TL;DR:

- Forty percent of European businesses use cryptocurrency, but only 41% of financial institutions offer crypto banking services. Regulatory and risk concerns cause most banks to reject crypto firms, with private banks being the most crypto-friendly. Proper regulatory licensing, documentation, and relationship-building are key to opening a crypto business bank account in Europe.

Forty per cent of European businesses now hold or use cryptocurrency, yet only 41% of financial institutions actively offer banking services to crypto firms. That gap tells you everything about the frustration crypto entrepreneurs face every day. You have a legitimate, growing business. You have clients, revenue, and regulatory intent. But opening a simple business bank account feels like trying to get a mortgage with an invisible credit history. This guide maps out exactly what’s happening in the European crypto banking landscape, why the barriers exist, and precisely what you need to do to get past them.

Key Takeaways

| Point | Details |

|---|---|

| Banking gap persists | Most financial institutions are not crypto-friendly, despite rising business adoption in Europe. |

| Regulation shapes choices | MiCA and licensing requirements strongly impact which banking options are open to crypto firms. |

| Private banks offer advantages | Private banks approve crypto accounts more often but demand stringent compliance documentation. |

| Preparedness is crucial | Clear, up-to-date compliance and licensing documentation make or break your account application. |

Understanding the crypto banking landscape in Europe

The numbers are striking. Europe leads global crypto adoption among businesses, yet the majority of its financial institutions still refuse to engage with the sector. This is not an accident. Banks operate under strict regulatory oversight and have historically treated crypto as a reputational and compliance liability. Most large retail and commercial banks still view onboarding a crypto business as a risk that is simply not worth taking, regardless of how well-structured your operation might be.

“The banking access gap for crypto firms is not a temporary inconvenience. It reflects deep structural caution within financial institutions that have spent years absorbing mixed regulatory signals from national and EU-level authorities.”

The situation is shifting, but slowly. MiCA, which came into full force in December 2024, requires any firm providing crypto asset services in the EU to obtain a CASP (Crypto Asset Service Provider) licence. This brings a standardised regulatory framework that banks can actually work with. Firms that previously operated as VASPs (Virtual Asset Service Providers) under national regimes have until July 2026 to obtain full MiCA authorisation or cease operating. The good news is that this transitional window gives existing businesses room to manoeuvre while they pursue compliance.

So what does the landscape look like in practical terms? Consider this breakdown:

- Large commercial banks: Only around 10% offer services to crypto businesses. Strict risk policies, lengthy compliance reviews, and internal committees that default to rejection make these institutions the most difficult entry point.

- Private banks: Remarkably, private banks show 100% engagement with crypto clients in recent benchmarking data. They have dedicated compliance teams familiar with the sector and the appetite for high-value clients.

- Challenger banks and neo-banks: Variable. Some are very open, others have quietly implemented restrictions that mirror their traditional counterparts.

- Electronic Money Institutions (EMIs): Growing rapidly as a practical alternative, particularly for startups and scale-ups.

Understanding crypto licensing requirements before approaching any banking provider is essential. Banks want to see that you have thought through your regulatory position before you arrive at their door. Keeping pace with crypto banking trends in 2026 will also help you present your business as forward-looking and compliant, not reactive.

Comparing banking options for crypto businesses

Now that the regulatory context is clear, let’s look at the types of banking solutions available and how they compare across the dimensions that matter most to a crypto firm: accessibility, compliance demands, and practical usability.

| Banking type | Crypto approval rate | Typical onboarding time | Key strength | Key risk |

|---|---|---|---|---|

| Large commercial bank | Very low (approx. 10%) | 3 to 6 months | Brand trust, broad services | High rejection risk |

| Private bank | Very high (approx. 100%) | 4 to 8 weeks | Specialist knowledge | Minimum asset requirements |

| Challenger/neo-bank | Moderate | 1 to 3 weeks | Speed, digital-first | Service limitations |

| EMI | High | 1 to 2 weeks | Accessible, fast | Limited banking functions |

As benchmarking data confirms, the contrast between private banks and large commercial banks is stark. If you have the assets and the business profile, a private bank is your strongest banking option. If you are an early-stage company, an EMI is a far more practical starting point.

Here is a ranked approach to selecting your banking option:

- Clarify your business model first. Are you an exchange, a custody provider, or a payment processor? Each type carries different risk profiles for banks and requires different licences under MiCA.

- Check your asset base. Private banks typically require minimum balances or turnover thresholds. If you meet them, prioritise this route.

- Research jurisdiction-specific options. Estonia, Lithuania, and Malta have developed regulatory ecosystems that attract crypto-friendly banks and EMIs.

- Build a shortlist of 5 to 8 providers. Do not apply to all at once. A wave of rejections creates a record that makes subsequent applications harder.

- Prepare your documentation package before any outreach. Banks want to see your licence status, AML policy, UBO (Ultimate Beneficial Owner) declarations, and business plan from the first conversation.

Understanding what crypto-friendly banking actually means in practice can save you months of misdirected effort. And if you are considering the EMI route, a detailed look at EMI accounts for crypto startups will help you assess whether the trade-offs work for your operational needs.

Pro Tip: Private banks have dramatically higher approval rates for crypto businesses, but they select clients carefully. If you approach a private bank, frame your pitch around long-term relationship value, not just an account opening request. Show them your growth trajectory, your compliance infrastructure, and your plans for the next two to three years.

Navigating regulatory and compliance requirements

After weighing your banking options, let’s focus on the compliance steps that will define whether any bank or EMI actually says yes to your application.

The core regulation you must understand is MiCA. Since MiCA came into full force in December 2024, all firms providing crypto asset services in the EU need a CASP licence, unless they qualify for the VASP transitional relief running until July 2026. Getting this licence is not just a regulatory formality. It is the single most important thing you can do to improve your banking prospects, because it signals to every financial institution that your business has passed regulatory scrutiny.

Here is what banks and regulators typically require before they will engage with a crypto business:

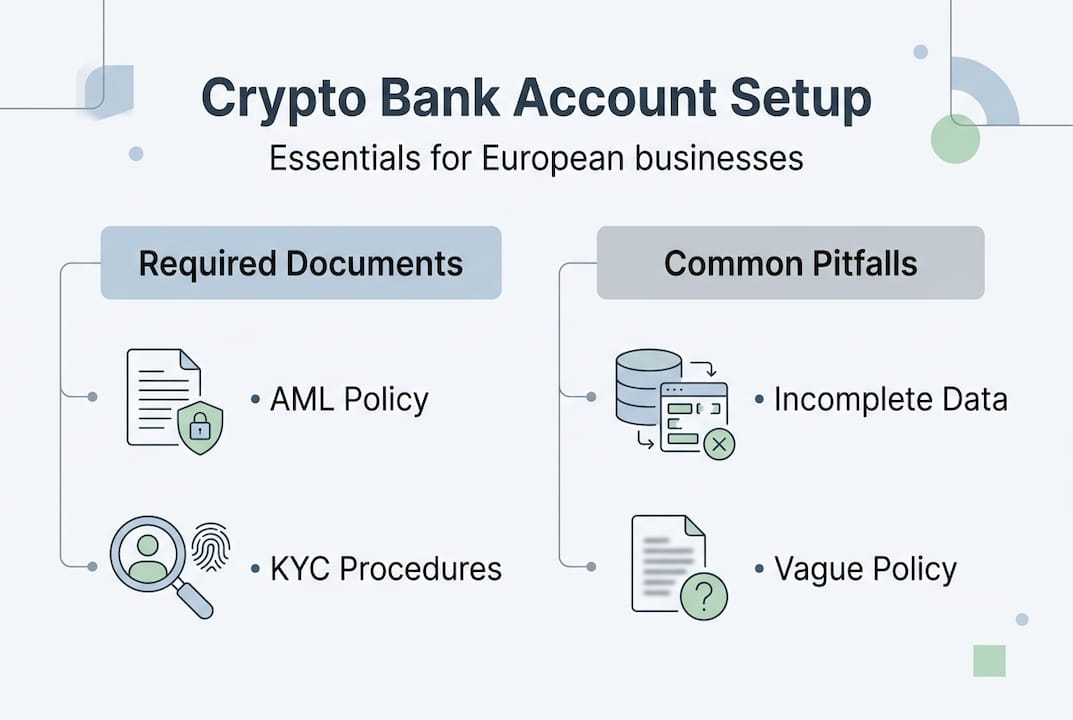

- CASP or VASP licence documentation: The actual licence or proof of application, including correspondence from the relevant national competent authority.

- AML/CFT policy: A written, up-to-date policy covering anti-money laundering and counter-terrorism financing procedures specific to crypto operations.

- KYC framework: Your onboarding procedures for clients, including how you conduct due diligence on individual and corporate clients.

- UBO declaration: Full beneficial ownership structure, with supporting documentation for each UBO holding 25% or more.

- Source of funds documentation: Evidence that business capital originates from legitimate, traceable sources.

- Business plan and financial projections: Banks want to understand your revenue model and anticipated transaction volumes.

| Compliance document | Purpose | Common shortfalls |

|---|---|---|

| AML/CFT policy | Demonstrates regulatory readiness | Out of date or too generic |

| KYC framework | Shows client due diligence rigour | Missing crypto-specific procedures |

| UBO structure | Identifies who controls the business | Complex structures without explanation |

| Source of funds | Confirms capital legitimacy | Insufficient trail documentation |

| CASP/VASP licence | Proves regulatory authorisation | Missing or in application only |

Working through a thorough crypto compliance checklist before you contact any bank will save you significant time and dramatically improve your chances. It is also worth understanding the specifics of CASP and VASP licensing in your target jurisdiction, as requirements vary between member states during the transitional period.

Pro Tip: Banks rarely tell you exactly why they rejected your application. Preparing clear, logically structured documentation from the outset removes ambiguity and accelerates the review process. Compliance officers appreciate when a business has pre-empted their standard questions.

Practical steps for opening a crypto business account

Having covered what you need for compliance, here is the step-by-step process for turning your preparation into an actual open business account.

- Define your banking requirements. Before approaching any provider, be precise about what you need. Multi-currency accounts? SEPA and SWIFT transfers? Crypto-to-fiat conversion? The clearer you are, the better you can match your needs to a specific provider’s offerings.

- Obtain or confirm your regulatory status. If you are within the VASP transitional window, document this formally. If you are applying for a CASP licence, obtain a written acknowledgement of receipt from the relevant authority. Do not approach banks without some form of regulatory standing.

- Build your documentation pack. Use the compliance document table above as your baseline. Every document should be current, accurate, and organised. Inconsistencies between documents are one of the most common reasons for rejection.

- Identify your shortlist of banking providers. Prioritise providers known to work with crypto businesses in your target jurisdiction. Use specialist consultancy networks if necessary to identify who is actually open to your sector right now, not who was open two years ago.

- Submit a pre-application inquiry where possible. Some banks and all EMIs allow you to have an initial conversation before a formal application. Use this to test their current appetite for crypto clients and to identify any deal-breaking requirements early.

- Submit your formal application with a concise cover document. This one-page summary should explain your business model, your regulatory status, your projected transaction volumes, and why you are approaching this particular institution. Keep it factual and professional.

- Respond to due diligence requests promptly. Delays in responding to compliance queries are frequently misread as evasion. Set up a dedicated process for responding within 24 to 48 hours.

Essential documents to have ready before you submit:

- Certificate of incorporation and company constitution

- Shareholder register and UBO declaration

- Directors’ identification documents and proof of address

- CASP or VASP licence or application confirmation

- AML/CFT policy and KYC procedures manual

- Last two years of audited accounts (or projections for startups)

- Bank reference letters if available

Understanding the nuances of opening a high-risk bank account in Europe will prepare you for the specific hurdles that crypto firms face beyond standard corporate onboarding. For a focused walkthrough of the account opening process, the guide on crypto corporate account opening covers jurisdiction-specific considerations in detail.

Pro Tip: Banks are not just assessing your documents. They are assessing your readiness and reliability as a long-term client. When you demonstrate that you understand their compliance concerns before they have to explain them, you significantly shift the conversation in your favour.

Why most crypto entrepreneurs misunderstand the European banking process

Here is what most founders get wrong, and it is not what you might expect. The common assumption is that getting a banking licence or regulatory approval is the hard part, and that everything else follows naturally. It does not.

Regulatory approval and practical bank onboarding are entirely separate processes. A CASP licence tells a bank that you are permitted to operate. It does not tell them that you are a client they want. Banks make commercial decisions, and they apply their own internal risk scoring to every applicant regardless of regulatory status.

The gulf between financial institutions serving crypto firms is not explained by regulation alone. It reflects relationship capital, or the lack of it. Banks are far more likely to onboard a crypto business that comes via a trusted intermediary or referral network than one that arrives cold through a website form.

Most founders treat banking as a transaction: apply, get approved, move on. The businesses that consistently succeed treat it as a relationship. They engage banking partners early, they communicate proactively, and they think about what ongoing value they bring to that institution. That mindset shift, more than any single document, separates the businesses that get banked from those that keep hitting walls.

For a grounded view of what actually works in practice, the high-risk EU banking case studies from businesses that have navigated this process are worth studying carefully.

Connect with proven solutions for crypto business banking

If you are ready to take the next step, BankMyCapital’s network of over 50 pre-vetted banks and EMIs gives your crypto business a direct path past the rejection barriers that stop most applicants cold. Our 87% approval rate is built on thorough preparation, not guesswork. Start with our banking rejection risks guide to identify where your current application might be vulnerable. Then work through the crypto compliance checklist to make sure your documentation is watertight. When you are ready to move, the high-risk banking checklist will guide you through each stage of the onboarding process with precision.

Frequently asked questions

Which European countries are best for opening a crypto business bank account?

Estonia, Malta, and Lithuania offer the most developed regulatory frameworks for crypto businesses, with higher bank and EMI acceptance rates than most other EU member states.

What are the required licences for crypto firms to get a bank account in Europe?

Your firm generally needs a CASP licence under MiCA, or proof of VASP status under the transitional measures that allow prior VASPs to operate until July 2026 pending authorisation.

Why do so many crypto companies get rejected by banks?

Banks cite AML and KYC compliance concerns as their primary reason for rejecting crypto clients, and as only 41% of financial institutions currently serve the sector, most default to rejection unless documentation is exceptionally well prepared.

Can I use an EMI instead of a traditional bank for my crypto business account?

Yes, EMIs are a viable and often faster alternative to traditional banks, though they may carry restrictions on payment rails, transaction limits, or credit facilities that a full banking licence would provide.