TL;DR:

- EU PSD2 has significantly reduced chargebacks for adult and dating businesses.

- Specialist EU EMIs and payment providers offer higher approval rates and operational benefits.

- Building a structured payment ecosystem with compliance and new payment tech is key to scaling.

Payment rejections, frozen accounts, and chargeback spirals are the everyday reality for dating business owners who rely on US-centric or offshore-only banking. What most owners don’t realise is that the EU’s regulatory architecture, specifically the Payment Services Directive 2 (PSD2), has measurably shifted the landscape in their favour: adult chargebacks dropped 22% to just 9.8% across EU-regulated processors in 2023, compared to significantly higher rates in the US. This guide breaks down exactly why EU banking works for high-risk dating firms, what it costs you to ignore it, and how to make the move strategically.

Key Takeaways

| Point | Details |

|---|---|

| Lower chargebacks | EU regulations like PSD2 have dramatically reduced chargeback rates for dating businesses. |

| Reduced banking rejection | Specialist EU banks and fintechs enhance approval odds for high-risk companies. |

| Competitive processing fees | Modern EU payment rails such as Wero often yield lower fees than non-EU alternatives. |

| Strategic compliance support | Proactive compliance in the EU is a growth tool, not just risk management. |

| Expert partner advantage | Engaging EU specialists, not just mainstream banks, is key for sustainable dating business growth. |

Understanding high-risk status in dating businesses

Before you can solve a problem, you need to understand why it exists. Banks classify businesses as “high-risk” based on a cluster of factors that signal elevated financial exposure for the institution. Dating platforms tick almost every box on that list.

The main triggers for a high-risk classification include:

- High chargeback rates from subscription billing disputes and fraudulent transactions

- Adult or age-restricted content, which raises regulatory and reputational concerns

- Global customer bases with currency conversion risk and cross-border compliance complexity

- Subscription-based recurring billing, which generates more disputes than one-off purchases

- Fraud vulnerability, particularly synthetic identity fraud and card testing attacks

The practical consequences are severe. Expect higher processing fees (sometimes 3.5% to 5% per transaction), frequent requests for rolling reserves (often 10% to 15% of monthly volume held for 90 to 180 days), and outright rejection from mainstream processors like Stripe or PayPal. Even when you do get onboarded, the relationship can end abruptly if your chargeback ratio creeps above 1%.

“The EU’s PSD2 framework has been a turning point for adult and dating businesses. EU PSD2 reduced chargebacks by 22% to 9.8% in 2023, versus materially higher rates seen across US-processed transactions.”

This is where EU banking fundamentally diverges from alternatives. Rather than treating dating businesses as a liability to be managed, specialist EU institutions and Electronic Money Institutions (EMIs) have built structured onboarding pathways. Options like EMI bank accounts for dating businesses offer purpose-built frameworks that account for the sector’s specific risk profile. Similarly, pursuing proper licensing for dating businesses in EU jurisdictions dramatically improves your credibility with banking partners.

The distinction matters enormously. A dating platform with an EU licence and an EU-regulated banking partner isn’t just “accepted.” It’s operating within a system designed to handle its complexity.

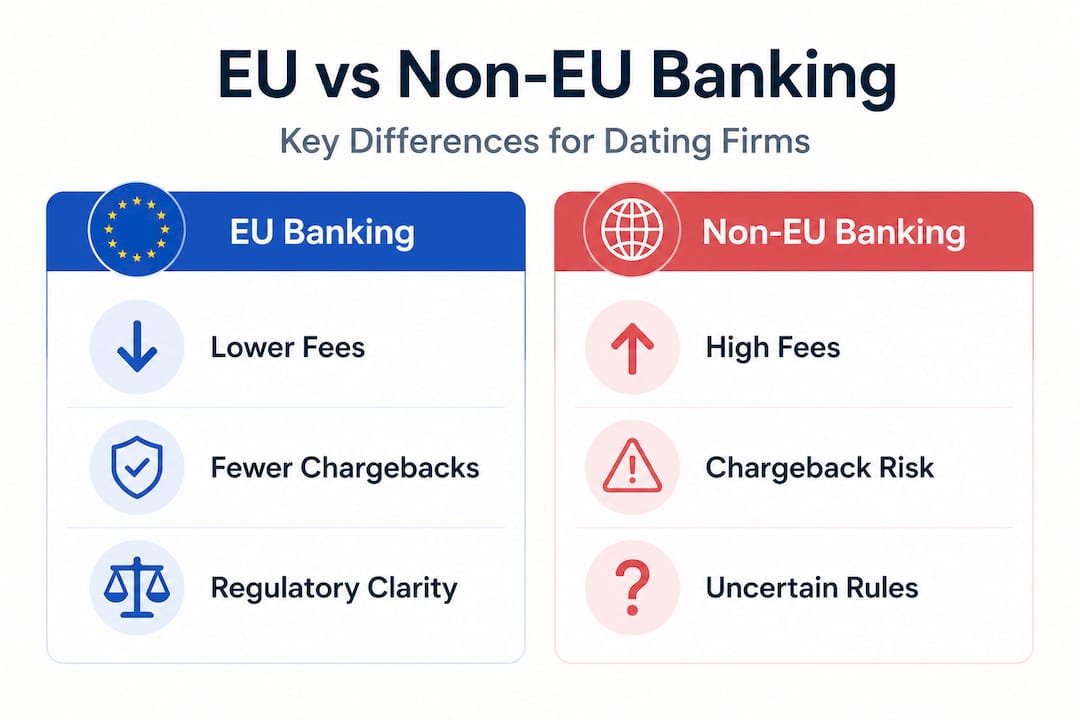

Key advantages of EU banking for high-risk dating firms

The EU banking ecosystem offers dating businesses a set of structural advantages that genuinely cannot be replicated by banking in the US, UK post-Brexit, or typical offshore centres. These aren’t marketing claims. They’re measurable operational benefits.

Pan-European payment rails and lower transaction fees

EU-based businesses gain access to the Single Euro Payments Area (SEPA), which covers 36 countries and enables low-cost, fast bank transfers. More importantly, the rise of account-to-account (A2A) payment schemes, particularly Wero, is reshaping cost structures for high-risk merchants. EU A2A like Wero reduces dependence on US card network dominance and can materially lower transaction costs compared to Visa and Mastercard rails. For a dating platform processing €500,000 per month, even a 0.5% saving in fees translates to €2,500 monthly directly back into your operation.

Regulatory clarity through PSD2 and its successors

PSD2 created a standardised framework for payment disputes, strong customer authentication (SCA), and processor accountability. This clarity benefits dating businesses because the rules are known, enforced consistently, and reduce the arbitrary account terminations that plague US-processed merchants. PSD3, currently progressing through EU legislative channels, is expected to tighten fraud liability further in ways that favour compliant, well-structured merchants.

Diversification away from US-centric risk

Over-reliance on US processors creates a single point of failure. US regulatory shifts, card network policy changes, and banking partner decisions can eliminate your payment infrastructure overnight. EU banking provides genuine geographic and regulatory diversification.

Pro Tip: Pairing with an EU specialist provider rather than a mainstream retail bank is not optional for dating businesses. Mainstream EU banks still reject high-risk applications. The real advantage comes from specialist EMIs and payment institutions that have pre-negotiated frameworks specifically for adult and dating platforms.

Here’s a quick comparison of what EU banking offers versus typical alternatives:

| Feature | EU specialist banking | US banking | Offshore banking |

|---|---|---|---|

| Chargeback rate (adult) | ~9.8% | ~12% to 15% | Variable, often higher |

| Regulatory clarity | High (PSD2/PSD3) | Moderate | Low |

| Account stability | High with specialist EMI | Low for high-risk | Moderate |

| A2A payment access | Yes (SEPA, Wero) | Limited | Rare |

| Compliance support | Structured and ongoing | Minimal | Often absent |

Understanding EU banking advantages at a structural level, and then cross-referencing them against EU banking regulations specific to high-risk sectors, gives you the full picture before you approach any institution.

EU versus non-EU banking: Compliance, cost, and chargebacks compared

Let’s make this concrete with numbers. The gap between EU and non-EU banking for dating businesses isn’t marginal. It’s the difference between a stable, scalable payment operation and a fragile one that requires constant firefighting.

Chargeback rates by geography

The PSD2 chargeback reduction to 9.8% for EU-processed adult transactions in 2023 is a headline figure worth sitting with. A US-processed dating business operating at a 13% chargeback rate faces not only higher dispute costs but also the constant risk of breaching processor thresholds (typically 1% for card networks, measured differently from total transaction volume). EU SCA mandates, which require two-factor authentication for card-not-present transactions, have been the primary driver of this improvement.

| Metric | EU-regulated processing | US-regulated processing |

|---|---|---|

| Average adult chargeback rate | ~9.8% | ~12% to 15% |

| Strong customer authentication | Mandatory (SCA) | Optional or inconsistent |

| Typical processing fee (high-risk) | 2.5% to 3.5% | 3.5% to 5.5% |

| Rolling reserve requirement | 5% to 10% | 10% to 20% |

| Account termination risk | Low (specialist EMI) | High |

What non-EU banks consistently get wrong for dating businesses

- They apply generic high-risk policies without understanding the dating sector’s specific risk profile

- They lack knowledge of age-verification compliance requirements under EU law

- They have no established escalation pathways for chargeback disputes in adult verticals

- They cannot support multi-currency SEPA settlement efficiently

- They routinely fail to distinguish between compliant dating platforms and unregulated adult content

Accessing the right EU payment partners for high-risk businesses addresses most of these gaps directly. The combination of regulatory familiarity and sector-specific experience is what separates a banking relationship that lasts from one that collapses under the first audit. Grounding your setup in payment processing best practices for 2026 ensures you’re not just compliant today but resilient for the regulatory changes ahead.

How to choose and secure an EU bank for your dating business

Knowing EU banking is better isn’t enough. You need to execute the process correctly, because a poorly structured application to an EU institution will fail just as quickly as an application to any mainstream bank. Here is a practical sequence that consistently improves outcomes.

-

Define your regulatory baseline first. Before approaching any bank, confirm your licensing status. An EU-licensed dating business in a jurisdiction like Malta, Cyprus, or Estonia is dramatically easier to bank than an unlicensed platform. If you’re not yet licensed, prioritise this step before banking outreach.

-

Prepare a comprehensive compliance package. This means anti-money laundering (AML) policies, Know Your Customer (KYC) procedures, age-verification documentation, terms of service, privacy policies compliant with GDPR, and corporate structure charts. Banks want to see that your compliance infrastructure is real, not theoretical.

-

Target specialist EMIs and payment institutions, not retail banks. Mainstream EU banks (think large national lenders) still reject high-risk applications as standard. Your target list should focus on EMIs and specialist payment institutions with documented experience in adult and dating verticals.

-

Prepare transaction history and chargeback reports. If you have existing processing data, present it clearly. Demonstrating that your chargeback rate is already at or below sector benchmarks is a powerful onboarding signal.

-

Engage a specialist advisor before submitting applications. Cold applications to EU banking institutions have a high failure rate for dating businesses. An advisor with existing relationships at target institutions can pre-qualify your application and ensure the submission format meets internal expectations.

-

Structure your corporate presence strategically. Certain EU jurisdictions offer more favourable environments for dating businesses. Cyprus, Malta, and certain Baltic states have established regulatory frameworks that banking partners recognise and trust.

-

Plan for ongoing compliance reviews. Securing the account is step one. Maintaining it requires regular compliance audits, proactive chargeback management, and transparent communication with your banking partner.

Pro Tip: EU institutions value consistency over perfection. A business with a slightly elevated chargeback rate that demonstrates active remediation measures is often more bankable than one with a clean record and no documented compliance programme.

The EU banking solutions available to high-risk firms with the right preparation carry an 87% approval rate through specialist channels. Contrast that with the sub-20% approval rate most dating businesses experience when approaching conventional banks cold. Reviewing specific banking approval tips for high-risk sectors before you begin the process reduces the most common and avoidable rejection triggers.

A2A payment growth in EU markets through 2025 and 2026 also means the cost advantage of EU banking for dating businesses will widen, not narrow, over the next two years.

What most businesses miss when switching to EU banking

Here’s the uncomfortable truth we see repeatedly: dating business owners spend months searching for “any bank that will take us” instead of building the infrastructure that makes premium banking partners want to take them.

The obsession with big-brand names is another consistent mistake. Businesses spend time chasing large EU retail banks because the name feels reassuring, while ignoring specialist EMIs that would onboard them in three weeks with better terms. The brand equity of a banking institution means very little when your account gets flagged and frozen. What matters is sector-specific experience and the institution’s internal risk frameworks for adult and dating verticals.

Compliance is the single most underutilised growth lever in this sector. Most dating business owners treat AML policies and KYC procedures as bureaucratic friction. The businesses that scale successfully treat compliance as a commercial asset. A documented, demonstrably functional compliance programme changes how banking partners price your account, how card networks assess your risk tier, and how regulators view your business during audits. It is genuinely competitive.

The payment innovation gap is equally striking. A2A payments like Wero are growing rapidly across European markets, yet most dating businesses are still running entirely on card rails. The fee savings alone justify exploration, but the more significant benefit is reduced chargeback exposure, because A2A payments don’t carry the same dispute mechanisms as card transactions.

Exploring deeper EU banking benefits reveals that the businesses winning in this space aren’t just “banked.” They’ve built multi-layered payment infrastructure with redundancy, lower cost per transaction, and regulatory relationships that protect them from sudden policy shifts. That’s the actual goal. Not “find a bank.” Build a payment ecosystem.

Unlock EU banking expertise for your dating business

The case for EU banking is clear, but executing the move without specialist guidance wastes time and risks further rejections that damage your banking history. At BankMyCapital, we work specifically with high-risk dating and adult businesses to navigate EU banking applications, licensing, and payment infrastructure. Our network of over 50 pre-vetted banking partners and EMIs includes institutions with proven experience in the dating sector, and our 87% approval rate reflects what structured, well-prepared applications achieve. Whether you’re starting from scratch or rebuilding after a banking termination, explore your options through our high-risk sector banking guide, review the full EU banking approval guide for 2026, or go directly to our dating business bank account options. Onboarding typically completes in two to three weeks.

Frequently asked questions

Why are dating enterprises considered high-risk for banks?

Dating companies face high chargebacks, regulatory scrutiny around adult content, and elevated fraud exposure, all of which make banks categorise them as high-risk by default. EU PSD2 has reduced adult chargeback rates to 9.8%, but the classification itself persists without the right banking partner and compliance structure.

Do EU banks really improve approval odds for high-risk businesses?

Specialist EU EMIs and payment institutions offer both regulatory clarity and significantly higher approval rates than traditional US or mainstream banking institutions for high-risk businesses. The key is targeting the right type of EU institution, not EU retail banks broadly.

Is it possible to access lower processing fees with EU-based payment systems?

Yes. A2A payment schemes like Wero are enabling materially lower transaction fees for EU-based high-risk businesses by bypassing traditional card network costs. Specialist providers are necessary to structure access to these rails effectively.

How does EU regulation affect chargeback rates for dating businesses?

PSD2’s strong customer authentication requirements directly reduce fraudulent and disputed transactions. EU adult businesses saw chargebacks drop to 9.8% in 2023, a 22% reduction compared to pre-PSD2 benchmarks and significantly below typical US-processed rates.

What is the biggest mistake dating businesses make with EU banking?

Relying solely on traditional banks rather than specialist EMIs and payment institutions is the most common and costly mistake, because mainstream institutions lack the sector-specific frameworks needed to sustainably serve dating businesses.