diversification as responsible risk management when communicated clearly. The key involves framing secondary accounts as business continuity planning rather than hidden backup infrastructure. Transparency prevents misunderstandings; secrecy or rapid account cycling triggers scrutiny. Establish accounts during stable operational periods, maintain equivalent compliance standards across all accounts, and communicate material changes proactively to all banking partners.

How long does establishing a resilient banking structure take?

Timeline from inception to full multi-account redundancy typically requires 12-16 weeks. Primary account establishment takes 2-4 weeks; subsequent accounts establish faster (2-3 weeks each) as existing banking relationships provide credibility. Plan initiation 6 months before operations require full redundancy, allowing gradual infrastructure build rather than crisis-mode establishment. Rushed account establishment appears suspicious and reduces approval likelihood.

Should all accounts handle equal transaction volumes?

Primary accounts should handle meaningful volumes establishing genuine transaction history and banking partner confidence. Secondary accounts benefit from handling adequate volume to remain operationally viable if primary relationship terminates, but can typically operate at lower volumes than primary accounts. The key involves preventing backup account perception—treat all accounts as primary from compliance and relationship perspective, with volume distribution reflecting operational efficiency rather than backup positioning.

How do I know which jurisdictions to prioritise for account diversification?

Evaluate your customer base geographic distribution, operational requirements, and growth trajectory. EU accounts make sense for European customer concentration; offshore accounts make sense for global operations or non-EU customer bases. Combine both for geographic diversification protecting against regional regulatory shifts. Your industry sector influences jurisdiction selection—crypto operations benefit from Cayman Islands or UAE jurisdictions with developed crypto regulatory frameworks; iGaming benefits from Malta or Curacao with gambling-specific licensing frameworks.