TL;DR:

- Running a crypto business in Europe requires understanding multi-layered infrastructure and compliance frameworks to secure banking relationships. Effective management of blockchain layers, KYC, AML, and Travel Rule protocols builds resilience against regulatory and banking risks, especially under strict EU regulations. Mastering crypto infrastructure offers high-risk businesses a competitive advantage by enhancing operational resilience and compliance credibility.

If you run a crypto business in Europe and your banking applications keep getting rejected, the problem is rarely your product. It is almost always your infrastructure and compliance posture. Crypto infrastructure explained simply means understanding the technical and regulatory layers that power every transaction your business touches. Most operators treat it as an IT concern and hand it off. That is a costly mistake. Banks assess your infrastructure choices directly when evaluating risk. This guide breaks down what you actually need to know, from blockchain layers to EU compliance frameworks, and how getting it right turns banking relationships from impossible to achievable.

Key Takeaways

| Point | Details |

|---|---|

| Layered architecture | Crypto infrastructure is built in five essential layers from blockchain consensus to user applications, ensuring robust transaction processing. |

| Compliance is critical | Strict EU rules require full customer due diligence, sanctions screening, and long-term record retention for crypto transactions. |

| Stablecoins enable speed | Using stablecoins supports instant global payments with less volatility and lower cross-border costs than traditional methods. |

| Third-party providers help | Managed infrastructure services reduce operational burdens and facilitate compliance for high-risk crypto businesses. |

| Expertise enhances success | Mastering crypto infrastructure and workflows improves trust with banks and regulators, turning perceived risk into an advantage. |

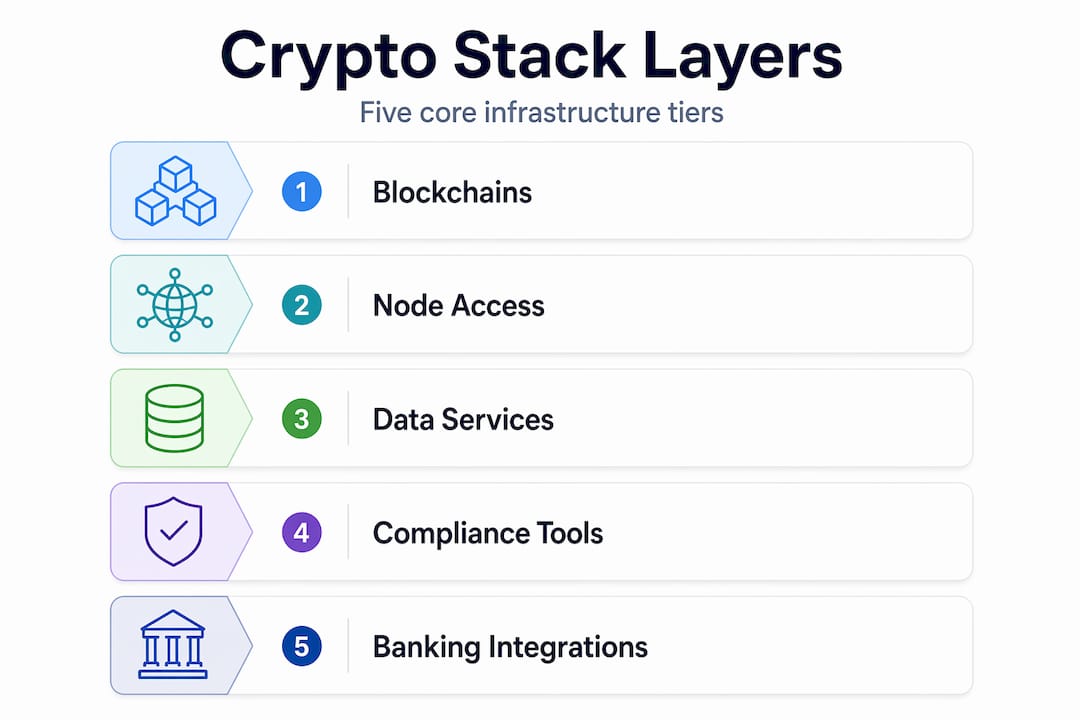

Understanding the layers of crypto infrastructure

The Web3 infrastructure stack consists of five layers, running from blockchain consensus at the base to user-facing applications at the top. Understanding this architecture is not optional for high-risk business owners. Every compliance and banking conversation you have will touch at least one of these layers.

Here is how the layers break down:

- Layer 1 blockchains such as Ethereum and Solana sit at the foundation. They handle consensus, transaction validation, and finality. Your choice of Layer 1 affects settlement speed, cost, and regulatory perception.

- Layer 2 networks such as Arbitrum or Polygon process transactions off the main chain and settle back to Layer 1, dramatically increasing throughput and reducing fees without sacrificing underlying security.

- Node access providers give your applications a managed RPC (Remote Procedure Call) endpoint to communicate with blockchains without running your own node infrastructure. This is where providers such as QuickNode become operationally critical.

- Data services index blockchain data and make it queryable in real time. Without them, pulling transaction histories or compliance-relevant records becomes impossibly slow.

- Application services handle identity verification, file storage, cross-chain messaging, and authentication. These sit just below the user-facing layer and are essential for building compliant workflows.

- The application layer is what your customers interact with: frontends, smart contracts, and backend APIs. This is where your product lives, but it only works correctly when every layer below it is sound.

Understanding crypto infrastructure basics at this level tells you something immediately useful. If your node access provider goes down, your payment rails go with it. If your data layer is poorly indexed, your transaction monitoring for AML purposes becomes unreliable. These are not abstract technical concerns. They are banking risk factors. Informed decisions about crypto payment processing start with understanding which layer each component occupies.

The role of crypto infrastructure in compliance and risk management

The blockchain infrastructure overview only makes sense when you map it onto what regulators actually require. Under the EU’s Anti-Money Laundering Regulation (AMLR), which was passed in 2024 and becomes active in 2027, CASPs face strict obligations with no minimum transaction threshold for customer due diligence. Every crypto transfer requires scrutiny.

Here is what compliant crypto operations must include under current and incoming EU frameworks:

- Customer due diligence on all transactions. There is no floor. Even micro-transactions require CDD under EU AMLR, which makes manual processes unviable. Your infrastructure must automate this.

- Verification of self-hosted wallets above €1,000. If a customer withdraws to a self-hosted wallet over this threshold, you are required to verify the wallet’s ownership.

- Five-year record retention. Transaction records and customer data must be held for a minimum of five years, with full audit trail integrity.

- 40 hours of AML training per year for each responsible staff member. This is not advisory. It is a formal obligation.

- Pre-execution sanctions screening. The EBA guidelines for CASPs require all crypto transfers to be screened against sanctions lists before execution, including fuzzy matching to catch name variations and disguised parties.

- Travel Rule compliance. Originator and beneficiary information must travel with every qualifying crypto transfer, aligning with FATF standards adopted in EU law.

Pro Tip: Do not treat compliance tooling as something to bolt on after you have built your payment infrastructure. AML transaction monitoring, KYC APIs, and Travel Rule solutions need to be integrated at the infrastructure planning stage. Retrofitting them is expensive and often means rebuilding core components.

A holistic approach covering KYC, transaction monitoring, and Travel Rule adherence is now the baseline for EU licensing acceptance. Review a detailed crypto compliance checklist to ensure you are not leaving gaps that will surface during banking due diligence. Strong risk management practices built into your infrastructure design is what separates businesses that get banked from those that do not.

Common crypto infrastructure options for high-risk business banking

With compliance requirements mapped out, the practical question becomes: which infrastructure components should your business actually use? Providers such as QuickNode demonstrate how managed services dramatically reduce the operational complexity of running your own nodes, which require constant maintenance, redundancy management, and significant DevOps resource.

| Infrastructure component | Build in-house | Use managed provider |

|---|---|---|

| Blockchain node access | High cost, high risk of downtime | Low cost, high uptime SLA |

| Wallet custody | Requires HSM and security audits | Available via WaaS platforms |

| KYC/AML tooling | Complex to build, slow to update | Regulatory updates included |

| Travel Rule compliance | Legal and technical complexity | Handled by specialist providers |

| Data indexing | Requires dedicated engineering | Available as API services |

Key options to evaluate for your crypto banking setup include:

- Wallet-as-a-Service (WaaS) platforms that support over 300 crypto assets and 80 or more networks, allowing you to launch custody and payment infrastructure quickly without building from scratch.

- Blockchain APIs that provide stable RPC access, transaction broadcasting, and webhook notifications for payment confirmations.

- Integrated compliance suites that bundle KYC, AML screening, and Travel Rule modules into a single vendor relationship, simplifying due diligence reporting for your banking partners.

- Multi-sig and MPC (Multi-Party Computation) custody for institutional-grade asset security that satisfies banking partner requirements.

Pro Tip: When evaluating providers, ask specifically what their uptime SLA is during network congestion events. Many providers quote average uptime but their performance degrades precisely when transaction volumes spike. That is exactly when your business cannot afford failures.

Choosing providers that offer built-in compliance tooling is not just operationally convenient. It materially improves your application when you approach banking partners for a crypto banking setup or need a business bank account without local entity setup. Banks want to see that your infrastructure has compliance baked in, not stapled on.

Nuances of stablecoins and payment processing in crypto infrastructure

Stablecoins deserve a section of their own because they have fundamentally changed what high-risk businesses can do operationally. USDC and USDT, pegged to the US dollar, eliminate the volatility that makes treasury management difficult when you are holding crypto balances. Stablecoins provide near-instant global settlement, bypassing the two to five business day delays and significant fees associated with SWIFT-based cross-border payments.

Here is how stablecoins fit into a practical business infrastructure:

| Use case | Traditional banking | Stablecoin-based |

|---|---|---|

| Cross-border supplier payment | 2-5 days, 2-4% fee | Minutes, sub-1% fee |

| Customer refund | 3-7 days | Near-instant |

| Treasury conversion | T+2 settlement | Continuous |

| Programmable payment | Not possible | Smart contract-enabled |

New BaaS (Banking as a Service) models built around stablecoins now enable self-custodial wallets that reduce reliance on intermediaries. For high-risk businesses, this means fewer counterparty risks and more direct control over fund flows. That matters enormously when traditional banking access is restricted.

Stablecoin use cases relevant to your operations include:

- Customer payment acceptance in USDC or USDT, converting to fiat via regulated off-ramps

- Supplier and affiliate payouts in real time, globally, without correspondent banking friction

- Cross-border remittances at a fraction of traditional costs

- Programmable payments via smart contracts, such as milestone-based fund releases

Under MiCA, stablecoins classified as e-money tokens or asset-referenced tokens face specific reserve and redemption requirements. Choosing a compliant stablecoin issuer is therefore part of your crypto payment processing due diligence, not an afterthought.

Pro Tip: If you are using USDC for treasury operations, ensure your off-ramp provider is MiCA-registered or holds an e-money licence in the EU. This protects you from regulatory exposure as enforcement tightens through 2026 and 2027.

Building a compliant crypto banking and payment workflow

Understanding how crypto infrastructure works is only useful if you translate it into a workflow. Here is a structured approach for building compliant crypto banking operations that will hold up under regulatory and banking scrutiny:

- Appoint a qualified MLRO (Money Laundering Reporting Officer). This individual must have demonstrable crypto-sector experience. Banks and regulators will ask for their CV and qualifications during onboarding.

- Implement KYC/AML procedures aligned to EU AMLR. Apply standard due diligence for routine customers and enhanced due diligence for high-risk profiles, jurisdictions, and transaction sizes. Automate where possible using API-based KYC providers.

- Integrate Travel Rule compliance from day one. Use a Travel Rule protocol such as TRISA or OpenVASP to capture and transmit originator and beneficiary data for all qualifying transfers.

- Deploy pre-execution sanctions screening. Every transaction must be screened before it is broadcast to the network. Post-execution screening is not compliant under EBA guidelines.

- Establish multi-year record retention. Five years minimum under AMLR. Use encrypted, auditable storage with access logging to satisfy both regulatory and banking requirements.

- Document and log AML training. Keep records of training sessions, materials used, and hours completed per staff member. This documentation is requested during banking due diligence reviews.

Unified compliance functions that integrate KYC, Travel Rule, and AML transaction monitoring are what regulators expect from CASPs in 2026. Building separate siloed systems that do not share data creates gaps that surface during audits.

Pro Tip: Approach your target banking partner before your compliance infrastructure is complete. Share your compliance roadmap and intended provider stack. Banks value transparency and early engagement significantly reduces the risk of rejection once you submit a formal application.

Work through a thorough crypto compliance checklist and align it with the requirements outlined by your intended banking jurisdiction. Understanding crypto banking for high-risk industries specifically means knowing what documentation banks will request before you walk in the door.

Why mastering crypto infrastructure is a competitive advantage for high-risk businesses

Most operators in the crypto sector treat infrastructure as a cost centre and compliance as a legal checkbox. That framing is precisely why so many high-risk businesses fail to secure banking relationships. The businesses that do get banked, and stay banked, treat infrastructure mastery as a genuine business advantage.

Decentralisation means no single point of failure, and that design principle extends beyond the technical layer. When you build a crypto operation with distributed node access, multiple custody options, and redundant compliance tooling, you are not just reducing technical risk. You are building a business that is visibly more resilient to banking partners, auditors, and regulators.

The uncomfortable truth is this: understanding crypto infrastructure basics and compliance requirements gives you knowledge that most competitors lack. That gap is exploitable. A business that can walk a banking compliance officer through its transaction monitoring architecture, Travel Rule implementation, and sanctions screening process is treated categorically differently from one that hands over a vague tech summary and hopes for the best.

Failing to grasp the layered architecture and the evolving EU regulatory landscape does not just create compliance risk. It inflates your operational costs because you end up rebuilding infrastructure repeatedly as gaps emerge. It delays banking access by months. And it exposes you to regulatory action at precisely the moment your business is trying to scale.

The risk management practices of the most successfully banked crypto businesses share a common thread: they invested in understanding and documenting their infrastructure early. Reviewing your crypto banking setup with that level of deliberateness is not a technical exercise. It is the foundation of a scalable, rejection-resistant business.

Secure compliant banking solutions for high-risk crypto businesses

The complexity covered in this guide is real, and navigating it alone significantly increases the risk of banking rejection, compliance gaps, and wasted time. Bank My Capital specialises in helping high-risk crypto businesses secure regulated banking relationships in Europe and beyond, with an 87% approval rate and onboarding that typically completes in two to three weeks. Their network of over 50 pre-vetted banking partners and EMIs includes institutions specifically experienced with crypto infrastructure assessments. If you need a business bank account without a local entity, or require end-to-end support through the banking onboarding process, their compliance team handles jurisdiction selection, regulatory liaising, and documentation preparation so your application is positioned for approval from the first submission.

Frequently asked questions

What are the main layers of crypto infrastructure businesses should understand?

The crypto infrastructure stack includes five layers: foundational blockchains (Layer 1), node access providers, data services, application services covering identity and storage, and the user-facing application layer with smart contracts and frontends. Each layer carries distinct operational and compliance implications.

How do EU AML regulations affect crypto-asset service providers?

Under EU AMLR obligations, CASPs must perform customer due diligence on all transactions regardless of size, verify self-hosted wallets above €1,000, retain records for five years, and provide a minimum of 40 hours of AML training annually to compliance staff.

Why are stablecoins important for high-risk crypto businesses?

Stablecoins enable near-instant low-risk global payment settlement, removing the delays and costs of traditional cross-border banking and allowing businesses to manage treasury and compliance obligations without significant volatility exposure.

What should businesses consider when choosing crypto infrastructure providers?

Businesses should assess provider uptime guarantees, coverage across crypto assets and networks, built-in compliance tooling, integration support, and total cost. Providers offering managed services reduce both operational complexity and the technical burden on your internal team.