TL;DR:

- EU PSD2 has significantly reduced chargebacks for adult and dating businesses.

- Specialist EU EMIs and payment providers offer higher approval rates and operational benefits.

- Building a structured payment ecosystem with compliance and new payment tech is key to scaling.

Payment rejections, frozen accounts, and chargeback spirals are the everyday reality for dating business owners who rely on US-centric or offshore-only banking. What most owners don’t realise is that the EU’s regulatory architecture, specifically the Payment Services Directive 2 (PSD2), has measurably shifted the landscape in their favour: adult chargebacks dropped 22% to just 9.8% across EU-regulated processors in 2023, compared to significantly higher rates in the US. This guide breaks down exactly why EU banking works for high-risk dating firms, what it costs you to ignore it, and how to make the move strategically.

Key takeaways

| Point | Details |

|---|---|

| Lower chargebacks | EU regulations like PSD2 have dramatically reduced chargeback rates for dating businesses. |

| Reduced banking rejection | Specialist EU banks and fintechs enhance approval odds for high-risk companies. |

| Competitive processing fees | Modern EU payment rails such as Wero often yield lower fees than non-EU alternatives. |

| Strategic compliance support | Proactive compliance in the EU is a growth tool, not just risk management. |

| Expert partner advantage | Engaging EU specialists, not just mainstream banks, is key for sustainable dating business growth. |

Understanding high-risk status in dating businesses

Before you can solve a problem, you need to understand why it exists. Banks classify businesses as “high-risk” based on a cluster of factors that signal elevated financial exposure for the institution. Dating platforms tick almost every box on that list.

The main triggers for a high-risk classification include:

- High chargeback rates from subscription billing disputes and fraudulent transactions

- Adult or age-restricted content, which raises regulatory and reputational concerns

- Global customer bases with currency conversion risk and cross-border compliance complexity

- Subscription-based recurring billing, which generates more disputes than one-off purchases

- Fraud vulnerability, particularly synthetic identity fraud and card testing attacks

The practical consequences are severe. Expect higher processing fees (sometimes 3.5% to 5% per transaction), frequent requests for rolling reserves (often 10% to 15% of monthly volume held for 90 to 180 days), and outright rejection from mainstream processors like Stripe or PayPal. Even when you do get onboarded, the relationship can end abruptly if your chargeback ratio creeps above 1%.

“The EU’s PSD2 framework has been a turning point for adult and dating businesses. EU PSD2 reduced chargebacks by 22% to 9.8% in 2023, versus materially higher rates seen across US-processed transactions.”

This is where EU banking fundamentally diverges from alternatives. Rather than treating dating businesses as a liability to be managed, specialist EU institutions and Electronic Money Institutions (EMIs) have built structured onboarding pathways. Options like EMI bank accounts for dating businesses offer purpose-built frameworks that account for the sector’s specific risk profile. Similarly, pursuing proper licensing for dating businesses in EU jurisdictions dramatically improves your credibility with banking partners.

The distinction matters enormously. A dating platform with an EU licence and an EU-regulated banking partner isn’t just “accepted.” It’s operating within a system designed to handle its complexity.

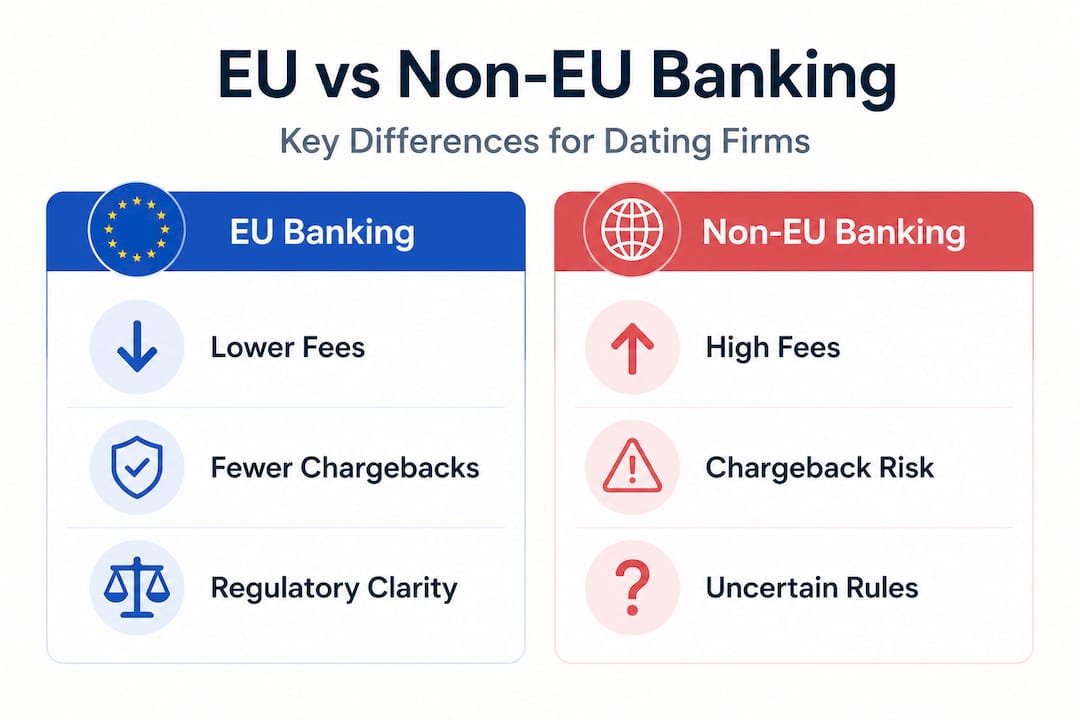

Key advantages of EU banking for high-risk dating firms

The EU banking ecosystem offers dating businesses a set of structural advantages that genuinely cannot be replicated by banking in the US, UK post-Brexit, or typical offshore centres. These aren’t marketing claims. They’re measurable operational benefits.

Pan-European payment rails and lower transaction fees

EU-based businesses gain access to the Single Euro Payments Area (SEPA), which covers 36 countries and enables low-cost, fast bank transfers. More importantly, the rise of account-to-account (A2A) payment schemes, particularly Wero, is reshaping cost structures for high-risk merchants. EU A2A like Wero reduces dependence on US card network dominance and can materially lower transaction costs compared to Visa and Mastercard rails. For a dating platform processing €500,000 per month, even a 0.5% saving in fees translates to €2,500 monthly directly back into your operation.

Regulatory clarity through PSD2 and its successors

PSD2 created a standardised framework for payment disputes, strong customer authentication (SCA), and processor accountability. This clarity benefits dating businesses because the rules are known, enforced consistently, and reduce the arbitrary account terminations that plague US-processed merchants. PSD3, currently progressing through EU legislative channels, is expected to tighten fraud liability further in ways that favour compliant, well-structured merchants.

Diversification away from US-centric risk

Over-reliance on US processors creates a single point of failure. US regulatory shifts, card network policy changes, and banking partner decisions can eliminate your payment infrastructure overnight. EU banking provides genuine geographic and regulatory diversification.

Pro Tip: Pairing with an EU specialist provider rather than a mainstream retail bank is not optional for dating businesses. Mainstream EU banks still reject high-risk applications. The real advantage comes from specialist EMIs and payment institutions that have pre-negotiated frameworks specifically for adult and dating platforms.

Here’s a quick comparison of what EU banking offers versus typical alternatives:

| Feature | EU specialist banking | US banking | Offshore banking |

|---|---|---|---|

| Chargeback rate (adult) | ~9.8% | ~12% to 15% | Variable, often higher |

| Regulatory clarity | High (PSD2/PSD3) | Moderate | Low |

| Account stability | High with specialist EMI | Low for high-risk | Moderate |

| A2A payment access | Yes (SEPA, Wero) | Limited | Rare |

| Compliance support | Structured and ongoing | Minimal | Often absent |

Understanding EU banking advantages at a structural level, and then cross-referencing them against EU banking regulations specific to high-risk sectors, gives you the full picture before you approach any institution.

EU versus non-EU banking: Compliance, cost, and chargebacks compared

Let’s make this concrete with numbers. The gap between EU and non-EU banking for dating businesses isn’t marginal. It’s the difference between a stable, scalable payment operation and a fragile one that requires constant firefighting.

Chargeback rates by geography

The PSD2 chargeback reduction to 9.8% for EU-processed adult transactions in 2023 is a headline figure worth sitting with. A US-processed dating business operating at a 13% chargeback rate faces not only higher dispute costs but also the constant risk of breaching processor thresholds (typically 1% for card networks, measured differently from total transaction volume). EU SCA mandates, which require two-factor authentication for card-not-present transactions, have been the primary driver of this improvement.

| Metric | EU-regulated processing | US-regulated processing |

|---|---|---|

| Average adult chargeback rate | ~9.8% | ~12% to 15% |

| Strong customer authentication | Mandatory (SCA) | Optional or inconsistent |

| Typical processing fee (high-risk) | 2.5% to 3.5% | 3.5% to 5.5% |

| Rolling reserve requirement | 5% to 10% | 10% to 20% |

| Account termination risk | Low (specialist EMI) | High |

What non-EU banks consistently get wrong for dating businesses

- They apply generic high-risk policies without understanding the dating sector’s specific risk profile

- They lack knowledge of age-verification compliance requirements under EU law

- They have no established escalation pathways for chargeback disputes in adult verticals

- They cannot support multi-currency SEPA settlement efficiently

- They routinely fail to distinguish between compliant dating platforms and unregulated adult content

Accessing the right EU payment partners for high-risk businesses addresses most of these gaps directly. The combination of regulatory familiarity and sector-specific experience is what separates a banking relationship that lasts from one that collapses under the first audit. Grounding your setup in payment processing best practices for 2026 ensures you’re not just compliant today but resilient for the regulatory changes ahead.

How to choose and secure an EU bank for your dating business

Knowing EU banking is better isn’t enough. You need to execute the process correctly, because a poorly structured application to an EU institution will fail just as quickly as an application to any mainstream bank. Here is a practical sequence that consistently improves outcomes.

- Define your regulatory baseline first. Before approaching any bank, confirm your licensing status. An EU-licensed dating business in a jurisdiction like Malta, Cyprus, or Estonia is dramatically easier to bank than an unlicensed platform. If you’re not yet licensed, prioritise this step before banking outreach.

- Prepare a comprehensive compliance package. This means anti-money laundering (AML) policies, Know Your Customer (KYC) procedures, age-verification documentation, terms of service, privacy policies compliant with GDPR, and corporate structure charts. Banks want to see that your compliance infrastructure is real, not theoretical.

- Target specialist EMIs and payment institutions, not retail banks. Mainstream EU banks (think large national lenders) still reject high-risk applications as standard. Your target list should focus on EMIs and specialist payment institutions with documented experience in adult and dating verticals.

- Prepare transaction history and chargeback reports. If you have existing processing data, present it clearly. Demonstrating that your chargeback rate is already at or below sector benchmarks is a powerful onboarding signal.

- Engage a specialist advisor before submitting applications. Cold applications to EU banking institutions have a high failure rate for dating businesses. An advisor with existing relationships at target institutions can pre-qualify your application and ensure the submission format meets internal expectations.

- Structure your corporate presence strategically. Certain EU jurisdictions offer more favourable environments for dating businesses. Cyprus, Malta, and certain Baltic states have established regulatory frameworks that banking partners recognise and trust.

- Plan for ongoing compliance reviews. Securing the account is step one. Maintaining it requires regular compliance audits, proactive chargeback management, and transparent communication with your banking partner.

Pro Tip: EU institutions value consistency over perfection. A business with a slightly elevated chargeback rate that demonstrates active remediation measures is often more bankable than one with a clean record and no documented compliance programme.

The EU banking solutions available to high-risk firms with the right preparation carry an 87% approval rate through specialist channels. Contrast that with the sub-20% approval rate most dating businesses experience when approaching conventional banks cold. Reviewing specific banking approval tips for high-risk sectors before you begin the process reduces the most common and avoidable rejection triggers.

A2A payment growth in EU markets through 2025 and 2026 also means the cost advantage of EU banking for dating businesses will widen, not narrow, over the next two years.

What most businesses miss when switching to EU banking

Here’s the uncomfortable truth we see repeatedly: dating business owners spend months searching for “any bank that will take us” instead of building the infrastructure that makes premium banking partners want to take them.

The obsession with big-brand names is another consistent mistake. Businesses spend time chasing large EU retail banks because the name feels reassuring, while ignoring specialist EMIs that would onboard them in three weeks with better terms. The brand equity of a banking institution means very little when your account gets flagged and frozen. What matters is sector-specific experience and the institution’s internal risk frameworks for adult and dating verticals.

Compliance is the single most underutilised growth lever in this sector. Most dating business owners treat AML policies and KYC procedures as bureaucratic friction. The businesses that scale successfully treat compliance as a commercial asset. A documented, demonstrably functional compliance programme changes how banking partners price your account, how card networks assess your risk tier, and how regulators view your business during audits. It is genuinely competitive.

The payment innovation gap is equally striking. A2A payments like Wero are growing rapidly across European markets, yet most dating businesses are still running entirely on card rails. The fee savings alone justify exploration, but the more significant benefit is reduced chargeback exposure, because A2A payments don’t carry the same dispute mechanisms as card transactions.

Exploring deeper EU banking benefits reveals that the businesses winning in this space aren’t just “banked.” They’ve built multi-layered payment infrastructure with redundancy, lower cost per transaction, and regulatory relationships that protect them from sudden policy shifts. That’s the actual goal. Not “find a bank.” Build a payment ecosystem.

Payment Processing for Adult and Dating Sites

Top payment solutions for adult sites: providers, features, and comparison

Now that you understand what payment processing is and how it applies to adult sites, let us examine which providers actually deliver and how their features differ.

The leading names in adult payment processing each have a distinct focus. CCBill processes over $1B annually and charges rates from 10.8–14.5% for adult content. Epoch specialises in international billing and multi-currency support. Segpay focuses on recurring billing and compliance tooling. PayBito and MyntPay cater to crypto-native adult businesses. SensaPay targets European merchants seeking higher approval rates through EU-based acquiring.

Here is a direct comparison to help you shortlist:

| Provider | Regions | Recurring billing | Fraud tools | 24/7 support | Chargeback protection |

|---|---|---|---|---|---|

| CCBill | Global | Yes | Advanced | Yes | Yes |

| Epoch | Global | Yes | Moderate | Yes | Yes |

| Segpay | US, EU | Yes | Advanced | Yes | Yes |

| SensaPay | EU | Yes | Moderate | Limited | Yes |

| MyntPay | Global | Crypto only | Basic | Limited | N/A |

When evaluating providers, prioritise 24/7 support, flexible APIs that integrate with your platform, and robust chargeback protection. Approval rates and processing fees matter, but a processor that drops you at the first sign of a spike in disputes is worse than one that charges a slightly higher rate and stands by you.

Common pitfalls to avoid when choosing a processor:

- Signing with a single provider and having no backup

- Ignoring the fine print on rolling reserves and termination clauses

- Choosing based on fee alone without checking regional coverage

- Overlooking whether the processor supports your specific content type (cams, VOD, subscriptions)

- Failing to check real merchant experiences before committing

Pro Tip: Always set up cascading routing across at least two processors. If your primary processor declines a transaction, the secondary picks it up automatically. This alone can increase your overall approval rate by 10–20%.

Your adult site payment processing setup should never rely on a single point of failure. Explore adult bank account options that complement your processing relationships for full financial resilience.

Managing chargebacks, reserves, and payment pitfalls in the adult sector

Beyond compliance, the practical reality of adult payments involves constantly mitigating operational risks like chargebacks and reserves.

A chargeback occurs when a customer disputes a transaction with their bank rather than contacting you directly. The bank reverses the payment, and you lose both the revenue and a chargeback fee. In adult, this happens more frequently than in most other industries, often because customers use a shared card, forget a subscription, or simply want to avoid embarrassment when querying a charge.

Rolling reserves are funds your processor holds back, typically 10–20% of revenue for 90 to 180 days, as a buffer against future chargebacks and refunds. They are standard in high-risk processing and non-negotiable for most adult merchants starting out.

Global chargebacks are projected to hit 261 million in 2025, representing 24% growth through to 2028. Adult e-commerce sees above-average dispute rates of 0.6–1%, and merchants win approximately 45% of representments (formal chargeback disputes). That win rate is meaningful, but prevention is always cheaper than fighting.

“Winning a chargeback representment takes time, documentation, and processor cooperation. The merchants who win most often are those who have built airtight billing descriptor practices and fast customer support response times.”

Strategies to reduce disputes:

- Use clear, recognisable billing descriptors so customers know exactly what they are being charged for

- Offer prompt, no-questions-asked refunds to customers who contact support before disputing

- Deploy fraud screening tools to catch stolen card use before it becomes a chargeback

- Send pre-billing reminders for subscription renewals

- Maintain detailed transaction records for every representment

Account terminations can happen suddenly in this sector. A spike in chargebacks, a card scheme audit, or a change in processor policy can leave you without a payment solution overnight. That is why high-risk payment processing tips consistently emphasise having a backup processor active and ready before you need it. Review international billing considerations if you serve customers across multiple regions, as currency and billing practices vary significantly.

EU Banking for Dating Sites: PSPs, AML Rules and Opening Accounts

What are the key payment service provider types for dating sites in the EU?

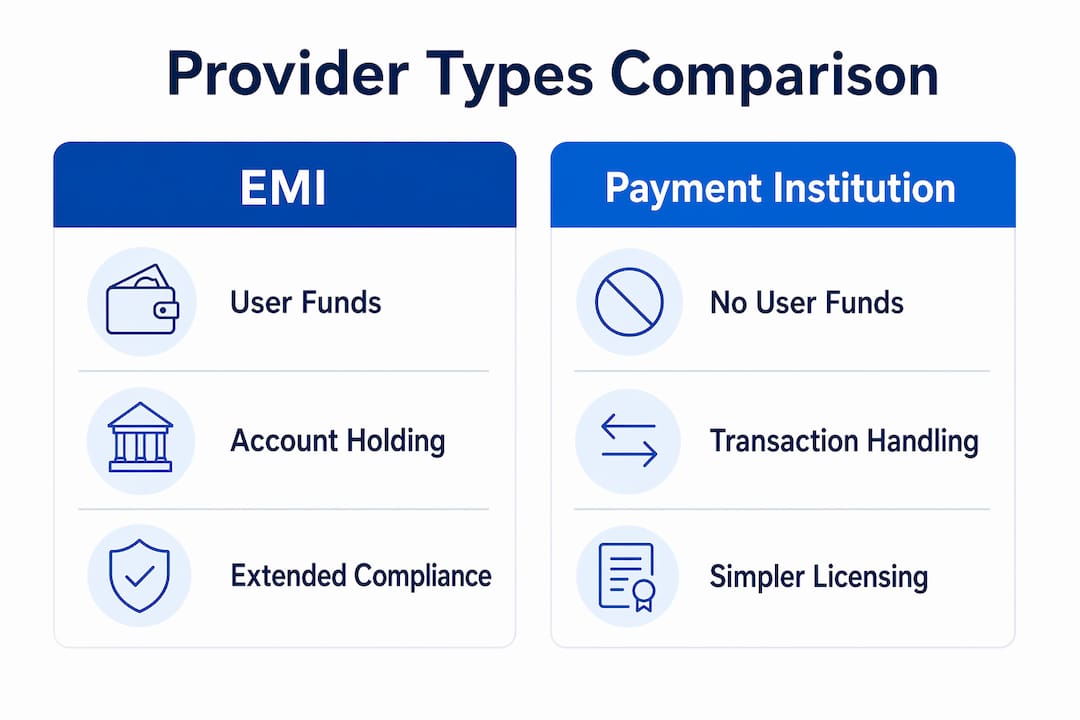

EU payment regulation draws a firm line between two provider categories that dating site operators must understand before approaching any bank or financial institution. Directive 2015/2366 (PSD2) governs both Electronic Money Institutions (EMIs) and Payment Institutions (PIs), but their functions differ in ways that directly affect how your platform handles funds.

A Payment Institution is authorised to execute payment transactions, including credit transfers and direct debits, but cannot hold customer funds beyond the time needed to process a transaction. An Electronic Money Institution, by contrast, can issue electronic money and hold balances on behalf of users. For a dating site operating a wallet or credits system where users pre-load funds, an EMI relationship is the correct structure. For a platform that simply processes subscription charges and passes funds to the operator, a PI arrangement is sufficient.

The distinction between EMIs and PIs under PSD2 directly shapes your compliance obligations. EMIs face stricter capital requirements and more frequent regulatory reporting. Choosing the wrong provider type creates friction during onboarding and can trigger compliance queries that delay account opening by months.

- EMI: Issues e-money, holds user balances, suits credit or wallet-based dating models

- PI: Executes payments only, suits subscription or one-off charge models

- Merchant of Record (MoR): Takes on payment liability, useful for multi-market EU expansion

- Acquiring bank: Processes card transactions directly, requires the highest compliance threshold

Pro Tip: Before approaching any payment partner, map your exact payment flow on paper. Identify whether your platform holds funds at any point, even briefly. That single question determines whether you need an EMI or a PI, and getting it wrong is the most common reason dating sites receive avoidable rejections.

You can find detailed guidance on EMI account options for adult and dating businesses through Bankmycapital’s dedicated resource.

How do EU AML/CFT rules affect dating site banking?

The EU’s anti-money laundering and counter-terrorism financing framework underwent a significant overhaul in 2024. Regulations (EU) 2024/1620 and 2024/1624, alongside Directive 2024/1640, now form the binding legal framework for AML/CFT obligations across all member states. For dating site operators, this matters because your payment partners are directly subject to these rules, and their compliance obligations flow down to you during onboarding.

Customer due diligence (CDD) is the most immediate impact. Every PSP or EMI you approach must verify the identity of beneficial owners, assess the nature of your business, and satisfy themselves that your revenue model does not facilitate money laundering or sanctions evasion. Dating platforms attract scrutiny because anonymous user interactions and cross-border micropayments can, in theory, be misused. Your job is to make that theory implausible through documentation.

Enhanced AML supervision under the new framework means that payment partners face harmonised supervisory methods and stronger CDD controls, which increases the depth of questions you will receive during onboarding. Sanctions screening is now continuous rather than periodic, so your platform must demonstrate that it does not process payments for sanctioned individuals or entities.

The most effective way to satisfy AML/CFT requirements is to present a written compliance programme before you are asked for one. A proactive submission signals that your business is prepared, not reactive, and changes the tone of the entire onboarding conversation.

Key documentation your compliance programme should address:

- Beneficial ownership structure with certified copies of ID for all owners above 25%

- Source of funds explanation for initial capitalisation

- Transaction monitoring policy describing how you detect unusual payment patterns

- Sanctions screening procedure naming the lists you check (OFAC, EU Consolidated List, UN)

- Refund and cancellation policy with clear timelines

Why are dating sites classified as high risk by banks?

MCC 7273 is the merchant category code that banks and card networks assign to dating services, and it carries an elevated risk flag by default. This classification exists because dating platforms historically generate higher chargeback rates than average merchants, driven by recurring billing disputes, forgotten subscriptions, and the occasional fraudulent charge. Card networks use MCC codes to set underwriting thresholds, and MCC 7273 triggers additional scrutiny before any account is approved.

The risk drivers compound each other. Recurring billing creates dispute exposure when users forget they subscribed. The association with adult content, even for platforms that carry none, raises reputational concerns for conservative banking partners. Fraud potential from romance scams means that some transactions are disputed not because of billing errors but because a user was deceived by another user. None of these risks are unique to your specific business, but they are attached to your category by default.

| Risk factor | Impact on banking | Mitigation |

|---|---|---|

| MCC 7273 classification | Elevated underwriting threshold | Legal opinion clarifying business model |

| Recurring billing disputes | Higher chargeback ratio | Clear cancellation policy, dunning retries |

| Adult content association | Reputational concern for banks | Explicit content policy and age verification proof |

| Romance scam fraud | Disputed transactions from deceived users | Fraud filters, user verification, dispute SLA |

| Cross-border payments | Sanctions and AML exposure | Sanctions screening programme |

A legal opinion that resolves classification ambiguity is one of the most effective tools available to dating site operators. In documented cases, a formal legal position focusing on service type, monetisation model, and AML/CFT compliance has shifted a bank’s risk assessment from high to medium or low, unlocking accounts that were previously refused. The opinion does not change your business. It changes how a compliance officer reads your business.

Pro Tip: Prepare a one-page risk narrative that explains your business model in plain language, describes your chargeback rate over the past 12 months, and lists the fraud prevention tools you use. Attach it to every banking application. Most operators never do this, which is precisely why it works.

Understanding how banks classify high-risk merchants and the mechanics behind MCC codes will help you frame your application more precisely.

What practical steps can dating sites take to open EU bank accounts?

Opening a bank account or payment processing arrangement as a dating site in the EU follows a predictable sequence once you know what each stage requires. The process rewards preparation far more than persistence.

- Incorporate in a credible EU jurisdiction. Malta, Cyprus, and the Netherlands are frequently used by dating businesses due to their established regulatory frameworks and banking familiarity with the sector.

- Prepare your document pack. This includes certificate of incorporation, director and beneficial owner ID, a business plan with revenue projections, domain registration proof, and at least six months of payment processing history if available.

- Obtain a legal opinion. Commission a qualified lawyer to produce a written opinion confirming that your platform is a dating service rather than an adult content business, and that your monetisation model complies with applicable law.

- Align with PCI DSS Level 1. Dating payment gateways require PCI DSS Level 1 compliance as a baseline. Confirm your hosting and payment page architecture meets this standard before approaching acquirers.

- Select a PSP or MoR with EU local payment method coverage. Loovedate, a dating platform that expanded across EU markets, used a payments partner with over 400 local payment methods and hosted payment pages to improve authorisation rates across multiple countries.

- Submit applications to pre-vetted partners. Applying to banks that already work with dating businesses avoids the educational overhead of explaining your sector from scratch.

| Document | Purpose | Common gap |

|---|---|---|

| Certificate of incorporation | Confirms legal entity | Outdated or unnotarised copy |

| Director ID and proof of address | Satisfies CDD requirements | Expired documents |

| Legal opinion | Resolves risk classification | Absent entirely |

| Processing history | Demonstrates chargeback control | Not available for new businesses |

| AML/CFT compliance programme | Satisfies PSP onboarding | Generic template rather than tailored policy |

Mismatches between payment processing structure, unclear subscription policies, and the absence of a strong AML framework are the primary obstacles in bank onboarding for dating sites. Addressing all three before submitting your first application reduces the back-and-forth that typically adds weeks to the process.

Unlock EU banking expertise for your dating business

The case for EU banking is clear, but executing the move without specialist guidance wastes time and risks further rejections that damage your banking history. At BankMyCapital, we work specifically with high-risk dating and adult businesses to navigate EU banking applications, licensing, and payment infrastructure. Our network of over 50 pre-vetted banking partners and EMIs includes institutions with proven experience in the dating sector, and our 87% approval rate reflects what structured, well-prepared applications achieve. Whether you’re starting from scratch or rebuilding after a banking termination, explore your options through our high-risk sector banking guide, review the full EU banking approval guide for 2026, or go directly to our dating business bank account options. Onboarding typically completes in two to three weeks.

Recommended

- Top advantages of EU banking for high-risk sectors

- EU Banking Regulations – Securing High-Risk Banking

- Banking solutions for EU high-risk firms: 87% approval

- High-risk banking in the EU: 87% approval guide for 2026

Frequently asked questions

Why are dating enterprises considered high-risk for banks?

Dating companies face high chargebacks, regulatory scrutiny around adult content, and elevated fraud exposure, all of which make banks categorise them as high-risk by default. EU PSD2 has reduced adult chargeback rates to 9.8%, but the classification itself persists without the right banking partner and compliance structure.

Do EU banks really improve approval odds for high-risk businesses?

Specialist EU EMIs and payment institutions offer both regulatory clarity and significantly higher approval rates than traditional US or mainstream banking institutions for high-risk businesses. The key is targeting the right type of EU institution, not EU retail banks broadly.

Is it possible to access lower processing fees with EU-based payment systems?

Yes. A2A payment schemes like Wero are enabling materially lower transaction fees for EU-based high-risk businesses by bypassing traditional card network costs. Specialist providers are necessary to structure access to these rails effectively.

How does EU regulation affect chargeback rates for dating businesses?

PSD2’s strong customer authentication requirements directly reduce fraudulent and disputed transactions. EU adult businesses saw chargebacks drop to 9.8% in 2023, a 22% reduction compared to pre-PSD2 benchmarks and significantly below typical US-processed rates.

What is the biggest mistake dating businesses make with EU banking?

Relying solely on traditional banks rather than specialist EMIs and payment institutions is the most common and costly mistake, because mainstream institutions lack the sector-specific frameworks needed to sustainably serve dating businesses.