TL;DR:

- High-risk industries like iGaming and forex are increasingly able to access regulated crypto banking through mature compliance frameworks. Building a reliable infrastructure involves licensing, automated KYC, transaction monitoring, and multi-jurisdictional reporting to meet evolving AML and ML/TF requirements. Long-term success depends on prioritizing compliance over shortcuts, establishing transparency, and engaging expert guidance throughout the process.

Many high-risk business owners still operate under the assumption that crypto banking is essentially a closed door for their sector. That belief is increasingly outdated. Regulatory frameworks are maturing rapidly, and FATF’s 2026 guidance is actively pushing firms toward regulated routes such as MiCA in the EU or established non-EU hubs like Switzerland, rather than away from crypto banking altogether. This guide unpacks the infrastructure, compliance logic, and practical steps you need to build a banking setup that actually holds up under scrutiny.

Key Takeaways

| Point | Details |

|---|---|

| Tailored solutions exist | High-risk industries can access secure crypto banking with the right infrastructure and compliance planning. |

| Regulatory arbitrage risks | Offshore shortcuts often lead to compliance troubles and loss of institutional trust. |

| MiCA sets the EU standard | EU-compliant solutions offer more sustainable access and payment rail reliability. |

| Documentation is crucial | Every compliance step must be recorded to satisfy bank and regulatory scrutiny. |

| Expert guidance pays off | Investing in professional advice ensures you avoid pitfalls and secure lasting banking relationships. |

Understanding crypto infrastructure for high-risk industries

When we talk about crypto infrastructure, we are not just referring to a wallet and a payment gateway. For iGaming operators, forex brokers, and similar businesses, the stack is considerably more complex. It covers virtual asset service provider (VASP) platforms, which are entities licensed to offer crypto-related services, along with custodial and non-custodial wallet architecture, multi-currency settlement rails, on-chain transaction monitoring tools, and the compliance technology that ties them all together.

High-risk industries carry that label for specific, well-documented reasons. Regulators classify sectors like iGaming and forex as high-risk because they handle large transaction volumes, attract customers across multiple jurisdictions simultaneously, and carry elevated exposure to money laundering (ML) and terrorist financing (TF) risks. This exposure is not hypothetical. It is the reason banks historically refused these businesses outright, and why even today, obtaining a straightforward business account requires significantly more documentation and scrutiny than a standard retail operation would face.

The challenge of institutional trust compounds this. Offshore VASPs frequently use nested structures within regulated host institutions to sidestep licensing requirements, but this approach carries serious ML/TF exposure and is attracting increasing regulatory attention globally. Regulators are not naive about these arrangements, and banks are not either.

The good news is that sector-specific banking platforms have emerged precisely to solve this problem. These platforms understand the operational reality of running an iGaming business or a leveraged forex desk, and they build compliance workflows around those realities rather than against them.

Here is what a functioning crypto infrastructure for a high-risk business typically includes:

- VASP licensing or partnership in a recognised jurisdiction

- KYC/KYB (Know Your Customer / Know Your Business) automation built into onboarding

- Real-time transaction screening using blockchain analytics tools such as Chainalysis or Elliptic

- Fiat-to-crypto and crypto-to-fiat settlement rails for operational liquidity

- Audit trail generation that satisfies both internal compliance and external regulatory review

- Multi-jurisdictional reporting capability to meet AML obligations across different regions

| Infrastructure component | Purpose | Risk if absent |

|---|---|---|

| VASP licence or partnership | Regulatory legitimacy | Operational shutdown |

| KYC/KYB automation | Customer due diligence | AML breaches |

| Transaction monitoring | On-chain risk screening | ML/TF exposure |

| Fiat settlement rails | Liquidity management | Payment failures |

| Audit trail systems | Regulatory reporting | Loss of banking access |

Pro Tip: Choose infrastructure that integrates dynamic compliance checks, meaning automated rule updates that reflect the latest FATF guidance and local AML regulations, rather than static systems that require manual updates. The regulatory environment shifts frequently enough that a static compliance layer can become a liability within months.

If you are exploring how to structure your banking outside of the EU, reviewing offshore banking for crypto businesses is a useful starting point for understanding where the genuine opportunities lie. Equally, the offshore crypto setup guide lays out the practical mechanics of making this work from scratch.

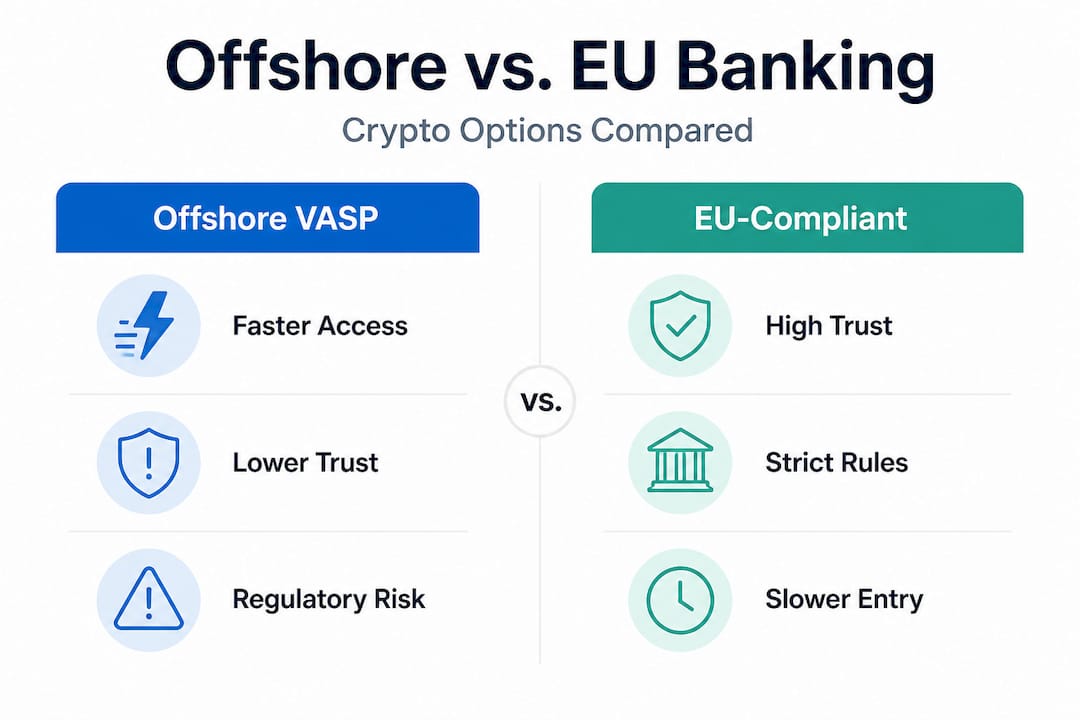

Comparing offshore and EU crypto banking frameworks

With the core infrastructure context established, the next question is which regulatory framework actually fits your business model. The two dominant routes are offshore VASP structures and EU-regulated frameworks, most notably MiCA, which stands for Markets in Crypto-Assets Regulation.

Offshore VASPs offer speed and structural flexibility. In certain jurisdictions, you can obtain a VASP licence and be operational within a matter of weeks. Costs are typically lower, and some offshore centres impose lighter ongoing compliance obligations. That flexibility is attractive, particularly for businesses that are still in their growth phase and want to move quickly.

However, the trade-offs are significant. Offshore structures often struggle to open correspondent banking relationships with tier-one European banks. Payment processors are more expensive, or simply unavailable. And FATF is actively targeting offshore VASPs, pushing high-risk firms towards MiCA for EU market access or towards regulated non-EU alternatives such as Switzerland, which maintains its own rigorous but internationally respected crypto banking framework.

“Offshore lacks institutional trust. FATF targets offshore VASPs, pushing high-risk firms toward MiCA for EU access or regulated non-EU options like Switzerland, which houses some of the leading institutional crypto banks.” — FATF 2026 Framework analysis

EU-compliant banking under MiCA carries a higher entry threshold. You will need to demonstrate capital adequacy, robust governance structures, and comprehensive AML programmes. The process takes longer, and the costs of compliance are ongoing rather than one-off. What you receive in return is access to the full range of European payment rails, institutional banking relationships, and the kind of reputational credibility that actually keeps those relationships intact long-term.

| Framework | Speed to market | Banking access | Regulatory risk | Trust level |

|---|---|---|---|---|

| Offshore VASP | Fast (weeks) | Limited | High and increasing | Low |

| EU MiCA compliant | Slower (months) | Full EU rails | Managed | High |

| Regulated non-EU (e.g. Switzerland) | Moderate | Strong | Low | High |

Leading operators in iGaming and forex are increasingly moving towards compliance-based frameworks, not because regulators have forced their hand, but because offshore shortcut structures are failing operationally. When your payment processor drops you or your bank freezes your account because of an FATF flag on your correspondent banking chain, the cost of that disruption dwarfs the initial savings you made by cutting compliance corners.

Understanding this landscape thoroughly is the foundation of a sound banking strategy. Resources such as offshore banking explained and a clear analysis of why offshore banking matters for high-risk operators help contextualise these decisions before you commit to a structure.

Mitigating compliance risk: ML/TF and regulatory scrutiny

Money laundering and terrorist financing risks are not abstract concerns for iGaming and forex operators. They are the specific reasons your industry faces regulatory scrutiny, and they are the exact lens through which banks and payment processors will evaluate every application you make.

Offshore VASPs that use nested structures within regulated hosts to avoid direct licensing are a textbook example of the kind of arrangement that triggers red flags. The logic behind nested structures is that an unlicensed VASP piggybacks on a licensed institution’s compliance framework. Regulators see through this immediately, and when they act, the consequences extend to the host institution as well.

Practical ML/TF mitigation is not complicated in principle, but it requires consistent execution. Here is a numbered workflow that seasoned operators use:

- Conduct risk-based customer due diligence at onboarding, classifying each customer into low, medium, or high-risk tiers based on geography, transaction behaviour, and source of funds.

- Screen all transactions in real time using blockchain analytics tools to identify wallet addresses associated with sanctioned entities, darknet markets, or suspicious mixing activity.

- Apply enhanced due diligence (EDD) automatically to any customer or transaction that triggers a risk threshold, requiring additional documentation and human review before processing.

- File suspicious activity reports (SARs) with the relevant financial intelligence unit (FIU) in your jurisdiction whenever a transaction meets the reporting threshold.

- Conduct quarterly AML policy reviews to incorporate updated FATF guidance, changes to sanctions lists, and emerging typologies in your sector.

- Maintain a comprehensive audit trail for every step above, with timestamps, analyst notes, and resolution outcomes stored in a format that regulators can audit on request.

Statistic callout: Regulatory actions against offshore VASPs have increased materially as FATF’s 2026 framework tightens expectations for correspondent banking relationships and beneficial ownership transparency.

Pro Tip: Document every compliance action at the transaction level, not just at the customer level. Banks reviewing your application will often request sample transaction files. If your records show a consistent, auditable compliance process at a granular level, it significantly strengthens their confidence in your operation.

For a structured approach, the crypto compliance checklist covers the key AML requirements for high-risk banking applicants. And if you need to assess your current payment operations, reviewing crypto payment processing best practices helps identify gaps before they become bank rejection reasons.

Designing crypto banking workflows for iGaming, forex, and similar sectors

Compliance frameworks are only as effective as the workflows built around them. Understanding regulatory requirements is the foundation, but building operational banking workflows that function day-to-day in your specific industry is where the real work happens.

Start by mapping your operational requirements clearly. Ask yourself: what jurisdictions do your customers come from? What transaction volumes do you process monthly? Do you settle in fiat, crypto, or both? What licensing do you already hold? These parameters determine which banking partners and infrastructure vendors can realistically serve you, and which will simply decline at the due diligence stage.

A practical onboarding workflow for a high-risk crypto banking relationship looks like this:

- Prepare your KYC/KYB package covering corporate structure, beneficial ownership, source of funds, and existing licences or regulatory approvals.

- Submit to a pre-vetted banking partner that already understands your sector, rather than cold-applying to institutions with no high-risk appetite.

- Complete enhanced due diligence as requested, providing transaction history, customer risk segmentation data, and your AML policy documentation.

- Agree on transaction monitoring parameters with your banking partner, including volume thresholds, geographic restrictions, and escalation procedures.

- Establish settlement frequency and currency pairs to ensure your operational liquidity needs are met without triggering unnecessary compliance holds.

- Set up ongoing compliance reporting to your banking partner on a quarterly basis, proactively sharing AML updates and any material changes to your business.

Critical features your banking platform must include:

- Multi-currency settlement including major stablecoins and fiat currencies relevant to your customer base

- Integrated blockchain analytics so that on-chain transaction screening is part of the core product, not a bolt-on

- Transparent ownership and governance visible to banking partners, which removes a common due diligence obstacle

- Real-time compliance monitoring dashboards accessible to both your compliance team and, where relevant, your banking partner

- Robust API connectivity to your existing payment processing infrastructure

One common pitfall worth highlighting specifically is the misapplication of reverse solicitation under MiCA. Reverse solicitation is narrow and scrutinised particularly around marketing activities. Some operators mistakenly believe that by not actively marketing into the EU, they can serve EU customers without MiCA authorisation. Regulators and banking partners do not view this generously. If you are serving EU customers at scale, MiCA authorisation or a compliant local partner is the only defensible route.

Reviewing payment processing solutions designed specifically for high-risk industries will help you identify which providers align with these workflow requirements from the outset.

Why most high-risk crypto operators get compliance wrong—and what actually works

Here is the uncomfortable reality we see repeatedly: most high-risk business owners approach crypto banking as a cost to be minimised rather than an asset to be built. They look for the fastest licence, the lightest compliance requirement, the jurisdiction that asks the fewest questions. And then, six to eighteen months later, they find themselves scrambling when their accounts are frozen, their payment processor has offboarded them, or their correspondent bank has flagged their operation.

The businesses that sustain long-term crypto banking access are not the ones that found clever shortcuts. They are the ones that invested early in compliance infrastructure that their banking partners could actually rely on. They standardised their KYC processes before they were asked to. They hired compliance officers rather than outsourcing the function entirely to a shelf-company structure. They chose banking partners through proper advisory processes rather than accepting the first offshore account that would take them.

The myth of the lowest-friction solution being the smartest move is particularly damaging in this sector. A fast offshore account with minimal compliance requirements might feel like a win initially. But when your payment volume scales, the weaknesses in that structure become exponentially more visible. Banks looking at your correspondent chain will see the gaps. Processors running enhanced due diligence will flag the risk. The account that cost you nothing to open will cost you far more to replace under operational pressure.

What actually gets high-risk businesses approved by EU-regulated banks and respected offshore institutions comes down to a few consistent factors:

- Transparent ownership structures with no unexplained layers or nominee arrangements

- Documented AML programmes that reflect real implementation, not just policy documents

- Sector-relevant licensing from a jurisdiction that your target banking partners recognise

- A track record of compliant operations, even if it comes from a prior banking relationship

- Proactive engagement with banking partners rather than reactive responses to due diligence requests

For operators benchmarking their current setup, reviewing best offshore banks for crypto and gambling gives a realistic view of what compliant, high-quality banking access actually looks like in practice.

Secure your high-risk crypto banking journey with expert support

The path from regulatory confusion to a secure, functioning crypto banking relationship is navigable, but it requires the right guidance from the start. At BankMyCapital, we work exclusively with high-risk operators in crypto, iGaming, forex, and related sectors, matching you with pre-vetted banking partners who already understand your industry and will not reject you at the first compliance question. Our crypto banking setup guide outlines exactly what the onboarding process looks like, and our advisory team helps you avoid the banking rejection risks that derail so many applications before they get started. If EU compliance is your priority, our crypto business banking EU compliance resource details the specific requirements and how we support you through each stage, from jurisdiction selection to regulatory liaison and beyond.

Frequently asked questions

Can high-risk industries still access crypto banking in 2026?

Yes, access is genuinely available through compliant platforms and expert-advised solutions. The FATF 2026 framework is directing high-risk firms towards regulated routes such as MiCA rather than closing the door on crypto banking.

What are the main regulatory risks for offshore crypto operations?

Offshore platforms face escalating scrutiny for using nested structures within regulated hosts, which exposes both the operator and the host institution to money laundering and terrorist financing risks.

Is MiCA compliance mandatory for all EU-facing crypto businesses?

MiCA compliance is required for meaningful EU market access. Reverse solicitation exceptions are interpreted narrowly and are subject to close regulatory monitoring, so they offer limited practical protection at scale.

How do you select a compliant crypto banking infrastructure?

Prioritise platforms with transparent ownership, embedded KYC/KYB automation, and real-time blockchain transaction monitoring. These three factors are what banking partners most consistently scrutinise during due diligence.

What is the biggest mistake high-risk firms make in crypto banking?

Prioritising speed over compliance is the single most common and costly error. Firms that optimise for fast, low-scrutiny onboarding consistently face service disruptions, account closures, or complete loss of banking access as their volumes grow.