TL;DR:

- High-risk sectors face high rejection rates, costly processing fees, and significant chargeback risks. Proper preparation, comprehensive documentation, and continuous compliance monitoring are essential for success. Expert support and sector-specific strategies improve stability and long-term payment processing relationships.

Getting your transactions frozen on launch day is not just an inconvenience. It can cost you thousands in lost revenue, damage customer trust, and trigger a cascade of compliance flags that follow your business for months. High-risk sectors including iGaming, crypto, forex, and adult entertainment face rejection rates that would floor most standard merchants, and the consequences of a poorly structured payment setup are rarely forgiving. This guide walks you through every critical stage, from understanding your risk profile to verifying a fully compliant, live payment operation, so you can move forward with clarity rather than guesswork.

Key Takeaways

| Point | Details |

|---|---|

| Expect higher costs | High-risk businesses face increased fees, chargeback penalties, and stricter requirements compared to standard merchants. |

| Preparation is essential | Gather thorough documentation and address compliance checks before applying to avoid costly delays. |

| Follow each step closely | Adhering to a systematic payment setup process is critical to approval and operational continuity in high-risk sectors. |

| Monitor ongoing risk | Daily monitoring of chargebacks, fraud, and reserves minimises financial losses and retains provider trust. |

Understanding payment processing risks for high-risk businesses

Not every business that gets labelled “high-risk” is doing anything wrong. The classification is largely based on statistical likelihood of chargebacks, regulatory exposure, and the financial burden a processor might absorb if things go sideways. Industries such as online gambling, cryptocurrency exchanges, forex trading, subscription adult content, and nutraceuticals regularly fall into this category regardless of how well-run they are.

Banks and payment processors assess risk through several overlapping lenses. They look at your industry code (MCC), your projected monthly volume, your chargeback history, your geographical footprint, and the regulatory environment of your jurisdiction. A crypto business operating from a lightly regulated territory with no processing history will face a very different reception than an EU-licensed iGaming operator with two years of clean statements.

The financial reality is stark. High-risk processing fees typically run 4 to 8% per transaction compared to 2 to 3% for standard merchants, and chargeback fees range from $25 to $100 each. Worse still, every $1 of fraud translates into $4.61 in total losses once you account for operational costs, dispute handling, and lost goods or services. These numbers make it clear that poor preparation is not just an administrative problem; it is a direct financial threat.

Here are the main threats to a successful payment processing setup in high-risk sectors:

- Regulatory non-compliance: Operating without the correct licence in your target jurisdiction triggers automatic rejections from most EU-regulated processors.

- Chargeback ratios above threshold: Visa and Mastercard both impose monitoring programmes once your chargeback ratio crosses 1%, and many processors terminate accounts well before that.

- Reputational exposure: Processors conduct media searches. If your business or directors appear in adverse news, onboarding stalls or fails entirely.

- Fraud exposure: Without robust fraud screening tools, high-risk businesses are disproportionately targeted, and losses compound rapidly.

- Technical integration failures: Poorly integrated payment gateways create customer friction and processing errors, both of which inflate chargeback rates.

Understanding these threats is foundational. You can explore how processors specifically evaluate high-risk merchant accounts to understand how the risk scoring works in practice before you begin your applications.

Essential requirements and documents for setup

Preparation is where most high-risk operators either gain a decisive advantage or doom their application before it is even reviewed. Processors in this space are experienced at spotting gaps, and missing a single document can delay your onboarding by weeks or result in outright rejection.

The following documents are typically required for a complete application:

| Requirement | Purpose | Submission tip |

|---|---|---|

| Certificate of incorporation | Confirms legal entity status | Ensure it is notarised and apostilled if offshore |

| Director/shareholder KYC | Anti-money laundering (AML) compliance | Include passports, proof of address dated within 3 months |

| Business licence | Proves regulatory authorisation | Confirm it covers your exact business activity |

| Processing history (3 to 6 months) | Demonstrates volume and chargeback record | Include month-by-month breakdown if possible |

| AML/KYC policy documents | Shows internal compliance framework | Have legal counsel review before submitting |

| Bank statements (3 to 6 months) | Evidences financial stability | Highlight consistent inflows and low dispute ratios |

| Website compliance review | Confirms terms, age verification, responsible gaming (if applicable) | Fix any non-compliant pages before applying |

Beyond gathering documents, you need to anticipate the reserve requirement. Reserves are standard at setup, and processors typically hold between 5% and 10% of monthly processing volume as a security buffer against chargebacks. This is non-negotiable at the start, but the terms are very much negotiable over time.

Pro Tip: When agreeing to a reserve, build in a quarterly review clause from day one. Processors are far more amenable to this conversation during initial negotiations than six months after you have signed. Tie the review to specific performance metrics, such as maintaining a chargeback ratio below 0.5% for 90 consecutive days, and put it in writing.

You can find a detailed breakdown of all required account documents and a full walkthrough of the banking setup steps that apply specifically to high-risk businesses operating across multiple jurisdictions.

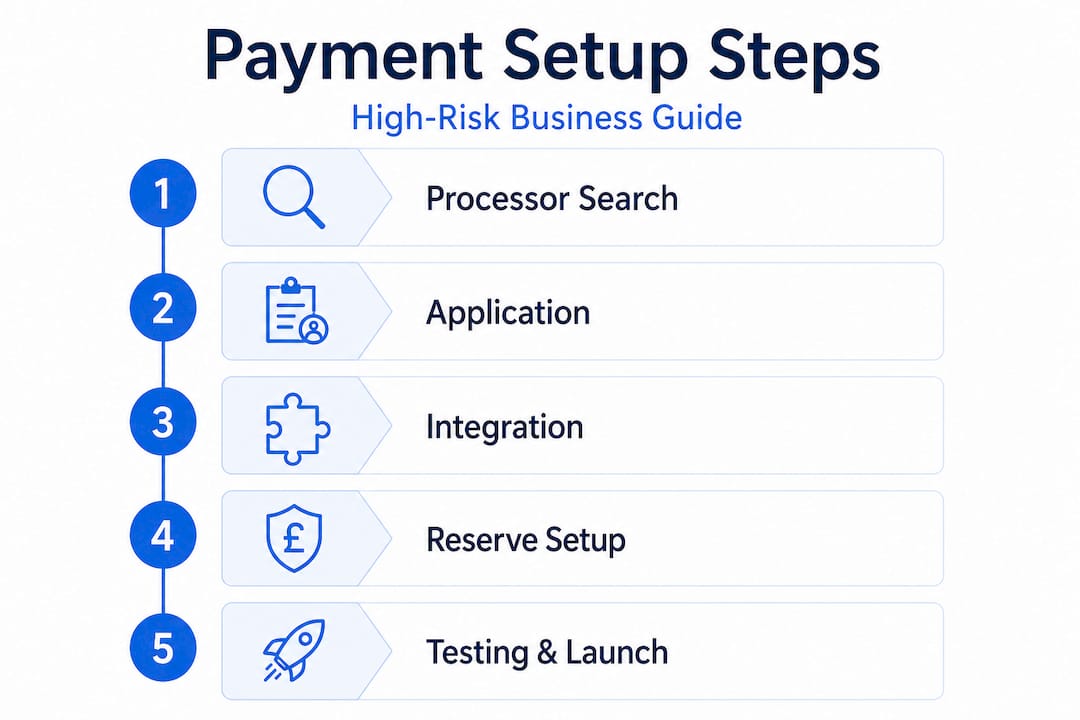

Step-by-step payment processing setup process

With your documentation in order, you can move through the setup process systematically. Each step has specific decision points that are unique to high-risk operators and deserve careful attention.

Step 1: Research and select a compliant payment processor

Not all processors accept high-risk merchants, and among those that do, the terms, supported currencies, and jurisdictional coverage vary enormously. Prioritise processors with demonstrated experience in your vertical, not just those that claim to accept “all industries.” Ask directly for their chargeback thresholds, reserve policies, and termination conditions before signing anything.

Step 2: Prepare your application to maximise approval

Frame your application around risk mitigation, not just business opportunity. Processors want to see that you understand the risks in your sector and have controls in place. Include your fraud prevention tools, your chargeback response process, and your AML policy upfront. Businesses that demonstrate awareness of their risk profile are consistently rated more favourably. Review approval strategies to understand exactly what processors look for in a compelling application.

Step 3: Technical integration and security protocols

Once approved, integration matters enormously. Use a PCI DSS-compliant payment gateway, implement 3D Secure 2.0 authentication for card transactions, and ensure your fraud screening tools are active before going live. Rushed technical integrations are one of the leading causes of post-launch chargeback spikes.

Step 4: Reserve account setup and negotiation

Agree your rolling reserve or upfront reserve terms, document the review schedule, and open a dedicated reserve account if your processor requires it. Keep this account funded to the agreed level to avoid processing interruptions.

Step 5: Conduct test transactions and live launch

Run a structured testing phase using real cards across different card schemes, geographies, and transaction values. Confirm that declines, refunds, and disputes all route correctly through your systems. Only go live when every scenario has been tested and documented.

| Factor | Traditional bank processors | Specialist high-risk processors |

|---|---|---|

| Approval likelihood | Low for high-risk sectors | Significantly higher |

| Processing fees | 2 to 3% | 4 to 8% |

| Chargeback tolerance | Very low | Calibrated to sector |

| Reserve requirements | Rare | Standard at setup |

| Jurisdictional flexibility | Limited | Multi-jurisdiction capable |

| Onboarding time | 4 to 8 weeks | 2 to 4 weeks (specialist) |

Pro Tip: Before going live, benchmark your expected chargeback ratio against industry standards. High-risk ecommerce benchmarks sit at 0.5 to 0.8%, subscription businesses at 0.7 to 1.2%, and digital goods above 1%. If your model suggests you will land near the top of these ranges, build your dispute resolution process before launch, not after.

For a more detailed walkthrough of each stage, the detailed payment setup guide covers integration specifics and processor selection criteria in full.

Troubleshooting and avoiding common mistakes

Even well-prepared businesses run into problems. The difference between a temporary setback and a terminal account termination is often how quickly you identify the issue and how methodically you respond.

The most frequent causes of setup failures and post-launch problems include:

- Incomplete or inconsistent documentation: A single mismatch between your registered address on your corporate documents and your bank statements can halt onboarding entirely. Cross-check every detail before submission.

- Ignoring chargeback monitoring from day one: Many operators wait until they receive a formal warning before taking action. By then, the ratio is already elevated and recovering it is significantly harder.

- Weak dispute response scripts: When a chargeback is filed, you typically have a narrow window to respond with compelling evidence. Generic responses fail. Tailor your rebuttal template to your specific business model and the reason code on the dispute.

- Underestimating fraud costs: The financial exposure from fraud is not limited to the disputed transaction value. Every $1 of fraud generates $4.61 in total losses, making even a modest fraud rate genuinely damaging at scale.

- Failing to update processors on business changes: Launching a new product line, entering a new market, or changing your primary acquiring relationship without notifying your processor can trigger a compliance review or account freeze.

“The businesses that survive long-term in high-risk payment processing are not necessarily those with the lowest fraud rates at launch. They are the ones with the fastest, most disciplined response systems when things go wrong.”

Addressing these issues quickly requires a clear internal protocol. Assign a named compliance contact for all processor communications, keep a live chargeback log updated daily, and schedule a fortnightly internal review of your fraud data. Explore processing best practices for structured frameworks, and review how top payment partners in Europe manage risk at scale.

Verifying your setup and ongoing compliance

A successful launch is not the finish line. The ongoing management of your payment processing relationship is where the real work begins, and where most accounts either stabilise or gradually deteriorate.

Your post-launch compliance checklist should include:

- Confirm that all test transactions have been reversed and reconciled before the first settlement.

- Verify that chargeback notifications are routing to the correct team with response deadlines clearly flagged.

- Check that your fraud screening thresholds are calibrated to your live transaction data, not your test environment assumptions.

- Review your first monthly settlement statement line by line to confirm fees match your agreed terms.

- Establish a communication rhythm with your processor account manager, at minimum monthly, and document each conversation.

- Set automated alerts for when your daily chargeback count exceeds a predetermined threshold.

- Schedule your first quarterly reserve review before the 90-day mark.

Chargeback rate benchmarks for high-risk businesses make clear that monitoring VAMP (Visa Acquirer Monitoring Programme) and ECP (Early Chargeback Programme) indicators daily is not optional. Ecommerce benchmarks of 0.5 to 0.8%, subscriptions at 0.7 to 1.2%, and digital goods above 1% should serve as your internal red lines, not the processor’s formal thresholds. Reserves remain standard at setup, but quarterly reviews are achievable once you can demonstrate consistent, documented performance.

Pro Tip: Set up automated daily reports from your payment gateway showing transaction volume, decline rates, and chargeback counts. Configure threshold alerts so that when any metric moves more than 15% from its rolling average, your compliance team receives an immediate notification. Early detection is always cheaper than remediation. Review processing solutions tailored to high-risk sectors for tools that support this kind of real-time monitoring.

Why rigorous prep and ongoing checks matter most

Here is the perspective that most payment processing guides will not give you: the technology is rarely the problem. Modern payment gateways are reliable, APIs are well-documented, and integration support is widely available. What fails high-risk businesses is almost always the human and compliance layer, specifically the decision to rush the preparation phase and the habit of treating post-launch monitoring as a passive activity.

We see this pattern repeatedly. A business invests significant effort in selecting a processor, negotiates reasonable fees, and launches successfully. Then, six weeks in, the chargeback ratio creeps up, nobody catches it until it crosses the processor’s threshold, and the account is placed under review or terminated. The technology never failed. The monitoring did.

The businesses that achieve stable, long-term payment processing relationships in high-risk sectors share one characteristic: they treat compliance as a continuous operating function, not a one-time setup task. Routine internal audits, real-time threshold alerts, and monthly processor communications are not administrative overhead. They are the direct cause of lower reserve requirements, better fee negotiations, and uninterrupted processing, all of which compound into a material competitive advantage over time.

The other insight worth stating plainly: high-risk best practices consistently show that businesses which invest in proper jurisdictional structuring and licensed operations before applying for payment processing achieve dramatically better outcomes than those attempting to retrofit compliance after the fact. Your payment processor is not your compliance partner. Your internal systems and advisors are. That distinction changes everything about how you approach setup.

Secure your payment processing setup with expert support

Navigating payment processing as a high-risk operator involves layers of regulatory detail, jurisdictional nuance, and processor-specific requirements that can derail even well-resourced businesses. At BankMyCapital, we work with iGaming, crypto, forex, and adult entertainment businesses to build compliant, robust payment setups backed by a network of over 50 pre-vetted banking partners and EMIs. Whether you are starting from scratch or recovering from a rejected application, our banking rejection risks guide and the banking success checklist are practical starting points. When you are ready to move forward, the payment setup guide maps out every stage with sector-specific detail.

Frequently asked questions

What qualifies a business as high-risk for payment processing?

High-risk businesses typically operate in sectors with elevated chargeback rates, significant regulatory scrutiny, or greater fraud exposure, including sectors such as gaming, adult content, crypto, and forex. Processors assess risk using industry codes, processing history, and geographic footprint.

How much does high-risk payment processing really cost?

Processing fees for high-risk businesses typically run between 4 and 8% per transaction, with individual chargeback fees ranging from $25 to $100, making cost management a core operational priority from day one.

What is a chargeback benchmark for high-risk sectors?

High-risk ecommerce benchmarks sit at 0.5 to 0.8%, subscription businesses at 0.7 to 1.2%, and digital goods above 1%, and these figures should be treated as internal red lines rather than hard limits set by your processor.

Is it possible to negotiate reserves set by payment processors?

Yes. Reserves are common at setup but many providers are open to quarterly reviews, particularly when you can demonstrate sustained low chargeback ratios and consistent transaction volumes over a defined period.

What is the financial impact of payment fraud for high-risk businesses?

Every $1 of fraud generates $4.61 in total losses once indirect costs such as dispute handling, operational time, and reputational exposure are factored in, making real-time fraud monitoring a financial necessity rather than an optional extra.