Thousands of legitimate businesses operating in crypto, iGaming, and forex are turned away by banks every year, not because of wrongdoing, but simply because of the sector they operate in. Many legitimate high-risk businesses are denied accounts purely on the basis of industry classification. This creates a damaging misconception: that high approval banking is somehow a shortcut or a loophole. It is not. This guide explains exactly what high approval banking means, why it exists, what genuine solutions look like, and how your business can access reliable, compliant accounts in the EU and offshore.

Key Takeaways

| Point | Details |

|---|---|

| High approval means tailored compliance | Genuine high approval banking focuses on supporting high-risk businesses through bespoke compliance, not lax standards. |

| Preparation boosts approval rates | Organising documentation and demonstrating regulatory readiness can increase your success by up to 70%. |

| Choose providers carefully | Only regulated, sector-experienced banks provide safe, sustainable solutions for crypto, iGaming, and forex businesses. |

| EU versus offshore trade-offs | EU accounts offer robust compliance while offshore accounts provide speed and flexibly, so many firms use both. |

Defining high approval banking for high-risk sectors

High approval banking is not a magic door that opens for anyone willing to pay a fee. It refers to specialised banking services designed specifically for businesses that operate in sectors traditional banks consider too risky to serve. Think crypto exchanges, online casinos, forex brokers, and adult platforms. These businesses are not inherently illegal. They are simply complex, and most retail banks lack the internal frameworks to assess them properly.

The critical distinction is this: high approval banking differs from “anyone accepted” services. It means tailored, compliance-ready solutions built around your sector’s specific regulatory requirements. A genuine high approval provider will conduct thorough due diligence, not skip it.

What problems does this actually solve? Here are the core ones:

- Access to IBAN accounts and SWIFT/SEPA payment rails for day-to-day operations

- Merchant accounts capable of processing high transaction volumes

- Multi-currency accounts suited to international business models

- Ongoing compliance support to prevent sudden account closures

- Relationships with banks that understand sector-specific risk profiles

Pro Tip: If a provider promises instant approval with zero documentation, walk away. Genuine high approval banking always involves a compliance review. That review is what protects your account long-term.

Common reasons high-risk businesses are rejected by banks

Understanding what high approval banking is explains why typical banks often say no. The reasons are rarely personal. They are structural.

Bank rejections are usually driven by perceived compliance or reputational risks that the bank is unwilling to absorb. Here are the most common causes:

- Sector classification — The bank’s internal policy simply excludes your industry, regardless of your compliance record.

- Incomplete KYC documentation — Missing or inconsistent Know Your Customer files trigger automatic rejections.

- Unclear source of funds — Banks need to trace where your capital originates. Crypto businesses often struggle here.

- No regulatory licence — Operating without a recognised licence in your jurisdiction is an immediate red flag.

- High chargeback ratios — iGaming and forex businesses frequently face this issue due to the nature of their transactions.

- Reputational exposure — If your business has been associated with negative press or regulatory action, banks will find it.

The scale of this problem is significant. Across the EU, high-risk account approval rates at traditional banks sit well below 30% for sectors like crypto and iGaming. That is not a niche issue. It affects the operational viability of thousands of businesses.

The good news is that each of these rejection triggers has a solution. Proper preparation, the right jurisdiction, and a compliance-ready application package change the outcome dramatically.

Key features of high approval banking accounts

Once you know why businesses are rejected, it becomes clear what a genuine high approval account must deliver. Not every provider offers the same standard, so knowing what to look for matters.

High approval banks typically offer enhanced onboarding and tailored compliance frameworks built around your sector. Here is what that looks like in practice:

| Feature | Traditional bank | High approval bank |

|---|---|---|

| Sector acceptance | Rarely | Yes, for regulated high-risk firms |

| KYC/AML support | Generic | Sector-specific |

| Onboarding time | Weeks to months | 2 to 3 weeks (typical) |

| Account manager | Shared | Dedicated |

| Multi-currency support | Limited | Standard |

| De-risking resilience | Low | High |

Beyond the table, the real differentiator is ongoing support. A high approval provider does not disappear after onboarding. They monitor regulatory changes, flag compliance gaps, and help you maintain your account in good standing.

Key features to confirm before signing with any provider:

- Dedicated compliance officer assigned to your account

- Clear AML (Anti-Money Laundering) policy aligned with your jurisdiction

- Transparent fee structure with no hidden charges

- Access to a bank account opening checklist tailored to your sector

Pro Tip: Ask any prospective banking partner which specific regulatory frameworks they operate under. A credible provider will name the exact directives, such as the EU’s AMLD6, without hesitation.

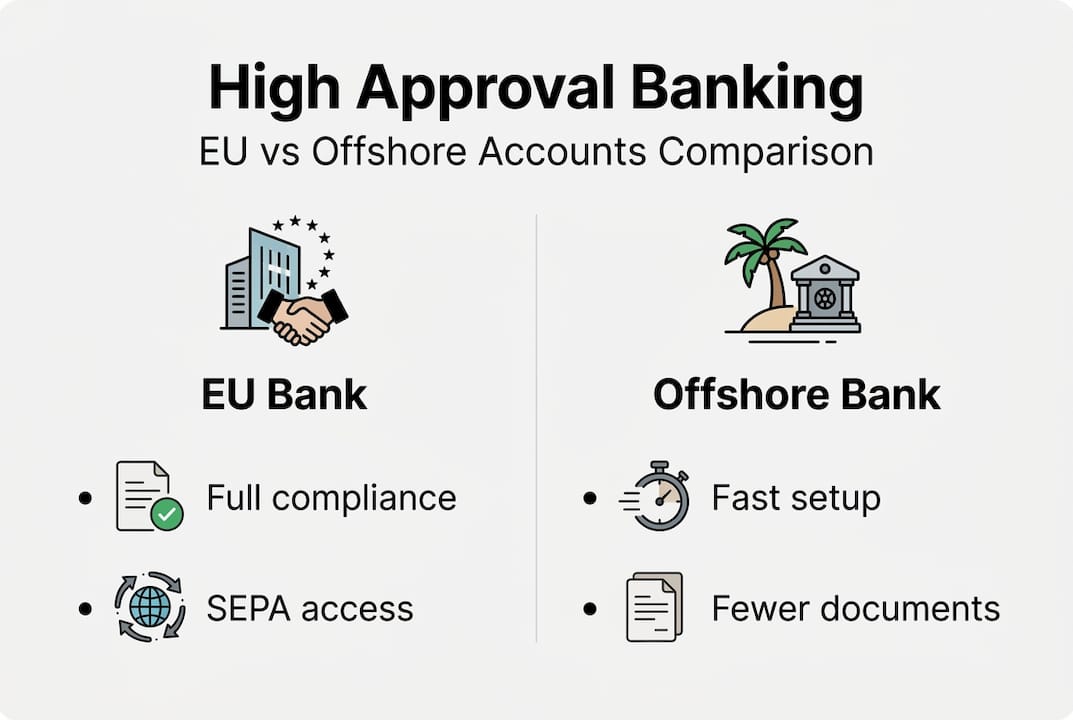

EU versus offshore high approval banking: a practical comparison

A core choice for many high-risk businesses is whether to bank in the EU, offshore, or both. Each option carries distinct advantages and trade-offs.

Offshore banks often offer faster onboarding, but EU banks provide stronger compliance frameworks that carry more weight with payment networks and regulators. EU-based accounts may take longer to open due to stricter regulatory checks, but they offer greater credibility with counterparties.

| Factor | EU banking | Offshore banking |

|---|---|---|

| Onboarding speed | 2 to 4 weeks | 3 to 10 days |

| Regulatory credibility | Very high | Moderate to high |

| Compliance requirements | Strict (AMLD6, PSD2) | Varies by jurisdiction |

| Transaction costs | Moderate | Often lower |

| Best suited for | Long-term EU operations | Speed, flexibility, diversification |

| Risk of de-risking | Lower | Moderate |

Many experienced operators use both. An EU account provides regulatory credibility and access to SEPA, while an offshore account offers speed and flexibility for international transactions. This dual structure is increasingly common among crypto and forex businesses operating across multiple markets.

Risks, pitfalls, and what to look out for

After comparing options, it is vital to know what to avoid. The high approval banking market attracts both genuine specialists and opportunists who exploit desperate businesses.

“Some ‘high approval’ offers are scams or may lead to account freezes if not truly regulatory-compliant.” The safest path is always through a provider who insists on full documentation and compliance review before promising any outcome.

Red flags to watch for when opening a high-risk account:

- No KYC or AML process — Any provider skipping these steps is either unregulated or operating illegally.

- Guaranteed approval before review — Legitimate banks assess applications. Guarantees before review are a warning sign.

- Vague jurisdiction information — If they cannot tell you exactly where the bank is regulated, that is a problem.

- Unusually low fees — Hidden charges often surface after onboarding, or the account gets closed without warning.

- No ongoing compliance support — A provider who disappears post-onboarding leaves you exposed to de-risking.

Using a structured high-risk banking checklist before engaging any provider helps you filter out the bad actors quickly. You can also explore bank account pre-approval processes that allow you to assess your eligibility before committing time and resources to a full application.

How to maximise your high approval banking success

With clarity on risks, the next step is a practical roadmap for securing a high approval account and keeping it.

Proper preparation and documentation can boost approval rates by up to 70%. That is not a marginal improvement. It is the difference between operating and stalling.

Follow this sequence:

- Audit your compliance position — Review your KYC, AML, and source-of-funds documentation before approaching any bank.

- Obtain or confirm your regulatory licence — Operating with a recognised licence in your jurisdiction is non-negotiable for most high approval providers.

- Select the right jurisdiction — EU or offshore? Your business model, transaction volumes, and target markets should drive this decision.

- Prepare a complete application package — Company registration documents, director identification, proof of funds, business plan, and compliance policies.

- Engage a specialist intermediary — A consultancy with pre-vetted banking relationships dramatically reduces rejection risk and onboarding time.

- Maintain the relationship post-approval — Respond promptly to bank queries, update your compliance files regularly, and flag any business model changes proactively.

The businesses that maintain high approval accounts long-term are not the ones with the cleanest sectors. They are the ones with the most organised compliance posture. Understanding how to pass bank compliance for a high-risk account is a skill worth investing in early.

Pro Tip: Build a dedicated compliance folder with version-controlled documents. Banks revisit your file during annual reviews. Having everything current and organised signals professionalism and reduces the risk of sudden account review.

Get expert support for high approval banking

Navigating the high approval banking landscape is genuinely complex, particularly when you are managing a crypto exchange, iGaming platform, or forex operation alongside it. BankMyCapital works directly with high-risk businesses to move them from application to approval, with an 87% success rate across a network of over 50 pre-vetted banking partners and EMIs. Whether you need to understand your rejection risks before applying, work through a structured banking checklist for success, or get a clear picture of what high risk banking means for your specific sector, the team provides sector-specific guidance and hands-on compliance expertise. Onboarding typically completes in two to three weeks, with Swiss-grade encryption protecting your sensitive data throughout the process.

Frequently asked questions

Who qualifies for high approval banking?

Generally, regulated online businesses with complete compliance documentation in high-risk sectors such as crypto, iGaming, or forex are eligible. High approval accounts are tailored to compliance-ready firms, not businesses seeking to avoid scrutiny.

How long does it take to open a high approval bank account?

Offshore accounts may open within days, while EU-based accounts typically take two to four weeks. EU onboarding is slower due to stricter regulatory checks, but the resulting account carries greater credibility.

Is high approval banking safe?

Yes, provided you choose a regulated, compliance-focused provider and avoid any service promising approval without documentation. Regulated providers minimise the risk of account freeze or unexpected closure.

What documents are usually required?

Expect to provide company registration certificates, director identification, proof of funds, and a full compliance and KYC profile. A thorough preparation checklist covers both corporate and personal compliance documents.

Can I have multiple high approval accounts?

Yes, and many high-risk firms actively maintain both EU and offshore accounts for operational flexibility and risk management. Dual account setups offer business continuity if one account faces disruption.