TL;DR:

- Forex payment processing involves complex regulatory, fraud, and banking relationships due to high risk.

- Effective controls like fraud filters, velocity checks, and ongoing compliance are essential for risk management.

- Choosing sector-specific payment partners with proven approval rates ensures operational stability and regulatory compliance.

Most forex firms assume payment processing is simply a matter of moving client funds in and out. It is not. Behind every deposit and withdrawal sits a web of regulatory obligations, fraud exposure, and banking relationships that can make or break your operation. Processors and banks classify forex as one of the most demanding sectors to service, and for good reason. Chargebacks, money laundering risks, and cross-border compliance requirements create a pressure that standard ecommerce firms rarely encounter. This guide covers how payment processing actually works for forex, the risks you need to manage, the controls that protect you, and how to choose the right partners.

Key Takeaways

| Point | Details |

|---|---|

| High-risk industry | Forex payment processing faces unique risks from chargebacks, fraud, and regulatory scrutiny. |

| Compliance is crucial | Regulatory controls and anti-fraud systems are essential to maintain banking access. |

| Careful partner choice | Selecting the right payment partner and banking strategy defines operational success. |

| Integrated solutions win | Successful firms use holistic strategies uniting payments, compliance, and banking. |

Understanding payment processing in the forex industry

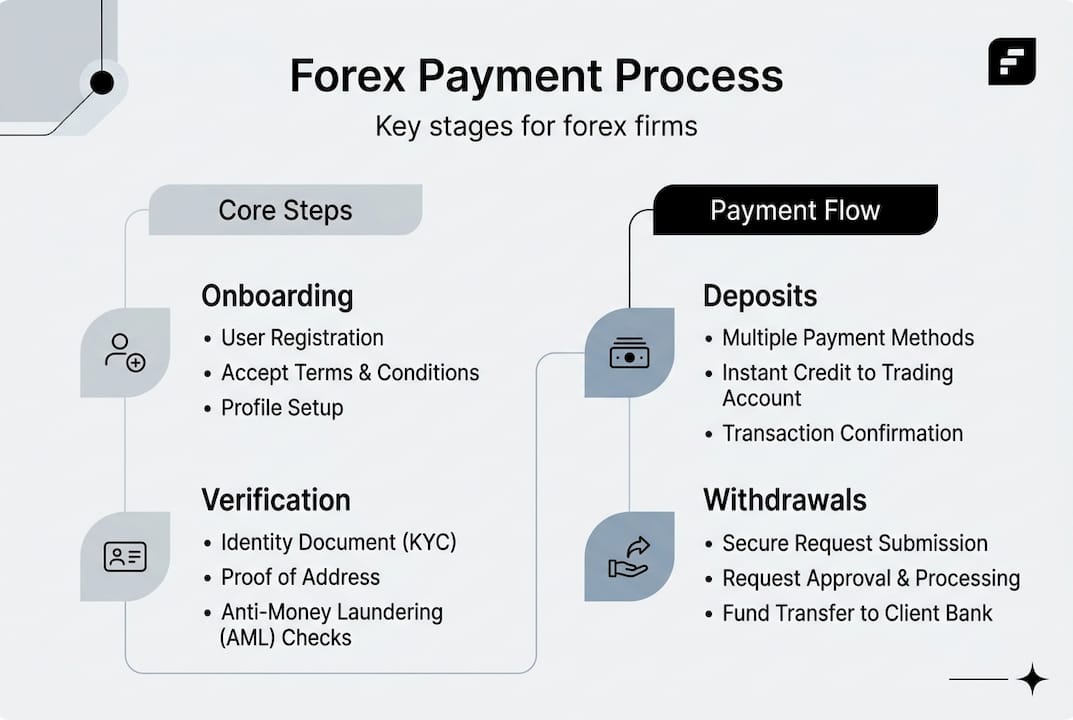

Payment processing in forex is not a single function. It is an interconnected set of operations covering client onboarding, fund collection, transaction monitoring, settlement, and regulatory reporting. Unlike a retail merchant processing card payments for physical goods, a forex broker is handling leveraged financial products with clients across multiple jurisdictions, currencies, and regulatory regimes. The stakes are fundamentally different.

At its core, payment processing basics for forex involves four key stages. First, client onboarding: verifying identity, checking sanctions lists, and approving funding methods. Second, transaction processing: accepting deposits via cards, bank transfers, or e-wallets and routing them correctly. Third, ongoing monitoring: screening transactions in real time for suspicious patterns. Fourth, settlement and reporting: reconciling positions, disbursing withdrawals, and producing audit-ready records for regulators.

Why do banks and processors treat forex differently? Because forex is high-risk due to high chargeback rates, fraud, bonus abuse, and money laundering exposure. These are not theoretical concerns. They are documented patterns that processors have absorbed losses from repeatedly. The result is that many mainstream acquiring banks simply refuse forex clients outright, pushing firms towards specialist high-risk processors.

Understanding forex account management terms is also part of the picture. Concepts like margin calls, rollover fees, and leverage ratios all affect how funds move and when, which in turn affects how processors assess and manage risk on your account.

Several technical controls sit at the foundation of any forex payment setup:

- Fraud filters: Automated rules that flag or block suspicious transactions before they are processed.

- Velocity checks: Limits on how many transactions a single account can initiate within a given timeframe.

- Blacklists: Databases of known fraudulent card numbers, IPs, and client identities shared across processors.

- 3D Secure authentication: An additional layer of card verification that shifts liability away from the merchant.

- Geolocation screening: Blocking transactions from restricted jurisdictions in real time.

Pro Tip: When evaluating a new payment processor, ask specifically how their fraud filters are configured for forex. Generic ecommerce filters will miss forex-specific patterns like bonus abuse cycles and rapid deposit-withdrawal sequences.

Risks and operational challenges in forex payment processing

Once you understand what payment processing involves in forex, it is crucial to grasp why it carries such a high risk for both firms and their banking partners.

Chargebacks are the most visible problem. Global chargebacks reached 287 million transactions costing $25 billion in 2023, and forex sits structurally above the 1% chargeback threshold that processors use to flag high-risk accounts. For context, the global average chargeback rate was 0.92% in 2023, with the US at 0.84% in Q4. Forex brokers routinely exceed this, which triggers penalty fees, reserve requirements, and in serious cases, account termination.

| Sector | Typical chargeback rate | Risk classification |

|---|---|---|

| Retail ecommerce | 0.5 to 0.8% | Standard |

| Travel and ticketing | 0.9 to 1.2% | Elevated |

| Forex trading | 1.2 to 2.5%+ | High risk |

| iGaming | 1.5 to 3.0% | High risk |

| Crypto exchanges | 1.0 to 2.0% | High risk |

Beyond chargebacks, forex firms face three distinct fraud patterns. Bonus abuse occurs when clients exploit promotional offers, deposit funds to claim bonuses, then withdraw before trading. Friendly fraud happens when legitimate clients dispute transactions after losing trades, claiming unauthorised activity. Money laundering is a structural concern because forex accounts can be used to layer illicit funds through a series of trades and withdrawals.

Operational disruption is often underestimated. Account freezes, compliance reviews, and delayed settlements can lock up client funds for days or weeks, damaging trust and triggering regulatory complaints.

Delayed settlements are a particular pain point. High-risk processors often hold rolling reserves, typically 5 to 10% of monthly volume, for 90 to 180 days as a buffer against chargebacks. This ties up working capital and complicates your liquidity management. Reviewing risk management in forex trading strategies can help firms model the impact of reserve requirements on their cash flow before signing processor agreements.

Pro Tip: Before signing with any processor, calculate the worst-case impact of a 10% rolling reserve held for 180 days on your monthly volume. If that number would strain operations, negotiate the reserve terms or seek a processor with a shorter hold period backed by best practices for high-risk payment processing.

Firms that ignore these operational risks often find themselves scrambling for solutions for high-risk payment processing after their first account is frozen, rather than before.

Key anti-fraud systems and compliance controls

Knowing the risks, the next challenge is putting robust anti-fraud and regulatory systems in place.

The baseline technical requirements for any forex payment operation in 2026 are not optional. Regulators and processors alike expect them. Fraud filters, velocity checks, and blacklists are the minimum standard, not a competitive advantage. Building beyond the minimum is where firms differentiate themselves and reduce their risk profile.

Here is a practical sequence for implementing anti-fraud controls:

- Deploy real-time transaction screening integrated directly with your payment gateway, not as a separate manual review step.

- Configure velocity rules specific to forex behaviour, such as flagging accounts that deposit and withdraw within 24 hours without placing trades.

- Implement KYC at onboarding with document verification, liveness checks, and sanctions screening against current watchlists.

- Run ongoing AML monitoring using transaction pattern analysis to detect structuring, layering, and placement activity.

- Maintain and update blacklists regularly, incorporating data from your processor, your own incident history, and industry-shared databases.

- Conduct periodic compliance audits to ensure your controls remain aligned with evolving regulatory requirements across your operating jurisdictions.

Common compliance pitfalls that forex firms fall into include:

- Treating KYC as a one-time onboarding step rather than an ongoing obligation.

- Using generic AML software not calibrated for forex transaction patterns.

- Failing to document the rationale for accepting or rejecting high-risk clients.

- Neglecting to update sanctions screening lists in real time.

For firms handling crypto deposits alongside fiat, crypto payment processing for high-risk operations requires an additional layer of blockchain analytics to trace fund origins. Identifying forex scam and fraud prevention methods also helps compliance teams recognise patterns before they escalate into regulatory incidents.

Pro Tip: Integrating your compliance tools directly into your payment workflow, rather than running them as parallel processes, reduces both chargebacks and regulatory scrutiny. When screening happens before authorisation rather than after, you stop problems at the gate. Reviewing top payment partners for high-risk sectors can help you identify processors with built-in compliance integration.

Choosing payment partners and adapting to banking expectations

With systems in place, the next decision is choosing partners who support both compliance and operational goals.

Not all payment processors are equipped to handle forex. Many that claim high-risk experience have limited exposure to the specific patterns and regulatory demands of currency trading. When evaluating partners, the criteria that matter most are sector-specific approval rates, integration depth with trading platforms, and demonstrated compliance experience with regulators in your target jurisdictions.

Global chargeback costs reached $25 billion in 2023, rising 12% year on year, and client acquisition costs in forex range from $500 to $1,500 per client. These numbers mean that a single poorly managed chargeback wave or a processor relationship that collapses mid-operation can cost far more than the fees saved by choosing a cheaper provider.

| Factor | Forex | iGaming | Crypto |

|---|---|---|---|

| Avg. chargeback rate | 1.2 to 2.5%+ | 1.5 to 3.0% | 1.0 to 2.0% |

| Regulatory complexity | Very high | High | Very high |

| Banking availability | Limited | Limited | Very limited |

| Reserve requirements | 5 to 10% | 5 to 15% | 10 to 20% |

| Typical onboarding time | 4 to 8 weeks | 3 to 6 weeks | 6 to 12 weeks |

When assessing potential partners, ask these questions:

- What is your approval rate specifically for regulated forex brokers?

- How do you handle chargeback disputes and what support do you provide?

- What reserve structure applies to our volume and risk profile?

- Which jurisdictions are you licenced to operate in?

- How do you integrate with MT4, MT5, or cTrader environments?

Understanding mitigation strategies for forex risk also shapes how you present your operation to potential banking partners. Banks assess forex firms on operational transparency, compliance maturity, and chargeback history. Firms that can demonstrate structured approval for high-risk processing and a clear understanding of banking rejection risks are far more likely to secure and maintain stable banking relationships.

Why most forex payment processing advice is too narrow

Most guides on this topic treat payment processing and banking as separate problems to solve independently. In practice, they are the same problem viewed from two angles.

A forex firm’s chargeback rate directly affects its banking relationships. Its KYC quality directly affects its processor approval odds. Its jurisdiction choice directly affects which banking partners will engage at all. Treating these as isolated decisions is how firms end up with a compliant payment setup that no bank will support, or a banking relationship that collapses the moment their chargeback rate spikes.

What we consistently see is that firms succeeding in 2026 are not simply buying better fraud tools. They are building a compliance narrative that runs from client onboarding through to settlement reporting, and presenting that narrative coherently to both processors and banking partners. Following payment processing best practices is the starting point, but the firms that thrive go further by treating data transparency as a competitive asset rather than a regulatory burden. The uncomfortable truth is that most rejections are preventable, and most of them happen because firms apply technical solutions to what is fundamentally a relationship and trust problem.

Streamline your forex operations with the right partners

If you are ready to put these insights into action, practical help is just a click away.

At BankMyCapital, we work specifically with forex firms and brokers who need more than generic payment processing advice. Our network of over 50 pre-vetted banking partners and EMIs means we can match your operation to institutions that understand your risk profile and are ready to engage. With an 87% approval rate and onboarding timelines of two to three weeks, we help firms move from banking rejection to stable, compliant operations quickly. Start with our business banking checklist, understand your banking rejection risks, and explore our tailored forex payment solutions to take the next step.

Frequently asked questions

Why is forex payment processing considered high-risk?

Forex firms face high chargeback rates, fraud, and complex regulations, making them unattractive to traditional banks and standard payment processors. This pushes brokers towards specialist high-risk acquiring solutions.

What anti-fraud measures should forex brokers use?

The essential toolkit includes fraud filters, velocity checks, and blacklists, combined with robust KYC procedures and real-time transaction monitoring to catch suspicious activity before it becomes a chargeback or regulatory issue.

How do chargebacks impact forex brokers?

Global chargebacks cost $25 billion in 2023, and for forex brokers specifically, elevated chargeback rates trigger penalty fees, rolling reserves, and can lead to account closures that disrupt client fund access entirely.

What should forex firms look for in a payment processing partner?

Prioritise partners with documented experience in forex specifically, strong built-in compliance tools, transparent reserve structures, and proven approval rates for high-risk sector clients rather than generic high-risk processors.

Recommended

- Payment processing solutions for high-risk industries 2026

- Crypto payment processing explained for high-risk firms

- Payment processing best practices for high-risk businesses 2026

- High-risk payment processing: 87% approval guide for 2026

- FX Trading Discipline Process: 5 Steps to Funding Success – DayProp Funding

- Master forex trading terms for efficient account management