Most high-risk business owners assume crypto payment processing is either a cheap shortcut or a compliance minefield. The reality sits somewhere more nuanced. Standard payment gateways routinely reject crypto businesses, iGaming operators, and adult platforms outright, leaving decision-makers scrambling for alternatives with little reliable guidance. Fees, volatility, counterparty risk, KYC requirements — the variables pile up fast. This guide cuts through the noise and gives you a practical, compliance-focused breakdown of how crypto payment processing actually works, what it costs, and how to build a setup that supports rather than jeopardises your banking relationships.

Key Takeaways

| Point | Details |

|---|---|

| Know your gateway type | Understand the pros and cons of custodial and non-custodial gateways to match your risk and business needs. |

| Crypto fees often lower | Payment processing fees for crypto average lower than traditional cards, but confirm hidden costs. |

| Compliance is critical | Maintaining transparency and KYC/AML standards is essential for keeping banking relationships open. |

| Clarity beats low fees | A clear, compliant payment process is more valuable long-term than marginal cost savings. |

What is crypto payment processing?

At its core, crypto payment processing means accepting digital currencies such as Bitcoin, Ethereum, or stablecoins in exchange for goods or services. Rather than routing funds through a card network like Visa or Mastercard, transactions move across a blockchain, verified by a decentralised network of nodes.

The key players in any crypto payment flow are:

- The customer, who initiates a payment from their digital wallet

- The merchant, who receives funds either as crypto or converted fiat currency

- The crypto payment gateway, which acts as the intermediary, processing and routing the transaction

- Banking partners or EMIs, which facilitate fiat conversion and settlement where required

For high-risk sectors specifically, crypto payment processing matters because it opens doors that traditional card processors keep firmly shut. It expands your payment options, can significantly lower transaction costs, and enables banking relationships that would otherwise be inaccessible. Staying across crypto compliance trends is essential as regulators tighten their expectations globally.

That said, high-risk firms face distinct struggles even within the crypto space: sudden account closures, intense compliance scrutiny, and exposure to price volatility if funds are held in crypto rather than converted immediately.

Gateways broadly fall into two categories. Custodial gateways hold funds temporarily, offer fiat conversion, and are easier for beginners but introduce counterparty risk. Non-custodial gateways send funds directly to the merchant wallet, carry lower fees of 0 to 0.5%, and offer greater sovereignty but demand more technical competence. Before selecting either, review your crypto compliance checklist to ensure your chosen workflow meets current regulatory expectations.

Pro Tip: Choose a payment workflow that matches both your technical capability and your compliance obligations. A gateway that is technically superior but creates audit gaps will cost you far more in banking friction than it saves in fees.

One figure worth keeping in mind: the global crypto payments market is projected to exceed $4.5 billion in transaction volume by 2026, reflecting how rapidly mainstream adoption is accelerating even in regulated sectors.

Comparing custodial vs non-custodial crypto gateways

Now that you understand the basics, let us look more closely at the two gateway models and what they mean in practice for high-risk operators.

Custodial gateways offer ease of use and fiat conversion but introduce counterparty risk. Non-custodial gateways offer lower fees of 0 to 0.5% and more control, but require more technical setup. Here is a direct comparison:

| Feature | Custodial gateway | Non-custodial gateway |

|---|---|---|

| Fees | 0.5% to 1.5% | 0% to 0.5% |

| Ease of use | High | Moderate to low |

| Fiat conversion | Built-in | Manual or third-party |

| Compliance tools | Often included | Varies by provider |

| Counterparty risk | Present | Minimal |

| Settlement speed | 1 to 3 business days | Near-instant |

| Technical setup | Low | High |

Which model suits your business depends on your sector and operational priorities:

- Retail and eCommerce operators typically benefit from custodial gateways due to their simplicity and built-in fiat conversion

- iGaming and adult platforms often prefer custodial solutions for their compliance infrastructure, though non-custodial can work if internal technical resources are strong

- Privacy-focused or high-volume crypto-native businesses may extract more value from non-custodial setups, accepting the technical overhead in exchange for lower fees and greater autonomy

Counterparty risk deserves particular attention. It means a third-party provider temporarily holds your funds, and if that provider faces insolvency, regulatory action, or a security breach, your capital is exposed. For high-risk businesses already navigating fragile banking relationships, this is not a theoretical concern.

For practical guidance on structuring your gateway selection, review processing best practices tailored to high-risk operators.

Pro Tip: If your priority is fast banking integration and compliance documentation, custodial is generally the safer starting point. If you have strong internal technical resources and value autonomy, non-custodial can offer meaningful long-term advantages.

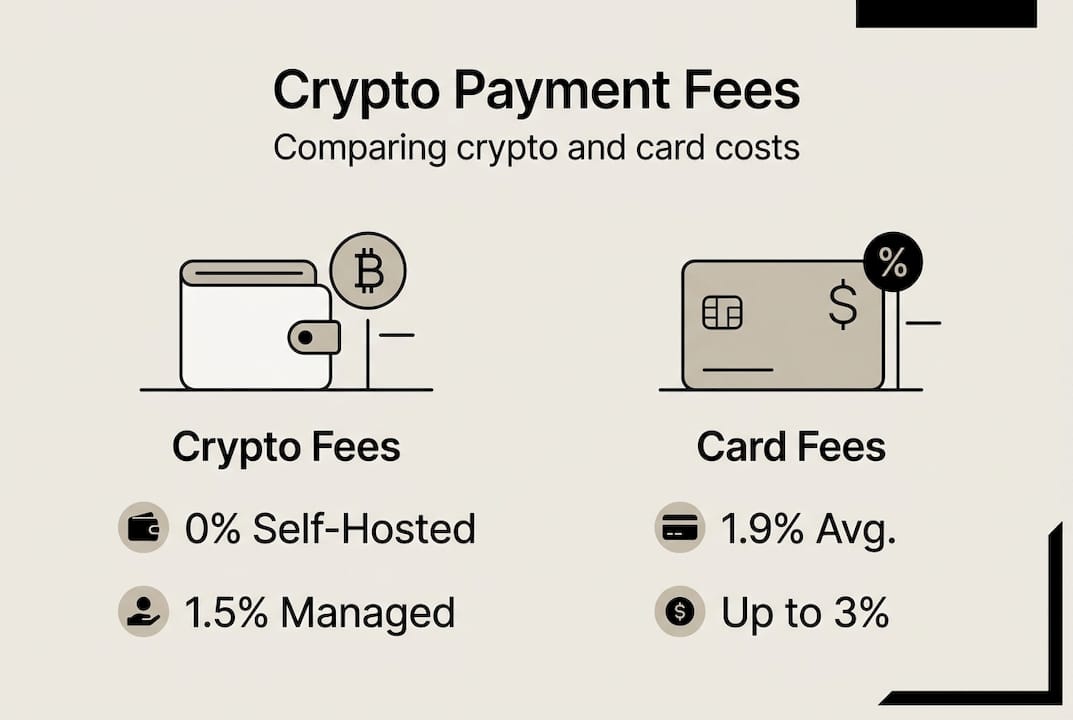

Understanding crypto payment fees versus traditional options

Once you have selected a gateway type, cost becomes the next critical variable. The fee landscape is more nuanced than most operators realise.

Fees range from 0% for self-hosted solutions like BTCPay Server to 1.5% for managed services like Stripe Crypto, with averages sitting between 0.5% and 1%. Traditional card processing typically runs from 1.5% to 3.5% plus additional charges. Here is how common options compare:

| Payment method | Typical fee range | Setup cost | Chargeback risk |

|---|---|---|---|

| BTCPay Server (self-hosted) | 0% | Technical time | Very low |

| Managed crypto gateway | 0.5% to 1% | Low to moderate | Low |

| Stripe Crypto | Up to 1.5% | Low | Low |

| Traditional card (Visa/Mastercard) | 1.5% to 3.5% | Low | High |

| High-risk card processor | 3% to 5%+ | Moderate | Very high |

Hidden costs in payment processing often appear in places operators overlook:

- Currency conversion fees, charged when converting crypto to fiat

- Withdrawal fees, applied when moving funds to a bank account

- Chargeback reserves, common with card processors but largely absent in crypto

- Integration costs, particularly relevant for non-custodial or self-hosted setups

- Compliance tooling, which some gateways charge for separately

The cost advantage of crypto is most pronounced for high-risk businesses. Traditional high-risk card processors routinely charge 3% to 5% or more, plus rolling reserves of 5% to 10% held for months. A crypto gateway at 0.5% to 1% with no reserve requirement represents a material operational saving.

For a broader view of your options, explore high-risk payment solutions designed specifically for sectors facing elevated processing costs.

Statistic: Businesses switching from high-risk card processors to crypto gateways can reduce effective processing costs by 60% to 80%, depending on volume and gateway selection.

Compliance and banking relationships: integrating crypto with the traditional system

Understanding costs brings us to a critical hurdle for high-risk businesses: aligning crypto payments with compliance and banking structures. This is where many operators stumble, not because they are non-compliant, but because their payment setup fails to demonstrate compliance clearly enough for banking partners.

Banks remain cautious about crypto for three primary reasons: the perceived risk of money laundering, inconsistent regulations across jurisdictions, and gaps in KYC (Know Your Customer) documentation. High-risk businesses face additional compliance hurdles and scrutiny with payment processors, especially when using crypto.

To maintain a compliant payment flow, follow these steps:

- Select a gateway with built-in KYC and AML tools to automate identity verification and transaction monitoring

- Ensure full transaction traceability so every payment can be traced from origin wallet to settlement account

- Maintain clear records of all conversions, settlements, and counterparty relationships

- Choose jurisdictions with clear crypto regulation, such as Lithuania, Malta, or Estonia within the EU

- Conduct regular internal audits to identify gaps before a banking partner or regulator does

- Work with banking partners who understand your sector and have pre-approved crypto business models

For a thorough overview of what banking partners expect, review crypto business banking compliance requirements and use the crypto banking setup framework to structure your approach from the outset.

Pro Tip: Use gateways with built-in compliance tools rather than bolting on third-party solutions afterwards. Integrated compliance creates cleaner audit trails, which directly improves your standing with banking partners.

Why clarity, not just cost, determines successful crypto payment operations

Here is something we observe consistently across high-risk operators: the businesses that struggle most are not those with the highest fees or the most complex technical setups. They are the ones whose internal processes are opaque, even to themselves.

Merchants frequently chase the lowest fees or fastest settlement times, treating gateway selection as a purely financial decision. But banking rejection is far more likely when compliance documentation is weak and transaction traceability is inconsistent, regardless of which gateway model you use. A beautifully optimised non-custodial setup with 0% fees is worthless if your banking partner cannot follow the money trail.

Sustaining operations in high-risk sectors depends on banking confidence. That confidence is built through clarity: clear processes, clear audit trails, clear counterparty relationships. Over time, the marginal savings from a lower-fee gateway are trivial compared to the cost of a banking relationship collapsing. Reviewing high-risk processing strategies with this lens changes the decisions you make at every stage of setup.

The businesses that thrive long-term are those that treat compliance infrastructure as a competitive advantage, not a cost centre.

Secure your high-risk business with compliant crypto payment solutions

If this guide has clarified one thing, it is that successful crypto payment processing is built on the right combination of gateway selection, fee awareness, and compliance infrastructure. At BankMyCapital, we work specifically with high-risk operators in crypto, iGaming, forex, and adult entertainment to connect them with compliant crypto payment solutions and banking partners who understand your sector. Our network of over 50 pre-vetted banks and EMIs means you avoid the banking rejection risks that derail most operators. Explore our full range of payment processing services or get in touch to discuss a tailored setup for your business.

Frequently asked questions

What types of crypto payment gateways are available for high-risk businesses?

High-risk businesses can choose custodial gateways, which handle fiat conversion with added counterparty risk, or non-custodial gateways, which provide direct transfers and lower fees but require more technical setup. Custodial and non-custodial gateways have distinct risk and technical trade-offs that should align with your operational capacity.

Are crypto processing fees always lower than card payments?

Crypto payment fees average 0.5% to 1.5%, which is often significantly lower than traditional card processing fees of 1.5% to 3.5% plus additional charges, though self-hosted solutions can reduce fees to zero.

How can high-risk businesses ensure their crypto payments stay compliant?

Firms should use gateways with built-in compliance tools and ensure all transactions are fully traceable, meeting KYC and AML standards. Compliance is a major concern for high-risk businesses using crypto payment processors, making integrated tooling essential.

What is counterparty risk in custodial crypto processing?

Counterparty risk means a third party holding your funds could restrict, freeze, or lose them before settlement. Custodial gateways introduce counterparty risk by temporarily holding funds during the processing cycle.