TL;DR:

- Most high-risk businesses in Europe mistakenly believe that obtaining a single banking license is straightforward, ignoring the distinct categories with different permissions.

- Choosing the correct license—credit institution, EMI, or PI—depends on actual product functions, fund handling, and regulatory requirements, not prestige.

Most high-risk business owners assume that “getting a banking licence” in Europe is a single, linear process. You apply, you get approved, you bank. But the reality is that the European regulatory landscape contains at least three meaningfully different licence categories, each with its own permissions, obligations, and real-world limitations. Firms operating in crypto, iGaming, or forex frequently hit walls not because they lack credibility, but because they are pursuing the wrong licence type entirely. Under the Single Supervisory Mechanism, the ECB holds responsibility for banking authorisation in the EU, which means the stakes for getting this right are high from day one.

Key Takeaways

| Point | Details |

|---|---|

| Licence type drives permissions | The right banking or payments licence directly determines what financial activities your business can legally offer in the EU. |

| EMI vs PI compliance | EMIs must safeguard client funds more tightly than PIs and face closer regulatory supervision. |

| Match licence to business model | Always align your operational realities—like deposit-taking or e-money issuance—with the correct regulatory licence. |

| Sector licences affect banking | Industries like iGaming often require both sector and financial licences for full compliance and payment access. |

Understanding the main banking licence types

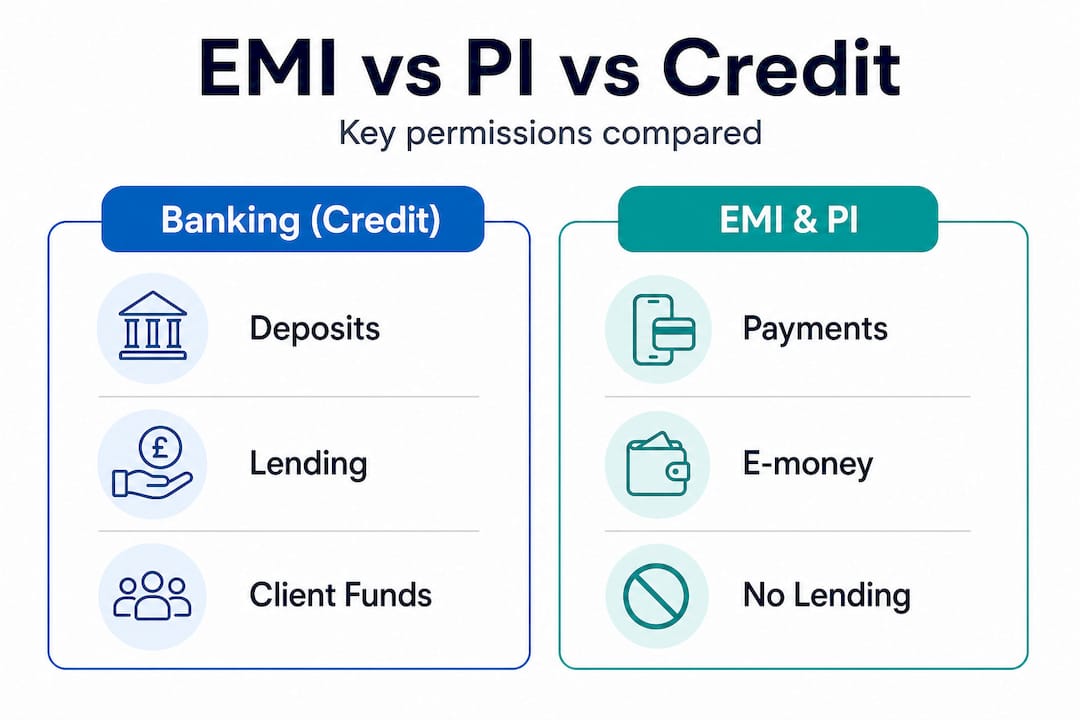

The European financial regulatory framework recognises three primary categories that businesses in high-risk sectors will encounter: credit institutions (full banking licences), Electronic Money Institutions (EMIs), and Payment Institutions (PIs). These are not interchangeable, and conflating them is one of the most expensive mistakes a growing fintech, crypto exchange, or iGaming operator can make.

A full banking licence in the EU is the authorisation to take deposits from the public and grant credit on the institution’s own account. This is the “gold standard” in regulatory terms, but it comes with capital requirements, governance obligations, and supervisory scrutiny that most high-risk businesses simply cannot meet in their early or mid-stage phases. Think of it as being licensed to do everything, but only if you can prove you are stable, well-capitalised, and conservatively managed.

An EMI licence is the far more practical route for businesses that need to issue electronic money and provide payment services without engaging in full deposit-taking or lending. EMIs are permitted to hold customer funds, but strictly as e-money, not deposits in the traditional sense. This distinction matters enormously from a compliance perspective.

A PI licence sits at the narrower end of the spectrum. EU EMI vs PI licensing is commonly distinguished by what you can do with customer value: a PI facilitates payment transactions but does not issue e-money or hold customer balances directly. Think payment gateway rather than wallet provider.

Quick reference matrix: licence types, core permissions, and typical uses

| Licence type | Deposit-taking | Lending | E-money issuance | Payment processing | Typical use case |

|---|---|---|---|---|---|

| Credit institution | Yes | Yes | Yes | Yes | Full retail or commercial bank |

| EMI | No | No | Yes | Yes | Digital wallet, prepaid card, crypto on/off ramp |

| PI | No | No | No | Yes | Payment gateway, merchant services |

This matrix alone should reframe how you think about your compliance strategy. Many firms operating crypto business bank accounts in Europe are actually working with EMIs rather than full banks, which is perfectly valid provided the scope of activities aligns.

Key permissions by licence type:

- Credit institution: Full deposit-taking, consumer and commercial lending, securities services, and payment processing

- EMI: E-money issuance, payment services, account management, international transfers, but no deposit-taking or credit

- PI: Payment execution, money remittance, and merchant services, but no e-money issuance, no balance holding, no lending

Pro Tip: Many fintech and payment providers operate under EMI licences rather than full banking licences. If your business model revolves around payment flows rather than deposit management, an EMI may be more appropriate and far faster to obtain than you might expect.

When considering crypto business banking compliance in 2026, it is worth noting that regulators increasingly assess the substance of what a firm does, not merely the licence it holds. A crypto exchange that holds large client balances in custody-like arrangements may find itself scrutinised at EMI level even if it technically operates under a PI framework.

Key differences: deposit-taking, lending, and holding client value

Here is where it gets genuinely complicated for high-risk operators. The question of who can legally hold customer funds, and under what conditions, is the pivot point around which most compliance frameworks are designed.

Only credit institutions are authorised to take deposits from the general public in the traditional sense. EMIs can hold customer funds, but those funds must be safeguarded, meaning they are ring-fenced from the institution’s own capital, held in segregated accounts or invested in secure, low-risk instruments. This safeguarding requirement is a major compliance edge: EMI and PI licensing models differ fundamentally in how they treat issuance and management of customer balances.

Important: If you are building a product where customer funds sit on your platform for any period of time, you are almost certainly operating in EMI territory at minimum. Treating this as a PI model, or worse, as an unlicensed activity, creates serious regulatory exposure.

Comparison table: deposit, lending, and client value permissions

| Activity | Credit institution | EMI | PI |

|---|---|---|---|

| Accept customer deposits | Yes | No | No |

| Issue loans or credit | Yes | No | No |

| Issue e-money | Yes | Yes | No |

| Hold client funds (safeguarded) | Yes | Yes | No |

| Process payments | Yes | Yes | Yes |

| Custodial asset management | Yes | Limited | No |

For businesses operating in the crypto-friendly banking space, the custody question is particularly acute. Crypto exchanges or wallets that allow users to hold balances on the platform are effectively performing a quasi-deposit function. Whether that triggers EMI obligations, full banking requirements, or separate MiCA-related licensing under the EU’s Markets in Crypto-Assets regulation is something that must be assessed carefully and jurisdiction by jurisdiction.

iGaming operators face similar complexity. Player funds held between deposits and withdrawals must be safeguarded. That obligation often requires a relationship with a licenced EMI or bank, or in some cases obtaining an EMI licence directly. Failing to structure this correctly is one of the primary reasons iGaming firms lose banking relationships abruptly.

Forex brokers are in a comparable position. Client margin deposits, unrealised profits sitting in accounts, and overnight fund holding all create potential obligations that a basic PI licence would not cover. The regulatory bar rises in direct proportion to the degree of client value being held.

Pro Tip: If your business holds customer funds overnight, even briefly, map that cash flow against the EMI safeguarding requirements before your compliance review. Regulators look at the economic reality of your product, not just how it is labelled in your marketing materials.

Choosing the right licence for your business model

The decision should not start with “which licence is easiest to get.” It should start with a clear-eyed mapping of what your business actually does. Here is a practical framework for getting that right.

Step-by-step decision framework:

- Map your cash flow. Where do customer funds sit, for how long, and in what form? If funds are held beyond transaction transit, you are likely in EMI or credit institution territory.

- Define your core product. Are you facilitating payments, storing value, issuing credit, or doing some combination? Each core function aligns with a specific licence category.

- Identify regulatory trigger points. Custody of client assets, e-money issuance, and lending each trigger distinct frameworks. Identify which apply before selecting a licence.

- Assess your jurisdiction. Different EU member states and offshore jurisdictions (Gibraltar, Malta, Cyprus) have varying interpretations of licence requirements and differing approval timelines.

- Pressure-test against sector-specific rules. Crypto firms must also consider MiCA. iGaming licensing adds its own layer on top of payment licensing obligations.

- Build your licensing stack. For many businesses, the answer is not one licence but two or three complementary licences working together.

The most common methodology for mapping product mechanics to the correct regulatory permission in Europe is to work backwards from the user experience: what does the customer experience when they put money in, hold it, and take it out? That end-to-end journey tells you more about your licence requirements than any internal product definition.

Let us look at three concrete sector scenarios:

Crypto exchange: Typically requires at minimum an EMI licence if holding user balances, plus MiCA authorisation from 2025 onwards for crypto-asset services. A PI alone is insufficient unless the exchange operates purely as a pass-through with zero balance holding.

iGaming operator: Requires a gaming operator licence from the relevant gambling regulator plus a banking or payment arrangement that satisfies player fund safeguarding requirements. Many operators also need an understanding of iGaming regulations across multiple territories if they operate cross-border.

Forex brokerage: Regulated typically under MiFID II in the EU as an investment firm. Payment services are ancillary, but client fund segregation rules overlap significantly with EMI safeguarding frameworks. In practice, most forex firms work with licenced EMIs or banks for their client account structure rather than holding their own banking licence.

According to regulatory data reviewed across EU member states, obtaining an EMI licence takes on average 12 to 18 months, while a PI licence can often be achieved in 6 to 9 months. A full credit institution licence routinely takes two to four years and requires minimum capital of €5 million under EU rules.

Pro Tip: Watch for overlap between sectors. If your crypto product also facilitates iGaming payments, or your forex brokerage holds overnight client balances, expect higher regulatory scrutiny. Custodial behaviour and customer value handling are always the harder compliance items, regardless of jurisdiction.

iGaming and the role of non-banking licences

The iGaming sector offers perhaps the clearest illustration of why non-banking licences have direct banking compliance consequences. A gambling operator licence is not a substitute for a payment licence, but its structure directly shapes what banking arrangements are feasible and required.

Gibraltar’s gambling framework, for example, distinguishes between B2C operator licences, B2B supplier licences, and Gambling Operator Support Services (GOSS) licences. GOSS licences cover firms providing marketing, affiliate management, and crucially, customer fund management services. The GOSS category matters enormously in the context of banking compliance because it creates a regulated intermediary layer between player funds and the operating company.

Why this matters for payment and banking compliance:

- Ownership scrutiny: Regulators in Gibraltar, Malta, and Isle of Man all examine beneficial ownership structures above the 25% threshold. Complex multi-entity structures often used in iGaming can trigger additional compliance reviews from both the gambling regulator and the banking partner simultaneously.

- Player fund ring-fencing: Most reputable gambling regulators require operators to demonstrate that player funds are held separately from operating capital. This almost always requires a relationship with either a credit institution or a licenced EMI.

- Payment integration complexity: GOSS-licenced firms providing white-label services often need their own payment arrangements separate from the end-operator. Two separate compliance stacks must coexist without conflict.

- Multi-jurisdictional exposure: Operators holding licences in multiple jurisdictions (Gibraltar, MGA, Curaçao simultaneously) face compounded compliance obligations, and banking partners assess that aggregate risk profile accordingly.

Securing an iGaming bank account that actually works operationally requires understanding not just the gambling licence structure but how it interacts with payment institution and EMI frameworks. Similarly, comparing iGaming licence jurisdictions is only meaningful when you factor in which jurisdictions have established banking relationships with licenced gambling operators.

What most high-risk firms overlook when choosing a banking licence

Here is an uncomfortable truth we encounter regularly: too many high-risk operators treat the pursuit of a full banking licence as a prestige exercise rather than a functional decision. The logic goes something like, “if we have a real bank licence, banks will take us seriously.” But that framing is backwards.

The businesses that achieve stable, long-term banking arrangements in sectors like crypto, iGaming, and forex almost never do so because they hold a credit institution licence. They succeed because they have built clarity around their regulatory posture, structured their licensing stack to match what they actually do, and selected jurisdictions where their model is understood and welcomed.

We have seen firms spend three years and seven figures pursuing a full banking licence in an EU member state, only to discover that their actual product, a crypto custody and staking platform, was better served by an EMI licence and a MiCA authorisation. The irony is that the EMI route would have been faster, cheaper, and more credible to their banking partners.

The real compliance risk almost always sits in the grey zones: who is holding client value, under what conditions, and is that function adequately licenced? Those questions matter far more than the label on your regulatory approval. The essential banking tips for iGaming operators who have successfully maintained banking relationships consistently point to regulatory clarity about fund flows as the decisive factor, not licence prestige.

If you are building a licensing strategy for a high-risk business in 2026, invest in understanding the functional boundaries of each licence type first. Match your actual product mechanics to the right regulatory framework. Then pursue the licence that fits, even if it is smaller, narrower, or less impressive-sounding than you imagined. That discipline is what separates operators who maintain banking relationships from those who lose them.

Connect with expert guidance and licensing solutions

Navigating EMI, PI, and credit institution requirements whilst also managing sector-specific licences is genuinely complex work. At BankMyCapital, we work directly with crypto, iGaming, and forex businesses to identify the right licensing stack, match them with pre-vetted banking and EMI partners, and manage the compliance process from initial assessment through to approval. Whether you need payment processing infrastructure, tailored crypto banking solutions for your exchange or custody platform, or specialist guidance on licensing services across EU and offshore jurisdictions, our team brings direct experience with the exact regulatory terrain this article covers. Speak to us before you commit to a licensing route.

Frequently asked questions

What is the difference between a banking (credit institution) licence and an EMI in the EU?

A banking licence allows full deposit-taking and lending, while an EMI licence permits electronic money issuance and payment services but does not grant deposit-taking or credit rights.

Can high-risk businesses like crypto or iGaming firms get a full banking licence in the EU?

It is rare and often impractical, as ECB banking authorisation requirements are strict and typically mismatched to high-risk business models. EMI or PI licences are more realistic and operationally appropriate for most of these firms.

How do compliance obligations differ between EMI and PI licences?

EMIs face stricter requirements around safeguarding customer balances and fund segregation compared to PIs, which do not issue e-money or hold client balances at all.

Why are non-banking licences like GOSS relevant for iGaming?

GOSS and similar non-banking licences cover support functions including customer fund management, which directly governs how iGaming compliance interacts with payment and banking arrangements in jurisdictions like Gibraltar.