TL;DR:

- High-risk businesses must thoroughly assess risks, prepare documentation, and match with suitable processors.

- Using multiple providers and embedding compliance ensures payment operations remain flexible, secure, and scalable.

- Ongoing testing, monitoring, and optimizing are vital for stable high-risk payment processing.

Getting payment processing right is one of the most consequential decisions a high-risk business makes. For operators in crypto, iGaming, forex, and adult entertainment, a poorly configured payment stack means rejected transactions, frozen accounts, and compliance penalties that can halt operations overnight. Chargebacks, fraud exposure, and regulatory scrutiny make these sectors uniquely vulnerable. This guide walks you through every stage of a robust setup: from assessing your risk profile and selecting the right processing model, to embedding compliance safeguards and optimising performance over time. Follow this roadmap and you will avoid the most costly mistakes.

Key Takeaways

| Point | Details |

|---|---|

| Prepare key documents | Gather company, compliance, and licensing materials before applying for processing. |

| Select the right model | Choose and combine processing models to reduce risk and improve approval rates. |

| Build in compliance | Integrate KYC, AML, and chargeback controls from the outset to avoid penalties. |

| Test and monitor | Regular health checks and prompt provider communication keep your processing stable. |

Assessing risks and requirements before setup

Before you approach a single payment provider, you need to understand exactly what makes your business high-risk and what documentation you must have ready. Regulators and processors do not give second chances to unprepared applicants.

What makes a business high-risk?

Crypto exchanges, iGaming platforms, forex brokers, and adult content sites all share common traits that trigger processor caution: elevated chargeback rates, complex regulatory environments, cross-border transactions, and reputational sensitivity. If your business operates in any of these sectors, you are already flagged before you submit a single application.

Common risk indicators processors look for include:

- Chargeback ratios above 1% of monthly transaction volume

- High average transaction values or irregular volume spikes

- Customers located in restricted or high-risk jurisdictions

- Business models involving recurring billing or subscription structures

- Absence of a recognised gaming, financial, or adult content licence

Core requirements you must prepare

Every serious processor will ask for a standard set of documents before onboarding. Missing even one delays your application by weeks. Prepare the following before making contact:

- Certificate of incorporation and corporate structure chart

- Certified identification for all directors and ultimate beneficial owners

- A written KYC and AML compliance manual

- Proof of relevant licensing (gaming authority, FCA, FSA, or equivalent)

- Three to six months of processing history if available

- Website screenshots and terms of service documentation

Assess your transaction volume, target currencies, and customer geography upfront. A processor specialising in European iGaming will not be the right fit for a crypto exchange serving Asian markets. Matching your profile to the right provider from day one is critical. Reviewing best practices for high-risk businesses before you begin can sharpen your preparation considerably.

Pro Tip: If you anticipate a volume spike due to a promotion or product launch, notify your processor in writing at least two weeks in advance. Unexplained spikes are one of the leading causes of sudden account holds.

| Sector | Key licence required | Primary risk flag | Typical chargeback threshold |

|---|---|---|---|

| iGaming | Gaming authority (MGA, UKGC) | Fraud, addiction claims | 1% |

| Crypto | VASP registration | Regulatory ambiguity | 0.5% |

| Forex | FCA, CySEC, or equivalent | Dispute-heavy clients | 0.75% |

| Adult | Age verification compliance | Reputational risk | 1% |

Choosing the right payment processing model

With your documents ready and your risk profile mapped, the next decision is which payment processing architecture will serve your business best. There is no single correct answer, and the wrong choice costs you in fees, approvals, and downtime.

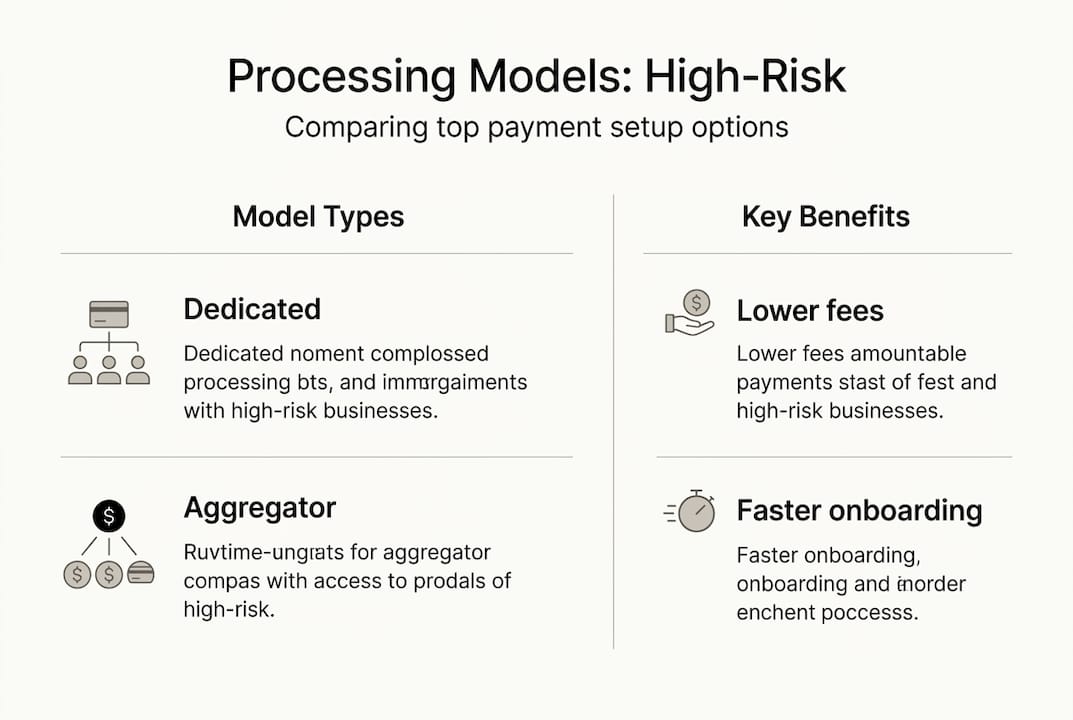

The four main models

- Dedicated high-risk processors specialise exclusively in sectors like yours. They accept higher chargeback ratios and offer tailored fraud tools, but charge premium rates.

- Payment aggregators pool merchants under a single master account. Faster to set up, but one bad actor in the pool can trigger account-wide reviews.

- Direct acquiring means negotiating a merchant account directly with an acquiring bank. Slower and more demanding, but offers the best rates and stability long-term.

- Hybrid stacks combine two or more of the above, often pairing a dedicated processor with crypto or alternative payment methods (APMs) for redundancy.

| Model | Best for | Main advantage | Main risk |

|---|---|---|---|

| Dedicated processor | All high-risk sectors | Sector expertise | Higher fees |

| Aggregator | Early-stage businesses | Fast onboarding | Shared liability |

| Direct acquiring | Established operators | Low rates, stability | Lengthy approval |

| Hybrid stack | Scaling businesses | Redundancy, flexibility | Complexity |

Multi-provider stacks and APMs enhance redundancy and reduce card dependency, which is especially critical for iGaming and crypto operators whose card approval rates can fluctuate sharply.

How to shortlist and compare providers

- Define your monthly volume, average ticket size, and top five customer countries.

- Filter providers by sector specialisation and jurisdiction coverage.

- Request indicative fee schedules and rolling reserve terms in writing.

- Ask for references from businesses in your exact sector.

- Confirm integration options (API, hosted page, or plugin) match your technical setup.

Explore processing solutions for high-risk industries and review crypto payment processing options before finalising your shortlist.

Pro Tip: Aim to route at least 30 to 40% of your payment volume through crypto or APMs. This reduces your dependence on card networks, which are the most volatile channel for high-risk businesses.

Integrating compliance and security safeguards

Selecting a processor is only half the work. Embedding compliance and security into your payment workflow is what keeps your accounts open and your business protected from regulatory action.

KYC and AML: what regulators actually expect

Know Your Customer (KYC) and Anti-Money Laundering (AML) processes are not optional extras. They are the baseline that every regulator and processor expects you to operate. Your compliance programme must include identity verification at onboarding, ongoing transaction monitoring, and a clear escalation path for suspicious activity.

Main compliance steps for payment onboarding:

- Verify all customer identities using government-issued documents and liveness checks

- Screen customers against sanctions lists (OFAC, EU, UN) at onboarding and on an ongoing basis

- Set transaction velocity rules to flag unusual patterns automatically

- Maintain a documented audit trail for every transaction

- Appoint a named compliance officer responsible for regulatory reporting

- Review and update your AML policy at least annually

For a structured approach to all of this, the compliance steps outlined for high-risk finance provide a reliable framework.

Chargeback mitigation: the 1% rule

Failing to maintain chargebacks below processor thresholds can result in account termination, fines from card networks, and permanent placement on industry blacklists such as MATCH. The reputational damage alone can take years to reverse.

The industry standard is clear: keep chargebacks below 1% of monthly transactions using alerts, representments, and AI-driven fraud tools that improve dispute win rates over time. Chargeback alert services such as Ethoca and Verifi notify you of disputes before they become formal chargebacks, giving you a window to issue refunds and avoid the penalty.

On the security side, ensure your payment infrastructure is PCI-DSS Level 1 compliant, uses tokenisation for stored card data, and layers in 3D Secure authentication for card-not-present transactions. These are not nice-to-haves. They are conditions of most processor agreements.

Test, monitor, and optimise your payment processing

With your compliance framework embedded and your processing stack live, the final stage is rigorous testing, disciplined monitoring, and continuous improvement. Most payment failures happen not at setup, but in the weeks following go-live.

Pre-launch testing

Before you accept a single live transaction, run end-to-end tests across every payment method, currency, and customer journey your platform supports. Test edge cases: failed payments, partial refunds, currency conversion errors, and timeout scenarios. A payment flow that breaks under unusual conditions will break in production at the worst possible moment.

Weekly and monthly health checks

- Review chargeback ratios by payment method and customer segment weekly.

- Monitor settlement timelines and flag any delays beyond agreed terms immediately.

- Track APM uptake as a percentage of total volume monthly.

- Compare approval rates across providers and routes to identify underperformers.

- Audit your rolling reserve balance and ensure it aligns with your processor agreement.

- Review fraud alerts and update velocity rules based on emerging patterns.

Notifying your processor before volume spikes is critical to avoiding account freezes, and this discipline should become a standard part of your monthly planning cycle. The high-risk approval guide provides additional benchmarks for what healthy processing metrics look like.

Optimising over time

As your data accumulates, you will spot patterns. Certain APMs may outperform cards in specific markets. Some customer segments may generate disproportionate chargeback risk. Use this intelligence to adjust your routing rules, shift volume between providers, and retire underperforming channels.

Pro Tip: Establish a named contact at each of your payment providers, not just a support ticket queue. A direct relationship means faster resolution when something goes wrong, and in high-risk processing, something always eventually goes wrong.

Why modern high-risk payment setups must be flexible and proactive

There is a persistent belief in this industry that once you find a processor willing to work with you, you lock in and stay put. We have seen this approach fail repeatedly. Processors exit sectors, regulators shift requirements, and card networks update their risk thresholds with little warning. A static payment setup is a liability.

The businesses that maintain stable processing in 2026 are those treating their payment stack as a living system. They maintain multiple providers, rotate APM mix based on performance data, and communicate proactively with every banking partner. Payment processing best practices now demand this level of operational agility, not just at launch, but on an ongoing basis. Redundancy is not a luxury. It is the minimum viable standard for any serious high-risk operator.

Next steps: find the best payment processing and banking partners

Ready to put these steps into action? BankMyCapital works exclusively with high-risk operators in crypto, iGaming, forex, and adult entertainment, connecting you with a network of over 50 pre-vetted banking partners and EMIs. Whether you need a reliable payment processing partner, guidance on reducing banking rejection risks, or a structured banking checklist for success, our team provides hands-on support from first application through to live processing. With an 87% approval rate and onboarding in as little as two to three weeks, we remove the guesswork from high-risk banking.

Frequently asked questions

What documents are needed to set up high-risk payment processing?

Typically, you will need company registration, directors’ IDs, a compliance manual, proof of licensing, and KYC details for all ultimate beneficial owners. Core onboarding requirements including legal registration and licensing are non-negotiable for any serious processor.

How can I keep chargebacks below 1%?

Use chargeback alert services, respond quickly to disputes, and deploy AI-driven fraud tools that learn from your transaction patterns. Alerts and representments combined with AI tooling are the most effective combination currently available.

Why should I use multiple providers for payment processing?

Spreading volume across providers reduces single-point failure risk, adds redundancy, and increases your overall approval odds with banks and regulators. A multi-provider stack is now considered standard practice for any high-risk business operating at scale.

What is the role of crypto in high-risk payment processing?

Cryptocurrency can account for 30 to 40% of payment volume, directly reducing card dependency and increasing processing resilience. Diversifying with crypto provides greater stability when card networks tighten their risk policies unexpectedly.